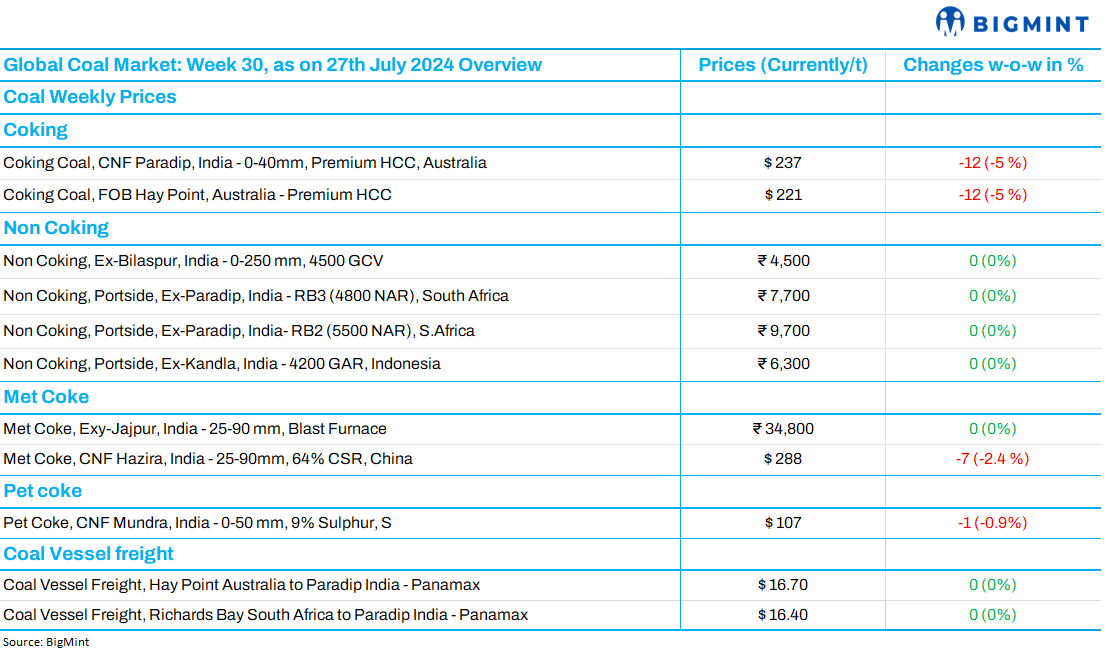

- Portside prices of South African, Indonesian non-coking coal stable w-o-w

- Australian coking coal prices dip 5% w-o-w

- Imported pet coke prices to India inch down

South African portside prices stable w-o-w

Prices of South African RB2 (5500 GAR) coal in the Indian market remained steady at INR 9,650/t ex-Gangavaram, marking a three-month low, according to BigMint data. Prices of thermal coal remained subdued for the week amid waning demand. The ongoing monsoon in India has led to reduced coal consumption across regions. Industrial demand has also slowed, as infrastructure projects are on hold until the monsoon ends, which has resulted in limited coal imports.

Indonesian thermal coal portside prices remain supported w-o-w

Indonesian thermal coal portside prices have remained largely stable in Chinese markets. Buyers here showed interest in coal, particularly due to soaring temperatures and rising power consumption. Supply issues and domestic demand in producing countries are also influencing the market. Meanwhile, in India, prices of the 3400 GAR at Navlakhi Port were stable at INR 5,200/t.

Indonesia’s benchmark coal prices increase in July

Indonesia’s benchmark coal price index, known as Harga Batubara Acuan (6,322 kcal/kg GAR), rose by 6% m-o-m in July 2024, reaching $130/t. Prices of the 5,300 kcal/kg GAR were at $91.85/t, while the 4,100 kcal/kg GAR and 3,400 kcal/kg GAR grades were at $56.09/t and $36.22/t, respectively.

Indian met coke prices stable amid awaited DGTR decision

Indian met coke prices remained stable at INR 34,800/t in the eastern region, with western prices dropping to INR 32,700/t. Indian met coke prices are expected to see decline with sentiments remaining bearish due to weak steel prices. The met coke and coking coal markets are expected to face continued downward pressure in the near term on subdued trades and low buying interest. The scenario is being compounded by the impending DGTR import recommendations.

Australian coking coal prices down 5% w-o-w

Australian premium hard coking coal prices fell by 5% w-o-w to $218/t FOB and $234/ t CNF on 26 July. The persistent oversupply has weakened market sentiments. Coking coal prices fell on low demand and sufficient supply. Asian buyers are showing limited buying interest and are hesitant to commit to procurement plans due to the steady decline in coking coal prices. Traders indicated that with supply exceeding demand, further price drops are inevitable. Also, reselling interest in the market was seen and expected further price falls in the market are keeping transactions on the lower side.

Imported pet coke prices inch down in India

Prices of imported pet coke (6.5% S) in the international market decreased slightly w-o-w, leading to lower offers for India. Current prices are now at $107-108/t CFR on the west coast and $109-110/t CFR, east coast.

Bulk coal vessel freight rates largely stable w-o-w

Coal vessel freight rates were mainly stable w-o-w. Notably, most traders preferred offering cargoes over securing stocks. Low demand in the domestic sponge and billets market has offset the impact of supply disruptions in South African coal and the limited availability of Australian cargoes. As per BigMint’s assessment, freight rates from Port Hay Point to Paradip were recorded at $17/dry metric tonne (dmt), inching up by $0.07 w-o-w. Freight rates from the Richards Bay Coal Terminal (RBCT) to Paradip are currently at around $16/dmt, up by $0.02/t w-o-w.

Leave a Reply