Domestic induction furnace finished long steel offers witnessed volatility this week. Prices varied in the range of INR 100-1,00/t. On the other hand, trade reference prices for hot rolled coil (HRC) and cold rolled coil (CRC) saw a downtrend, falling in the range of INR 100-500/t w-o-w.

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, decreased by INR 100/t w-o-w to INR 9,250/tonne (t) DAP Raipur on 27 December. Pellet prices in Raipur continued to face downward pressure this week, driven by muted demand and falling sponge iron and semi-finished steel prices.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index decreased by $2.5/tonne (t) w-o-w to $62.5/t FOB east coast, India, on 26 December. Indian iron ore fines export offers continued to face downward pressure, as buyers avoided procuring lower-grade material at higher prices. The market saw muted trading activity due to a growing bid-offer disparity, with the discount for lower-grade fines widening to 20-21% on the global index (from 18-20% last week) following a lack of inquiries.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) fell by $1.5/t w-o-w to $96/t on 27 December. The seaborne market remained silent due to the Christmas holidays, with nil inquiries seen this week. Moreover, some sellers focused on domestic deals due to better realisations.

- Dry bulk iron ore freight rates showed mixed trends this week, driven by the recovery in import demand tied to China’s steel production and seasonal restocking. According to BigMint’s assessment, Asia-Pacific Supramax dry bulk freights (50,000-55,000 t) for iron ore shipments from the east coast of India to China increased $1/tonne (t) w-o-w to $12/t on 24 December.

Coal

- India’s portside prices of South African thermal coal dipped further this week due to increased port stocks and subdued buying sentiment ahead of the holidays. RB2 (5500 NAR) prices fell by INR 100/t to INR 9,250/t, while RB3 (4800 NAR) dropped by INR 50/t to INR 7,750/t, both ex-Gangavaram.

- BigMint’s assessment shows 4500 GCV coal dropping by INR100/t to INR4,800/t, while 5000 GCV coal declined by INR400/t to INR 5,600/t, exw-Bilaspur.

- In a recent notification, the Director General of Foreign Trade, Government of India, has sanctioned the imposition of “quantitative restrictions” on imports of low-ash metallurgical coke (met coke) into India. The country-wise quantitative restrictions on coke have been announced for two quarters of 2025 i.e. January-March and July-September, with the total volume pegged at 713,583 t for each quarter.

Ferro scrap

- India’s imported scrap market saw moderate demand with a slight decline in prices last week. Shredded scrap from the UK, which was offered at $390/t CFR last week, fell by about 1% to $385/t CFR this week. The market was affected by the holiday season, leading to fewer fresh offers and limited supplier activity. Many suppliers were fully booked for January shipments, with little new material available, as many yards temporarily halted operations.

- Prices for HMS (80:20) from the UK remained steady at $365/t CFR, while offers from other regions, including West Africa and Latin America, ranged from $360-370/t CFR. The holiday season and a slowdown in the domestic steel market contributed to cautious buyer sentiment.

- However, the market was quieter than usual due to the upcoming holidays, with limited supply and price stability expected to continue into the new year. There is some expectation that prices may rise slightly once the holiday period concludes and supply resumes.

- Approximately 12,500-13,500 t of scrap were booked, including 5,000-6,000 t of shredded scrap from Australia and the US at $382-385/t. Additionally, 5,000-5,500 t of HMS (80:20) were booked from Brazil, West Africa, and Chile at $360-375/t. There was also a mix of HMS and LMS, as well as handloaded HMS and HMS1 sourced from Yemen and South America, at $365-385/t.

Ferro Alloys

- Silico Manganese: Domestic silico manganese offers in India witnessed elevation this week due to constrained supply and strong seller offers. This modest increase marks a shift in market dynamics, with sellers gaining influence. Prices of the 60-14 grade rose by INR 1,150/t ($13/t) w-o-w to INR 67,300-68,000/t ($788-796/t) exw in Raipur, Durgapur, and Visakhapatnam.

- Ferro manganese: Indian ferro manganese (HC 70%) prices rose by INR 2,950/t ($35/t) to INR 70,900/t ($830/t) exw in Raipur and by INR 3,000/t ($35/t) to INR 70,800/t ($829/t) exw in Durgapur. Prices surged on limited supplies in the market as many players have taken production cuts in key regions.

- Ferro silicon: Indian ferro silicon (FeSi: 70%) prices rose by INR 1,000/t ($12/t) w-o-w to INR 103,900/t ($1,217/t) exw-Guwahati on 27 December. While, Bhutan’s prices also went up by INR 800/t ($9/t) to INR 104,000/t ($1,218/t) exw. Offers rose due to limited supply, with further increases anticipated as Bhutanese sellers’ BIS licenses expire.

- Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si: 4%) prices registered a decline of INR 5,950/t ($70/t) to INR 102,550/t ($1,201/t) exw-Jajpur. Prices fell w-o-w on waning stainless steel demand and lower bids in recent auctions. Additionally, Tsingshan lowered its ferro chrome tender price for January’25 by RMB 400/t ($55/t) m-o-m to RMB 6,995/t ($958/t).

Semi-Finished Steel

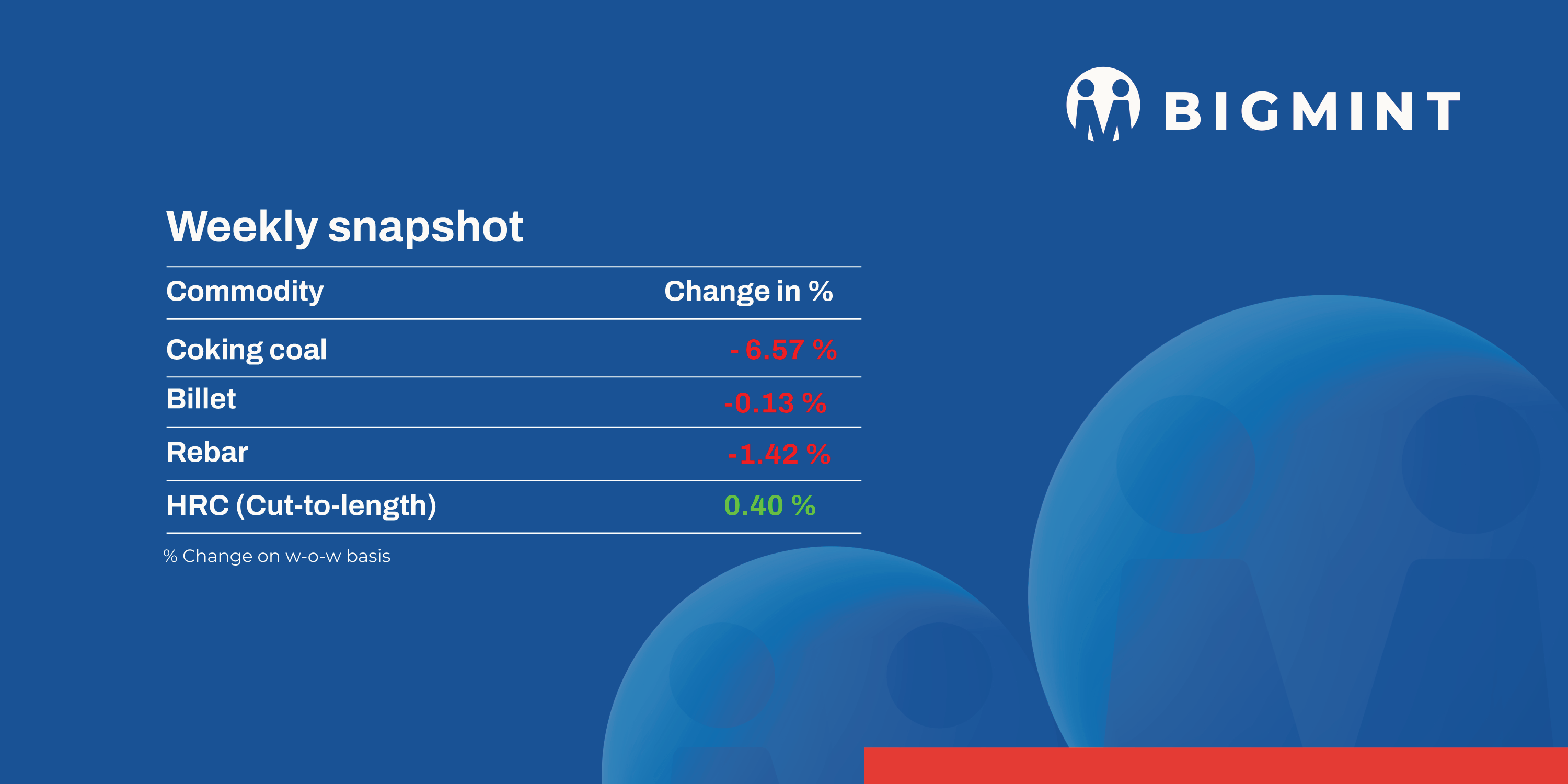

- Indian semi-finished steel prices exhibited mixed trends. Domestic billet prices showed divergent trends. At some locations prices decreased by INR 100-500/t , with a major decrease of INR 500/t seen in the Goa and Hyderabad markets, while at some other locations prices trended up by INR 150-600/t. However, sponge iron prices declined in many markets in the range of INR 100-1,000/t, with a major decrease of INR 1,000/t seen in the Hyderabad market. However, Durgapur, Bellary and Mandi Gobindgarh showed a slight uptick.

- SAIL-Bokaro Steel Plant (BSL) held an auction for 14,000 t of steel-grade pig iron on 26 December. Out of the total volume, 7,000 t were booked at an average price of INR 30,900/t exw. In the previous auction on 8 November, the entire quantity of 14,000 t of steel-grade pig iron was sold at an average price of INR 35,000/t exw.

- Indian DRI (Direct Reduced Iron) export offers increased by $1/t, reaching $350/t CPT Raxaul while CPT Benapole offers decreased by $11/t to $349/t.

Finished Long Steel

- IF route: India’s induction furnace route finished long steel prices saw a mixed trend w-o-w. Trading activities remained dull throughout the week amid lack of buying interest. Sellers were offering attractive discounts to boost sales depending on the location. However, buyers chose to stay on the sidelines. A similar trend was seen in sponge iron and steel billet markets. As per sources, prices are likely to remain volatile in the near term.

- On a weekly basis, rebar steel prices witnessed a variation in the range of INR 200-1,000/t across regions, as per BigMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 41,500-41,900/t exw Raipur, INR 46,900-47,500/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 43,800-44,300/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 42,400-42,800/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices fell w-o-w owing to subdued domestic demand across markets. Buyers have moved to the sidelines and adopted a wait-and-watch approach due to continuous drop in prices and weak market sentiments. Current week’s rebar prices (12-32mm) in the trade segment edged down by INR 100/t w-o-w to INR 52,300/t exy-Mumbai, excluding 18% GST.

- In the project segment, prices fell w-o-w to around INR 49,500-50,500/t FOR Mumbai amid limited buying interest.

Flat Steel

-

- Hot-rolled coil (HRC) prices continued to see sustained downward pressure, declining by up to INR 500/t ($6/t) to a new low of INR 46,700-48,500/t ($642-679/t). Conversely, cold-rolled (CR) coil prices remained rangebound at INR 53,400-58,800/t ($703-762/t) in key markets. Despite an increase in offers stemming from the safeguard duty investigation, most buyers resisted these price levels.

- Imports of bulk HRCs and plates declined to 2,77,175 t till 23 December, as per the bulk vessel line-up data maintained with BigMint. Further, it is expected that around 89,717 t will be imported by the month end.

- Indian HRC export offers to the Middle East (ME) remained largely stable w-o-w. However, trading activity in the region slowed significantly due the Christmas and New Year holidays, according to sources based in the ME. Indian HRC export offers to the Middle East were stable at $540-545/t CFR UAE.

- Similarly, the European market witnessed subdued activity, with many participants in the EU already on holiday. Export offers to Europe were also steady at $590-595/t CFR Antwerp ($540-545/t FOB, east coast India) for S275, 3 mm material.

Leave a Reply