This week, global ferrous scrap prices dropped by 1-5% across various markets. Indian buyers avoided the seaborne market due to unviable current prices. Pakistan experienced limited demand for seaborne scrap due to weak downstream demand. In Bangladesh, civil unrest from student protests disrupted market activities. Turkish mills showed limited interest in scrap due to the availability of more cost-effective billets.

Japanese export offers declined due to the JPY’s recovery against the US dollar and subdued demand from key importers. Tokyo Steel lowered scrap procurement prices three times this week. Similarly, China’s Shagang Steel reduced scrap procurement prices twice in July due to weak market sentiment.

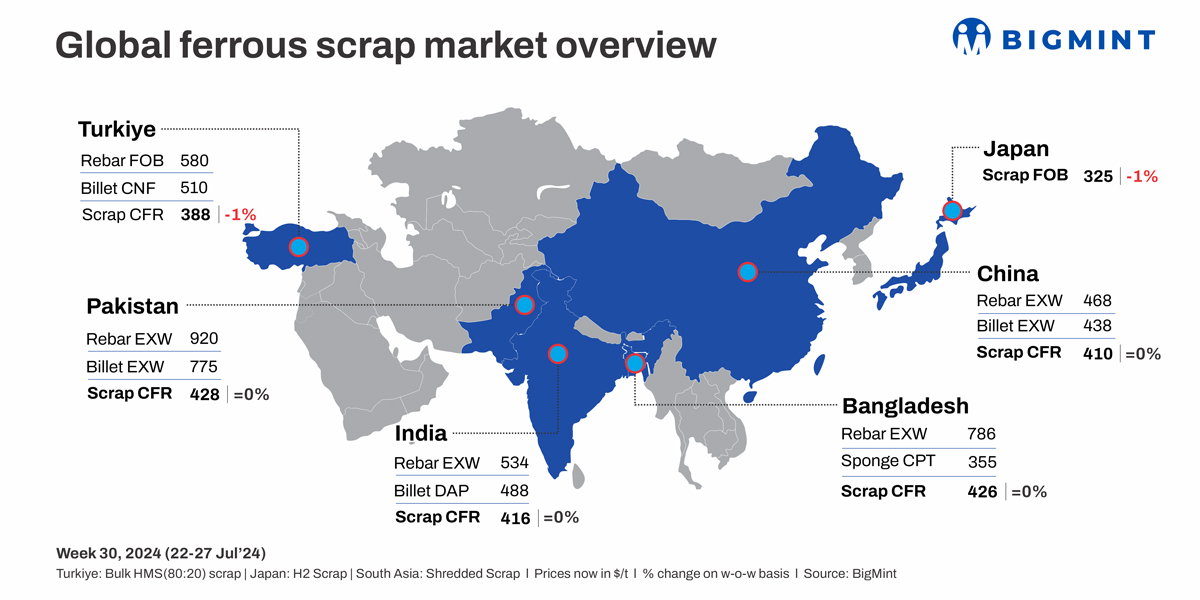

Turkiye: The Turkish imported ferrous scrap index dropped $3/t w-o-w amid bearish sentiment and anticipated price declines. A weak global and Turkish finished steel markets are increasing concerns, while Turkish mills prefer billet imports over scrap, pressuring prices. Scrap sellers face a choice between maintaining prices or offering discounts, with expected intensified pressure from mills. Around 3 to 4 deep-sea bulk scrap deals heard from the US and Europe this week. Turkish mills are restocking deep-sea scrap for late-August shipments, despite weak finished steel sales.

US scrap remains $5-6/t pricier than European material. Shredded scrap from Germany and the Netherlands is around $340-350/t, and HMS at $310/t. Egyptian demand supports Turkish scrap prices. Export rebar quotes remain weak, with offers at $580/t FOB for August shipment, slightly down from $582-585/t FOB a week ago. Domestic ship scrap prices also held steady at $370-385/t.

India: This week, India’s imported scrap market saw a marked decrease in activity due to a significant price disparity between suppliers’ offers and buyers’ bids, resulting in almost no trades. Both buyers and suppliers were at an impasse, with the latter ceasing offers to India in favour of more lucrative domestic markets in the UK and Europe. The domestic steel market’s slowdown and ongoing volatility further dampened demand.

The announcement of the FY24-25 budget, which maintained nil import duties on ferrous scrap, did little to revive interest. The bid-offer gap remained wide, with buyers finding current import price levels unviable compared to domestic scrap, which was more cost-effective. The gap between imported and domestic scrap prices was around INR 3,000-3,500/t, pushing buyers towards more affordable domestic scrap.

Reports from various trading representatives highlighted the poor market conditions and lack of significant buying activity. Despite some inquiries, particularly from regions like Gujarat, there were no suppliers willing to meet the buyers’ desired prices. This week underscored the preference for domestic scrap and the ongoing challenges in aligning international scrap prices with local market realities.

Weekly average offers for shredded scrap from the UK/Europe were assessed at $414/t CFR Nhava Sheva, while HMS 80:20 at $387/t CFR, down by $1/t and $2/t respectively.

Pakistan: This week, Pakistan’s imported scrap market experienced limited demand, primarily due to sluggish rebar sales and squeezed margins. Indicative offers for shredded scrap were consistent, with prices from the UK/Europe at $425-430/t CFR Qasim, the US at $420-425/t CFR, and the UAE at $435/t CFR. The domestic market reflected similar challenges, with local scrap prices at PKR 152,000-155,000/t and rebars at PKR 255,000-260,000/t.

A steel mill official highlighted low sales and delayed payments contributing to low market sentiment. However, market participants expressed cautious optimism for improvement following recent IMF approval, which might resolve letters of credit (LC)-related issues and support a potential recovery.

Bangladesh: Bangladesh’s imported ferrous scrap index remained range-bound w-o-w with containerised shredded and HMS (80:20) offers from Europe rising slightly due to higher freight rates. However, workable levels are $5-8/t lower. Australian suppliers noted a significant drop in inquiries from India and Bangladesh due to high freight costs, with rates from Australia to Bangladesh reaching $2,000 per 20 foot and 40 foot container.

Indicative offers for shredded scrap from Europe are $422-426/t CFR, and HMS (80:20) is $403-408/t CFR. US bulk scrap prices rose $2-3/t, and Japanese H2 scrap increased $3-4/t. Rebar prices in Chattogram and Dhaka dropped by BDT 1,000/t, while domestic shipyard scrap prices rose to BDT 61,500-62,000/t exy Chattogram.

Domestic disruptions from student protests and the monsoon have hindered scrap movement and collection. Curfews and internet outages are impeding communication and new inquiries. Despite this, steel mills in Dhaka are maintaining production, though sales and deliveries are affected.

Japan: This week, Japanese H2 scrap export offers have decreased further due to the appreciation of the JPY against the US dollar. Despite this, seaborne demand remained sluggish. BigMint’s weekly assessment of Japanese H2 scrap export offers stood at JPY 50,000/t ($323/t) FOB Tokyo Bay, down by JPY 400/t ($3/t) from the previous week’s JPY 50,400/t ($326/t) FOB.

Tokyo Steel has cut domestic ferrous scrap procurement prices for the third time this week. New prices at Okayama, Takamatsu and Utsunomiya plants are at JPY 49,000/t ($319/t), JPY 48,700/t ($317/t), and JPY 51,000/t ($332/t) respectively. Overall, during the week prices fell JPY 500/t ($3/t) at Tahara, JPY 1,000/t ($7/t) at Utsunomiya, and JPY 1,500/t ($10/t) at Okayama.

Vietnam: Offers for H2 scrap from Japan have climbed, influenced by the appreciation of the JPY, reaching $370/t CFR Vietnam and some suppliers quoting up to $385/t CFR. However, Vietnamese mills have shown limited interest due to weak steel demand, driven by reduced construction activities during the monsoon season.

Meanwhile, Vietnamese steel mills have shown a preference for US-origin bulk HMS (80:20) at around $370-375/t CFR Vietnam. However, suppliers have been unwilling to meet these price expectations.

Vietnamese domestic scrap prices remained stable in the week reflecting steady demand. In northern Vietnam, prices for domestic Type 1 or H2-equivalent 3-6 mm scrap held steady at VND 9,250-9,500/kg ($363-373/t). Similarly, prices for the same grade in the south stayed within a range of VND 8,500-8,750/kg.

South Korea: South Korean mills remained uninterested in seaborne scrap due to accumulating inventories in the domestic market. Domestic scrap prices in Korea held firm, with POSCO and Hyundai Steel raising scrap procurement prices by $7/t last week. Market participants expect scrap demand to improve before the Liberation Day holidays, as major mills tend to restock ahead of the holidays.

H2-equivalent Light A grade scrap stayed within a range of KRW 380,000-390,000/t ($275-282/t) for the week, while Heavy A grade scrap remained steady at KRW 410,000/t.

This week, the combined ferrous scrap inventory of eight major South Korean steel mills reached 815,000 t, marking a slight 1% increase from the previous week’s 807,000 t.

China: Shagang Steel has reduced its ferrous scrap procurement prices by RMB 150/t ($21/t) for all grades this week. Under the new pricing structure, HMS (6-10 mm) is now priced at RMB 2,640/t ($364/t), including 13% VAT. Notably, this marks the company’s second price cut this week.

Leave a Reply