The South Asian ferrous scrap index continued to trend downwards. In India, buyers were not interested in imported scrap due to bid-offer disparities, cost-effective local alternatives, and weak steel demand. Pakistan saw limited demand as buyers await price drops amid domestic market slowdowns. Bangladesh is facing political instability, with market activity expected to remain subdued for some time. Meanwhile, in Turkiye, imported ferrous scrap prices held steady, but mill inquiries were scarce, prompting sellers to offer more aggressively.

Overview

India: Indian buyers continued to show disinterest in imported scrap due to bid-offer disparities, the availability of cost-effective sponge iron and local scrap, and subdued steel demand. Additionally, only a few suppliers were active in the market, with many holding back due to unviability.

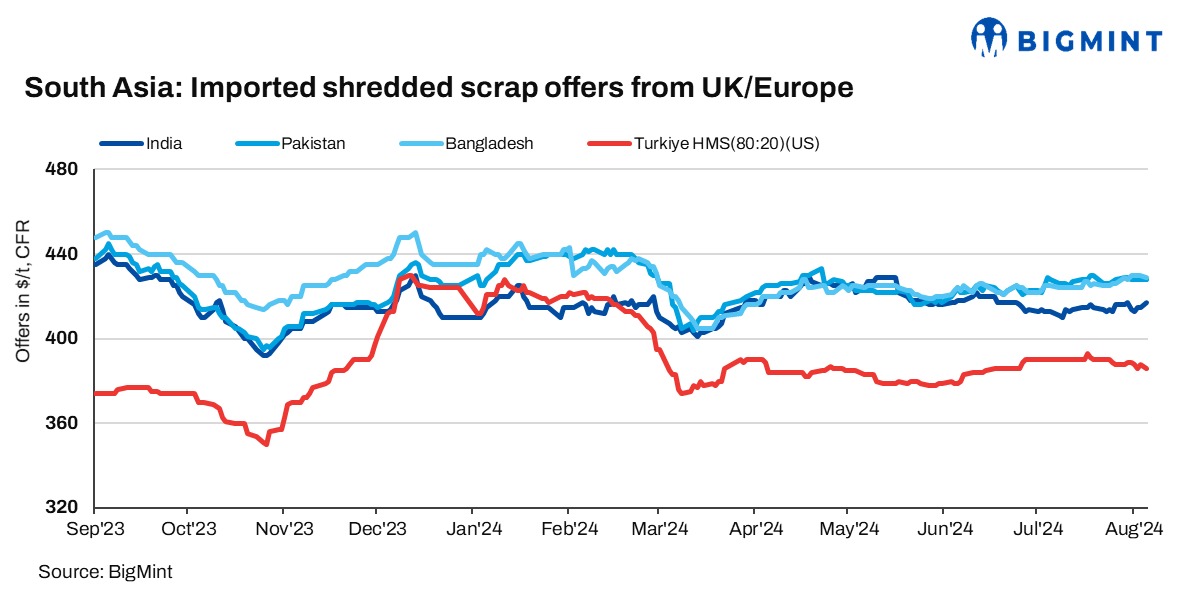

Indicative offers for shredded scrap from the UK/Europe were around $415-420/t CFR Nhava Sheva, while buyers sought prices below $400-405/t CFR. HMS (80:20) offers from the UK/Europe were heard at $390/t CFR Nhava Sheva, while buyers considered workable levels to be around $385/t CFR.

A prominent supplier stated, “Scrap imports are unviable in India at the moment. We’ve stopped offering, and even if we do, it won’t be less than $430/t, so we refrained from doing it.”

A trade source said, “The Indian market is sluggish with dull finished sales, good sponge availability, and local scrap still cheaper than imported.”

Pakistan: Demand for imported scrap remained limited as buyers anticipate a price drop and a slowdown in the domestic steel market due to payment delays and lower finished steel margins. Indicative offers for shredded scrap from the UK/Europe were assessed at $425-430/t CFR Qasim.

A steel mill official said, “Last week, due to rains, our work was impacted. It was bill payment week, and customer payments are being delayed. Moreover, average sales prices are below cost, so we are unable to buy scrap, and finished steel sales are limited.”

Bangladesh: The Bangladesh market remains unstable, with expectations of being out of action for some time due to ongoing political turmoil. There are speculations of a temporary government or even a military takeover until re-elections occur or the situation stabilises. The last heard indicative offers for shredded scrap from the UK/Europe were at $425-430/t CFR Chattogram, while HMS (80:20) was at $408-410/t CFR.

Domestic scrap prices have slightly increased to BDT 62,000-62,500/t, while rebar prices remain unsupportive at BDT 91,000-92,000/t ex-Chattogram.

Turkiye: Turkish deepsea imported ferrous scrap prices remained unchanged at $386/t CFR. Mill inquiries were scarce, leading sellers to offer more aggressively to attract demand. Indicative tradable values for US/Baltic-origin premium HMS (80:20) ranged from below $386-390/t CFR. Turkish mills, having recently imported large volumes of billets, were considering production cuts. The rebar market was stagnant, with prices assessed at $575/t FOB, down $5 from last week.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $417/t CFR Nhava Sheva, up by $2/t compared to last closing on Friday.

Pakistan: UK-origin shredded indicatives were assessed unchanged at $428/t CFR Qasim compared to the last closing on Friday.

Bangladesh: UK-origin shredded prices were assessed at $429/t CFR Chattogram, down by $1/t compared to the last closing on Friday.

Turkiye: US-origin HMS (80:20) bulk prices were assessed unchanged at $386/t CFR Turkiye compared to the last closing on Friday.

Leave a Reply