- Bid-offer disparity in seaborne market

- Global fines spot, future prices range-bound w-o-w

- Slight drop in pellet inventory at Chinese ports

The Indian pellet sellers in the seaborne market remained silent in the past few days following the downtrend prices of global iron ore and steel. The pellet inventory at the Chinese port dropped but demand has remained under pressure due to maintenance shutdown and low steel demand in China.

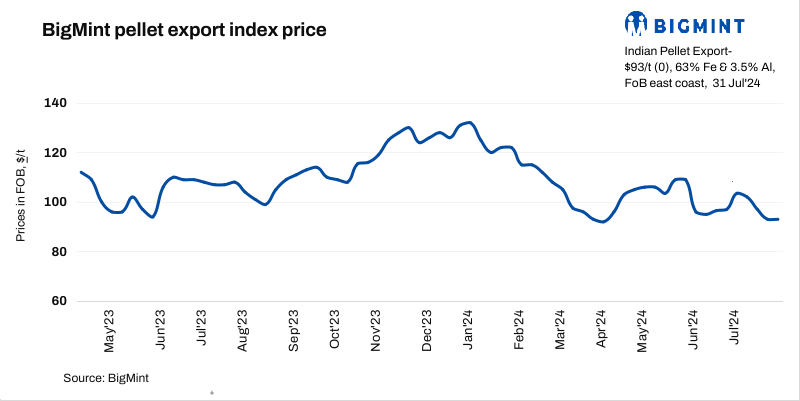

BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) remained stable w-o-w at $93/tonne (t) on 31 July 2024. No pellet export was recorded from India in the last one week.

As per sources, the price disparity between buyers and sellers had prevented pellet export deals from India. Few buyers offered around $5-6/t premium on the global fines index which were not accepted by the sellers.

A pellet producer said, “The pellet production costs are higher due to moderate iron ore fines prices in the market. The downtrend sentiments in the Chinese market kept Indian pellet under pressure in the overseas market. We are holding the offers and waiting for the improvement in the global market for the next transactions.”

Notably, domestic prices in India are still INR 1,200/t ($14/t) higher than exports. Pellet (Fe 63%) prices in Odisha’s Barbil fell by INR 50/t ($0.5/t) w-o-w to INR 7,050/t exw ($85/t). However, ex-plant realisation for pellet exports in Barbil remained largely stable w-o-w to INR 5,800-5,900/t exw ($70-71/t).

An exporter reported that due to heavy rain in China, mill operations were disrupted and faced logistical hurdles. As a result, raw material demand decreased and it is anticipated that prices will remain under pressure for the next few weeks. The pellet option to feed is not viable for them due to a negative import margin. However, inventory at port side dropped last week.

Rationale:

- No pellet export deals were recorded in the last one week and were not taken under price calculations. Hence these were accorded 0% weightage in the index calculation Click here for detailed methodology.

- Eleven (11) indicative prices were received and nine (9) were considered for calculation of the index and given a 100% weightage.

Factors impacting pellets export market

- Iron ore fines index range-bound w-o-w: The benchmark iron ore fines index fell by $1/t to $99/t CFR China on 30 July. Prices were under pressure following planned maintenance for some blast furnaces amid weak steel mill margins and growing uncertainty in market demand due to heavy rain. Discounts remained wide due to the accumulated supply and lack of demand.

- DCE futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2024 contract dropped by RMB 7.5/t ($1/t) w-o-w to RMB 768/t ($106/t) on 31 July. On a d-o-d basis, futures prices rose by RMB 12/t ($2/t) against RMB 756/t ($104/t) yesterday.

- Portside pellet prices edge down w-o-w: Chinese sources said that Qingdao portside offers for Indian pellets (Fe 63.5%) inched down by RMB 5/t ($1/t) w-o-w to RMB 945/t ($129/t) on 31 July, inclusive of all import taxes and port charges. Meanwhile, prices improved by RMB 5/t ($1/t) d-o-d.

- Pellet inventories drop w-o-w: Pellet inventories at China’s major ports decreased by 0.45 mnt to 6.25 mnt on 25 July, 2024 compared to last week, according to SteelHome data.

Outlook

BigMint noted that seaborne pellet offers are expected to remain volatile due to global fines price fluctuations and uncertain market dynamics in China. The exporters are expecting a positive market trend but due to lower steel demand in China, premium material is avoidable for mills currently.

Leave a Reply