- Crude steel production growth rate higher than iron ore’s

- Iron ore also rides higher sponge iron production in H1

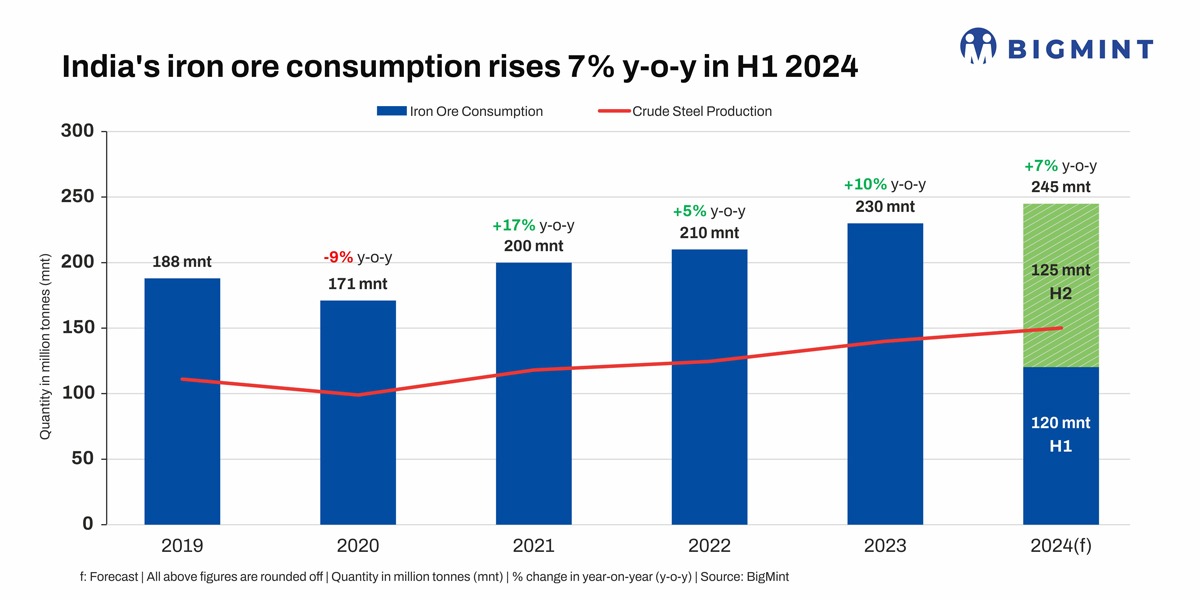

- Iron ore consumption may touch 245 mnt in CY’24

Morning Brief: India’s iron ore consumption was recorded at around 120 million tonnes (mnt) in the first half of calendar 2024 (H1CY’24), a modest increase of 7% compared to 112 mnt seen in the same period in CY’23, as per data compiled by BigMint.

Factors that impacted iron ore consumption

Higher crude steel output: India’s crude steel production rose at a higher pace of 10%, compared to iron ore consumption, to around 74 mnt in H1CY’24 against 68 mnt in H1CY’24. Within this quantum, the share of the blast furnace-basic oxygen furnace (BF-BOF) route remained static at 31 mnt, while EAF’s contribution went up by a mere 1 mnt to 16 mnt. Induction furnace (IF) mills’ share rose a significant 24% to 27.2 mnt from around 22 mnt in H1CY’23.

This indicates that a large chunk – of 43 mnt – of crude steel output was contributed by the EAF-IF mills in H1CY’24, which was a 17% increase over 37 mnt in H1CY’23.

Both EAFs and IFs are heavy consumers of sponge iron, and ferrous scrap.

DRI production rises: Data shows that India’s DRI production shot up 13% y-o-y in H1CY’24 to 27 mnt against 24 mnt in H1CY’23. The rise in DRI production can be attributed to two reasons. One, the increased contribution of the EAF-IF sector to India’s crude steel production. Secondly, sponge units saw a decrease in the cost of production. Thermal coal, particularly of South African origin, are best suited for Indian sponge-making. Average prices of the 4800 NAR RB3 grade, portside Gangavaram, dropped 20% in H1CY’24 to INR 7,978/t ($95/t) compared to INR 9,955/t ($119/t) in the same period last year. Similarly, the same grade, CNF Gangavaram, declined 16% to $90/t against $107/t in this period.

It may be mentioned that the DRI segment is a huge consumer of iron ore in the form of pellets as a key feed.

Scrap consumption up: However, data also reveals that scrap consumption has risen a significant 16% in H1CY’24 to over 17 mnt from 15 mnt in H1CY’23, even though its share in the entire raw material mix is far lower in comparison to iron ore. However, imported scrap consumption fell a considerable 26% in H1CY’24 to 4 mnt (from 5 mnt in the same period last year). On the rebound, domestic scrap consumption rose a steep 39% to 14 mnt (9.7 mnt) amid an increase in domestic generation and availability, even though prices of both imported and domestic fell y-o-y in H1.

Outlook

India’s crude steel production in H2CY’24 is expected to rise at a higher rate considering that a stable government is in place and the new Budget has kept the infrastructure spend target unchanged at INR 11.11 trillion (as given in the Interim Budget, 2024). A turnaround in demand is expected especially from Q4 (January-March, 2025) which, along with a possible drop in exports from October, will support the higher output. BigMint thus expects India’s crude steel production to rise another significant 76 mnt in H2CY’24 taking the total to an estimated 150 mnt in CY’24. Correspondingly, India’s iron ore consumption is likely to rise to 245 mnt in CY’24, with an increase of 125 mnt in H2.

BigMint will be hosting its 7th Iron Ore & Pellet Summit, to be held over 22-23 August, 2024 in Gurugram, Haryana. Be ready to attend the session on “How is India Readying Itself to Fulfill the Rising Iron Ore Demand?” Invigorating discussions on demand-supply dynamics, policy pulls and pressures, pricing and a lot more are on the cards. Register now!

Leave a Reply