The US East Coast scrap export index softened as export prices declined slightly due to fewer inquiries from Turkiye, where cheaper billets are available. Meanwhile, demand in the US domestic market weakened due to slow construction activities during the summer break.

The reduction in ferrous scrap collection and increased labour costs are further straining the supply chain, making it difficult to control price increases. Market factors influencing specific scrap grades continue to vary, but the underlying theme of lower scrap supply continues to underpin expectations for the next US ferrous scrap trade.

The US scrap steel prices may rise in August amid tight supply caused by extreme heat and rising labour costs. The historic last-minute replacement in the lineup for the 2024 presidential election failed to faze the US steel market.

US steel mills may be forced to prioritise securing ferrous scrap tonnes over relieving pressure on cost structures, with the scrap market likely to remain supply-driven in August, according to market sources.

In the finished steel market, the US hot-rolled coil (HRC) prices have been declining, impacting prime scrap grades in recent months. Sources indicate that HRC prices may continue to fall due to weak demand and depressed risk appetite. However, as the market nears its bottom, HRC may not significantly influence the busheling market in August, with more focus shifting to automotive production.

The local mill’s weekly consumer spot price for HRC remained stable at $650-660/t at the start of this week.

Auto sector outages across multiple US plants in late June and July, estimated to have reduced July’s auto sector capacity by approximately 21%, could ease stock pressure, allowing for production increases but also reducing busheling availability.

Few in the steel market will change their vote in November due to Vice President Harris leading the ticket instead of President Biden and the United Steelworkers labour union expressed gratitude to President Biden and vowed to continue his mission for a brighter future for everyone.

Export market scenario-

US-origin bulk scrap bookings for Turkiye remain relatively slow towards the weekend as a total of three bulk cargo booked from the US, lower as compared to last week’s four to five bulk deals.

US-origin HMS (80:20) at $390/t was sold to an Aegean region mill and another US-origin HMS (80:20) at $390/t was sold to a Mediterranean region mill.

US-origin 30,000 t mix scrap (10,000t each of HMS (90:10), shredded, and bonus) at $392/t and $410/t sold to a Mediterranean region mill.

Assessments

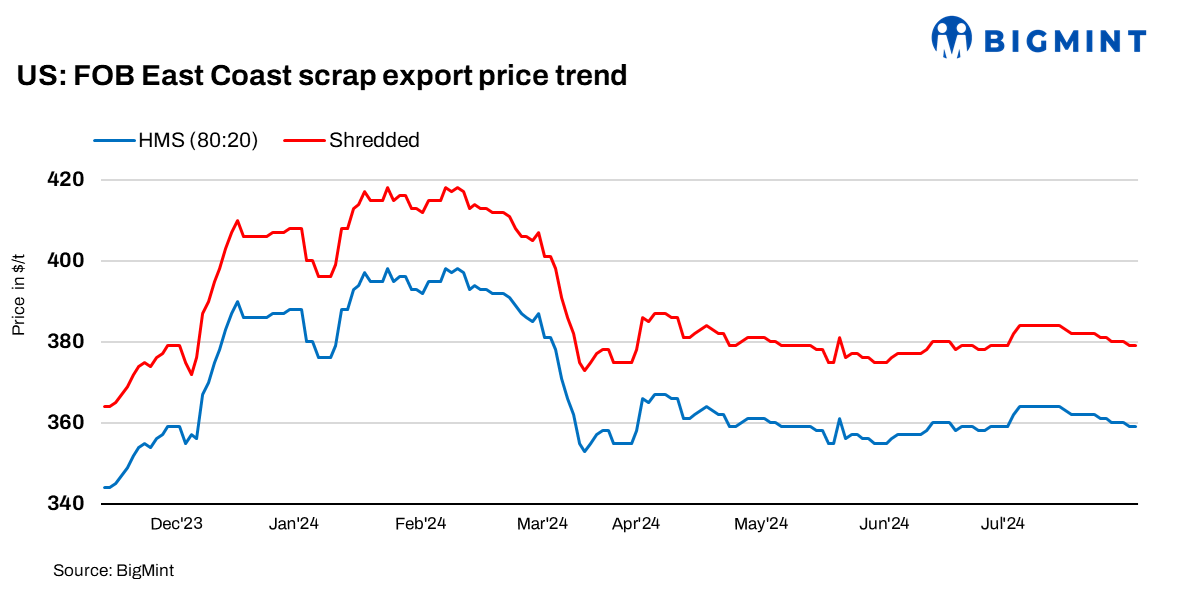

BigMint’s assessment for HMS (80:20) bulk FOB east coast decreased by $2/t w-o-w to $359/t on Friday from $361/t a week ago.

BigMint’s assessment for shredded bulk FOB east coast decreased by $2/t w-o-w to $379/t on Friday from $381/t a week ago.

Outlook: With President Biden dropping out of the presidential race, the US steel market is turning its attention to policies rather than personalities. Competition for scrap from Turkiye is expected to support HMS and shredded grades, especially as US mill utilisation remains healthy. Sources suggest that material will likely continue to flow toward the US East where prices remain favourable in export markets.

Leave a Reply