- Chinese market witnesses lower steel demand

- No iron ore export deals from India in last one week

- Inventory levels remain range-bound at ports

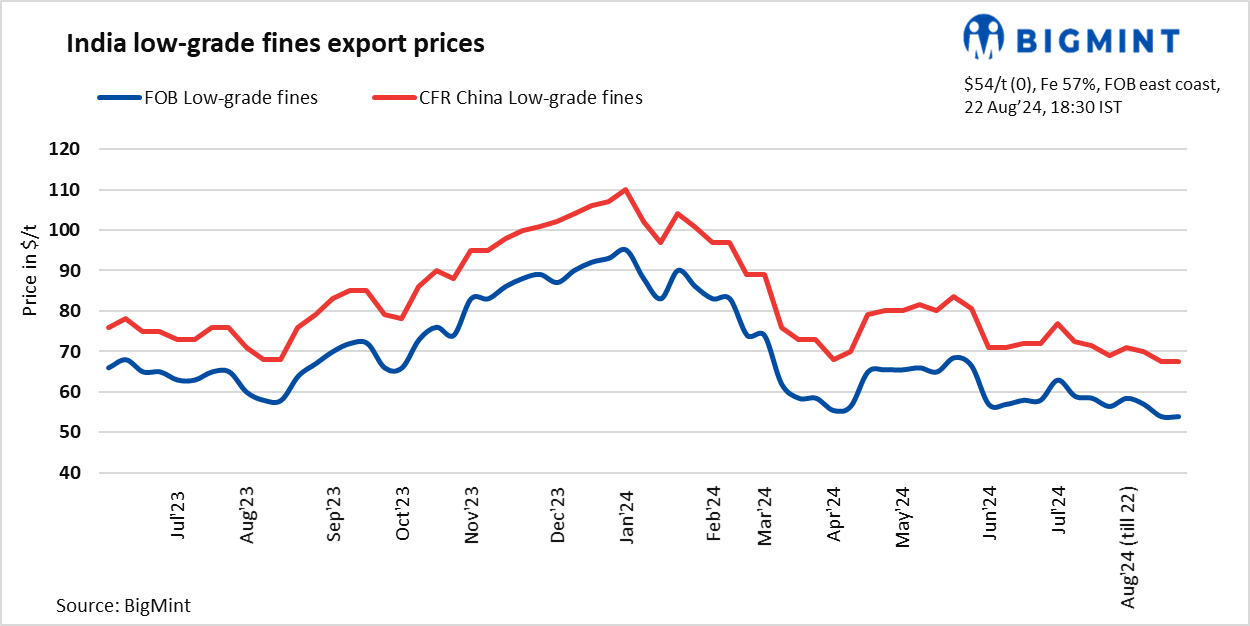

The iron ore seaborne market remained inactive over the week amid sluggish response from the Chinese mills for the Indian material. Sellers waited for the decent price level. However, seaborne prices continued to fluctuate. BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $54/t FOB east coast on 22 August 2024. The market remained silent with no major trades concluded by the Indian iron ore exporters.

Market participants said that demand for the lower grade fines was witnessed in the seaborne market. However, bids from the buyers were very low. As a result, they were not viable for the Indian exporters for active transactions. Sources stated that exporters were unwilling to accept prices below $70/t CFR China for deals. Most sellers stayed away from the market, anticipating a price improvement in the near term. However, this anticipated improvement is unlikely to materialise positively in the coming days.

Iron ore inventories in China’s major ports dropped by 0.4 mnt to 149.2 million tonnes (mnt) on 22 August compared to the last week, according to SteelHome data.

According to a source, August’s shipment volumes from India are also anticipated to drop sharply because the impending strike threatens to interfere with port operations in India. The strike is expected to cause operational disruptions at most ports in the country, potentially hindering the movement of cargo.

Recently, Indian fines performed well due to their cost-effectiveness. However, potential taxes, unstable exports, and supply issues from mines have cast a bleak outlook. Currently, Chinese mills are focusing on purchasing lower-grade Australian special fines. This shift is driven by the need to reduce manufacturing costs amidst lower finished steel demand and to avoid the higher costs associated with higher-grade fines.

Price indicators

- No confirmed deal was reported from the East Coast this week and taken into price calculation under T1 trade and given 0% weightage in the index calculation. For detailed methodology Click here.

- BigMint received nine (9) indicative prices in the current publishing window and seven (7) were considered for price calculation as T2 inputs and given 100% weightage.

Factors impacting the seaborne market-

- Iron ore spot prices stable w-o-w: The benchmark iron ore fines remained stable w-o-w at $98/t CFR China on 21 August. Prices remained stable amid improved market sentiment and positive demand outlook, despite an ongoing pressure on steel production levels. As per report, slight uptick in downstream steel demand, particularly for rebar, was observed as mills maintained low inventory levels.

- Portside offers in China up w-o-w: Portside offers of Indian iron ore fines (Fe57%) in China rose by RMB 25/t ($3/t) w-o-w on 22 August. Offers were recorded at around RMB 555/t ($77/t) at Qingdao Port, including all import taxes and port charges. D-o-d, portside prices remained unchanged today.

- DCE futures up w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2025 contract increased by RMB 17/t ($2/t) w-o-w to RMB 730/t ($103/t) on 22 August. D-o-d, future prices fell by RMB 12/t ($2/t) against RMB 742/t ($104/t) yesterday.

Outlook

Seaborne iron ore export prices are expected to remain volatile in the near term. The production levels of Chinese mills will significantly influence Indian iron ore export prices in the coming period.

Leave a Reply