Turkish imported ferrous scrap index sharply dropped by $10/t w-o-w. Turkish steel producers have largely remained inactive in the deep-sea scrap import market due to weak finished steel sales and the availability of low-cost billets from Asia, particularly China. Although Turkish steelmakers re-entered the deep-sea scrap market last week for September and early October shipments, demand was limited, hampered by competition from cheaper Asian billet imports. A regional steel mill recently secured billets and a larger volume of slabs from Indonesia at $500-505/tonne (t) CFR.

As of today, the weekly price assessment for steel billet imports, CFR Turkiye, is $490/t, down $10 from the previous week’s range of $500/t. Similarly, under pressure from cheaper billets, BigMint’s assessment for US-origin HMS (80:20) bulk scrap has reached its lowest level for 2024.

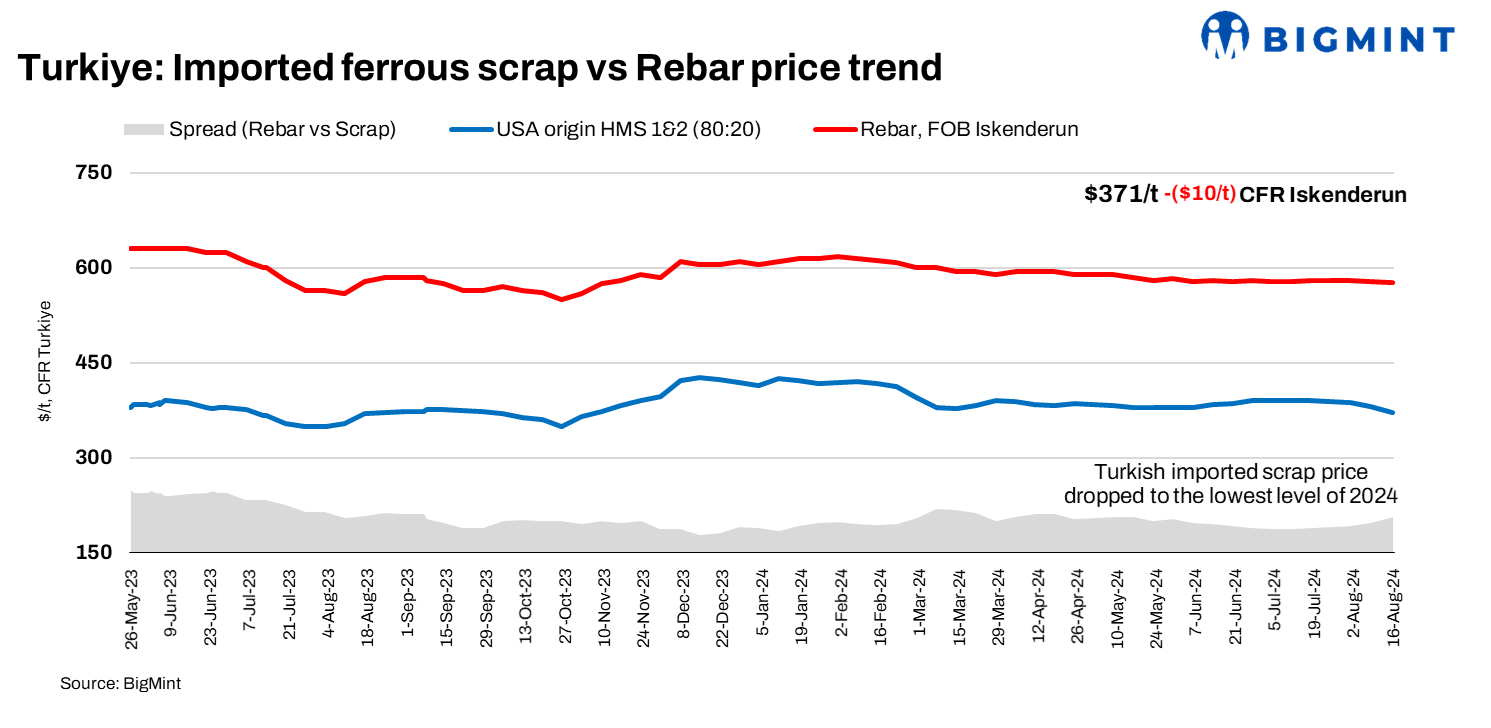

Assessment trends

- BigMint’s assessment for US-origin HMS (80:20) bulk scrap stood at $371/t CFR, down by $10/t w-o-w.

- BigMint’s assessment for bulk HMS (80:20) from the US East Coast stood at $347/t FOB, down $6/t w-o-w.

The scrap-to-rebar spread was assessed at $205-206/t FOB, widened as compared to last week.

Turkish steel mills are trying to maintain their steel prices, but this may prove challenging. They might need to lower finished long product prices below $570/t soon to sustain sales.

According to suppliers, Turkish steel producers are largely inactive in the deep-sea scrap market. They are closely monitoring the market for potential further price declines, given their current focus on billets and slabs, which are exerting pressure on scrap prices.

Recent deals

- Aegean-origin mill booked another Europe-origin bulk cargo with HMS (80:20) at $364.5/t CFR Turkiye.

- Europe-origin supplier sold bulk cargo to an Aegean-origin mill comprising 35,000 t of HMS (80:20) at $369/t CFR Turkiye.

In the shortsea market, a Turkish mill in Samsun booked Bulgaria-origin HMS (80:20) at $354-356/t CFR and Romania-origin material at $358-360/t CFR, with bids for Romania-origin scrap at $363-365/t CFR being less viable from the supplier side. Workable levels for shortsea scrap were reported at $352-$356/t CFR.

Outlook: Recyclers struggled to attract demand as buyers anticipated lower prices in the near-term, targeting US-origin HMS (80:20) at $368-369/t CFR and below.

Leave a Reply