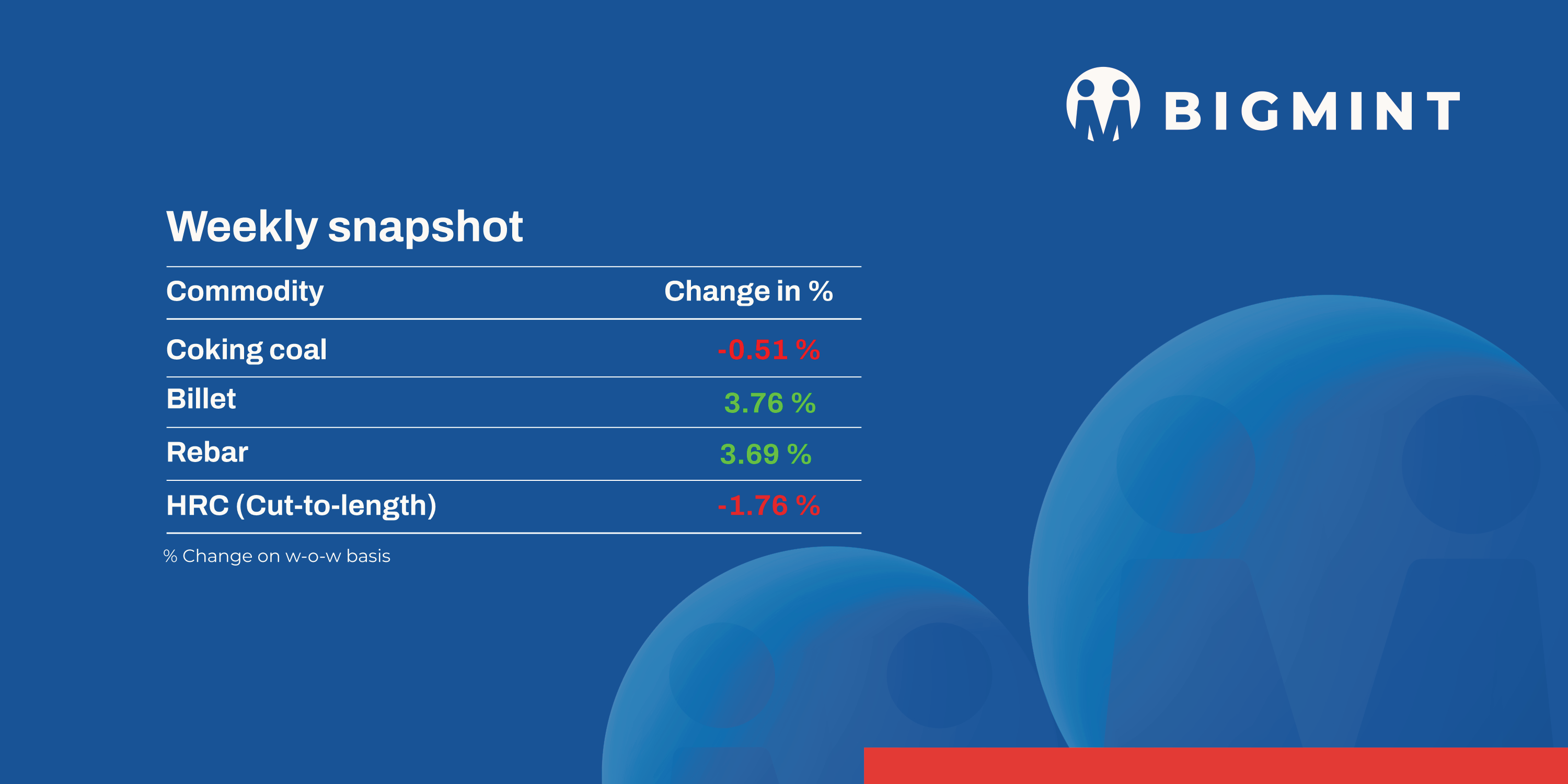

The domestic steel market saw positive trends in prices during week 38 of CY’24 (16 September – 21 September 2024), as semi-finished steel prices edged up by INR 100-1,350/tonne (t) amid an increase in steel demand. However, domestic induction furnace (IF) finished long steel offers showed upward trends.

Iron ore and pellet

- Odisha Mining Corporation (OMC) conducted an auction for 2.4 million tonnes of iron ore on 20 September, in which the entire quantity was sold at a premium. Around 1.377 mnt of fines (Fe 54-65%) and 1.021 mnt of lumps (Fe 58-64%) were booked at INR 2,370-4,970/t and INR 3,900-6,800/t, respectively. Bids (weighted average) for fines and lumps increased by around INR 275/t and INR 50/t against last month. The company has rolled over base prices of both fines and lumps for the majority of the lots compared to last month’s base price. Recent improvements in sponge iron ore prices and tight availability of high-grade ore due to the extended monsoon supported the premium bids in the auction.

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, inched down by INR 50/t w-o-w to INR 8,600/t DAP Raipur on 20 September. This week, deals of around 59,000 t of pellet (Fe62.5-63%) were recorded in the Raipur region. Raipur-based pellet makers kept their offers for Fe 63%(+/_0.5%) stable at INR 8,600/t ($102/t) exw-Raipur.

- National Mineral Development Corporation (NMDC) auctioned 348,000 t of iron ore on 13 September 2024 from its Kumaraswamy mines. Around 128,000 t of lumps (10-40 mm, Fe 59.58-64.41%) were booked at INR 4,464-5,877/t against base prices of INR 3,704-4,677/t, while 220,000 t of fines (Fe 60.53-64.56%) were booked at INR 3,652-4,897/t against base prices of INR 3,302-3,996/t. Prices were on ex-mines basis, including royalty, DMF, and NMET.

- BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index inched down by $0.5/t w-o-w to $53/t FOB east coast on 19 September 2024. The discount level on the global fines index remained similar to last week’s at 20-23%. The India pellet (Fe 63%, 3% Al) export index (FOB east coast) remained stable w-o-w at $85/t on 20 September.

Coal

- Australian premium hard coking coal prices picked up by 4% to $187.65/t FOB. Market participants are awaiting clarity regarding future pricing directions.

- RB1 (6000 NAR) grade coal prices remained unchanged w-o-w at $101/t FOB. RB3 prices edged down at $69/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port remained unchanged at INR 7,600/t.

Ferro scrap

- In India, the week saw sluggish demand for imported scrap, as buyers leaned towards cheaper domestic alternatives due to weak steel sales. Shredded scrap offers remained steady at $385-390/t CFR, but buyers showed little urgency to purchase. By mid-week, some optimism emerged, with hopes of a market rebound in October, driven by restocking ahead of the festival season and potential US Fed rate cuts improving liquidity.

Despite this, challenges like bid-offer mismatches and a weak domestic market continued to hamper trade, with buyers holding off on deals, waiting for prices to align with expectations.

HMS (80:20) offers from Europe and West Africa ranged within $365-370/t CFR Nhava Sheva.

Ferro Alloys

- Silico manganese: Silico manganese prices decreased marginally w-o-w by around INR 650/t ($8/t) to INR 65,000-65,500/t ($779-785/t) exw in Raipur, Durgapur, and Visakhapatnam. Domestic silico manganese prices have continued to decline w-o-w, with the market facing a prolonged downturn due to reduced trades, shrinking profit margins, and weakening demand.

- Ferro manganese: India’s ferro manganese (HC70%) prices in Raipur went down by around INR 1,000/t ($12/t) w-o-w to INR 70,000/t ($839/t) exw. Meanwhile, in Durgapur, prices diminished by around INR 1,100/t ($13/t) w-o-w to INR 69,700/t ($835/t). Prices declined due to slow demand and subdued trade activities.

- Ferro silicon: Indian ferro silicon (FeSi:70%) prices increased by around INR 900/t ($11/t) w-o-w to settle at INR 89,300/t ($1,070/t) exw-Guwahati on 20 September. Meanwhile, prices in Bhutan also rose by INR 2,200/t ($26/t) w-o-w, reaching INR 91,200/t ($1,092/t) exw. The price rise was driven by higher trade settlements, which influenced the market trend.

- Ferro chrome: Prices of Indian high-carbon ferro chrome (HC60%, Si:4%) remained largely stable, inching up INR 100/t ($1/t) w-o-w to INR 107,100/t ($1,283/t) exw-Jajpur on 20 September amid stable market sentiments. The recent OMC chrome ore auction saw rising bid prices for lower grades, which are expected to impact price trends for the upcoming week.

Semi finished

- Indian semi-finished steel prices showed an upward trend as per BigMint’s assessment. Domestic billet prices in almost all key locations increased by INR 100-1,350/t across regions, with a major increase of INR 1,350/t seen in the Raipur market. Similarly, sponge iron prices also increased in almost all key locations by INR 200-1,050/t, with a major increase of INR 1,050/t seen in the Raigarh market.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 32,000 t on 19 September 2024. Out of the total quantity, 24,000 t were booked at an average price of INR 33,500/t.

- SAIL-Bokaro Steel Plant (BSL) held an auction for 14,500 t of steel-grade pig iron on 20 September 2024. The entire quantity was booked at an average price of INR 34,950/t exw.

- Indian direct reduced iron (DRI) export offers decreased by $5 for CPT Raxaul, reaching $342/t, while CPT Benapole offers decreased by $5/t to $360/t.

Finished long steel

- IF-rebar: India’s IF route finished long steel prices surged w-o-w basis. Trading improved slightly as prices bottomed out, post which sellers tried to hike their offers. A similar trend was observed in sponge iron (PDRI) and steel billet. Buyers booked average volumes but avoided bulk procurement, choosing to wait for further clarity on the market direction. Participants are of the view that further improvements may be noticed, as decent bookings were observed at the current levels, which might continue in the near term.

- On a w-o-w basis, rebar steel prices increased in the range of INR 200-1,500/t across the regions as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 42,000-42,400/t exw-Raipur and INR 45,500-46,000/t exw-Jalna.

- The trade reference price of heavy structural steel for the base size 150 mm channel stood at INR 44,500-45,000/t exw-Raipur.

- The trade reference price of wire rods hovered at INR 42,600-43,100/t exw-Raipur.

- BF-rebar: Blast furnace (BF) rebar trade prices witnessed mixed trends across markets during the week. Demand in the distribution channel network remained slow, which weighed on market sentiments.

- A leading PSU steelmaker raised rebar prices by INR 1,500/t earlier this week due to constrained supply, as the company is currently running only one blast furnace. This resulted in a slight uptick in rebar trade prices across markets in the southern part of the country.

- The current week’s rebar prices (12-32 mm) in the trade segment dropped by INR 600/t w-o-w to INR 50,000/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the project segment, prices hovered at around INR 48,500-49,500/t FOR Mumbai. Buying interest was limited amid need-based procurement.

Finished flat steel

- Hot-rolled coil (HRC) prices declined by INR 1,000/t and are now ranging between INR 47,000-51,000/t. Similarly, cold-rolled coil (CRC) prices also decreased by INR 1,000/t, maintaining a range of INR 55,000-60,000/t across various markets. The market is currently experiencing subdued demand alongside increased supply, which is putting downward pressure on prices.

- Market rumours suggest that several steel mills have announced preliminary price adjustments for HRC and CRC in September. These adjustments reportedly include either price decreases or price support measures ranging from INR 500-1,000/t. However, an official confirmation regarding the same has remained elusive.

- The expected list prices of HRCs (IS2062, Gr- E250, 2.5-8 mm) stood at around INR 49,000-50,000/t ex-Mumbai, while that of CRC (IS513, Gr-O, 0.9 mm) were at around INR 55,000-56,000/t ex-Mumbai for September 2024 sales. These prices are for the coil form and exclude GST at 18%. However, the list prices of a few private mills have not been revealed yet.

- Cumulative import volume, based on vessel lineup data, reached 5,11,767 t till 16 September 2024. However, an additional 2,85,071 t are expected by the end of September.

- Indian steel mills have maintained their HRC export offers to Southeast Asia and the Middle East in light of sluggish global market sentiment and the Chinese Mid-Autumn Festival holidays. In contrast, Indian HRC export offers to Europe remained stable w-o-w, with no confirmed transactions reported due to the ongoing anti-dumping investigation.

Leave a Reply