- Top four provinces continue to see y-o-y declines

- Govt seeks emission curb targets from provinces

- June-July may see further decline in production

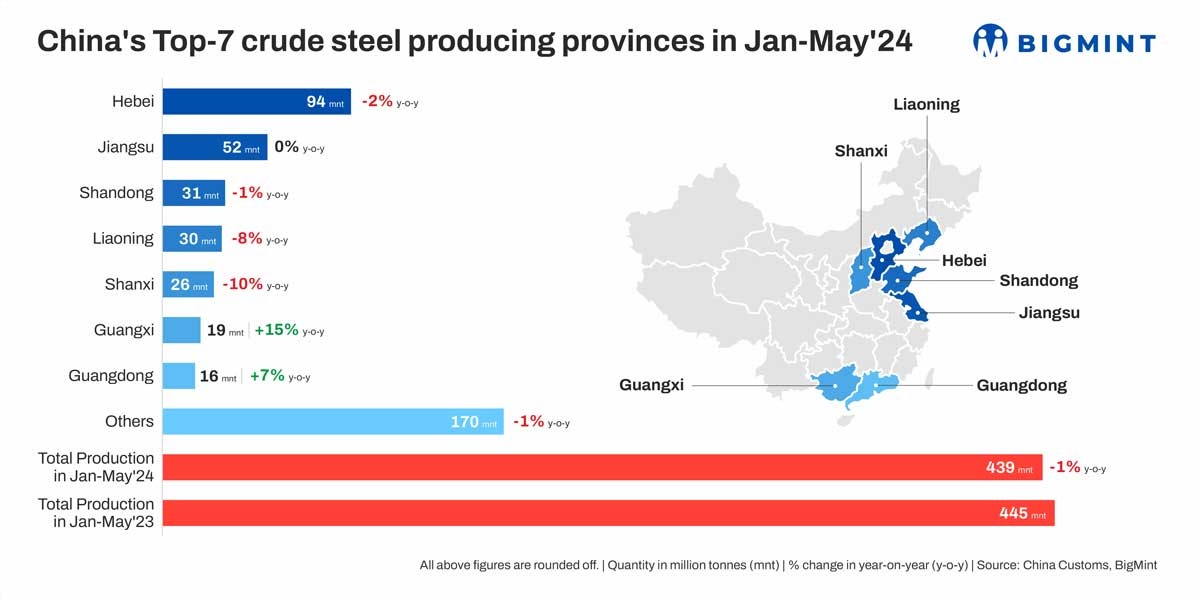

Morning Brief: Four amongst China’s top seven steel-producing provinces continued to show a y-o-y decline in January-May, 2024, reveals data maintained with BigMint. Overall, volumes dipped 1% to 439 million tonnes (mnt) in this period from 445 mnt seen in the same five months in 2023.

It may be mentioned that China’s crude steel production rose a surprising 1.6% in January-February, 2024. But, from March onwards started registering a decline. For instance, as per worldsteel, over January-March, the decline was 1.9% y-o-y. January-April recorded a 3% drop with the trend extending into January-May, albeit at a slower pace.

However, production in May 2024 was up 2.7% y-o-y.

Province-wise break-up

Hebei, the largest producer amongst the seven, after showing flat growth over the first two months of the year, started declining from March and recorded a decline of 2% to 94 mnt over January-May. Jiangsu, the second-largest producer, saw volumes remaining flat y-o-y at 52 mnt.

Shangdong (-1%), Liaoning (-8%), and Shanxi (-10%), continued to decline y-o-y with a total production of 87 mnt (92 mnt in 2023). Production at Guanxi and Guangdong rose 15% and 7% respectively with their combined contribution at 35 mnt (32 mnt).

Factors that impacted China’s crude steel output in Jan-May’24

Rising inventories warrant production cuts: China’s domestic steel market experienced a slight recovery in May 2024, which allowed production to spurt 2.7% y-o-y last month. This uptick was driven by supportive government policies, relatively stable end-user demand, and cost-control measures. Supporting this observation was the fact that The China Iron and Steel Association (CISA) reported a drop in inventories at key mills in late May by over 8% m-o-m and 7% y-o-y which allowed the decline rate in output to slightly decelerate in the period under review.

However, mills had been nursing inventory gluts in the initial three months of 2024, which rose to the highest level of 20 mnt in mid-March. Thus, mills were forced to cut production to allow for stock depletion which did happen in end-April as well as May.

Persistently low domestic demand: Despite the several real estate-related measures announced recently, the property sector, the largest consumer of steel, is still feeling the heat. Supply exceeds demand. In end-April, inventory had climbed up 16% y-o-y. Thus, many feel the recovery will be slower y-o-y as consumer confidence is still low.

Mills see loss in revenues: Another key reason for the production cuts lies in the fact that mills have been nursing squeezed margins for months now amid the low demand and eroded steel prices, which they are looking to assuage somewhat through production cuts. Benchmarked HRC prices in Tangshan fell 7% and rebar by 6% in January-May 2024.

In this period, China’s steel industry saw a 3.3% y-o-y decline in revenues. The operating cost for this period also decreased y-o-y by 3%. But, despite the decrease in costs, the industry incurred a loss of RMB 12.72 billion ($1.75 billion).

This scenario encouraged maintenance and shutdowns of several blast furnaces across mills.

Exports slow down: China’s steel exports are showing a slowdown in their growth momentum. Data collated by BigMint reveals, exports over January-May, 2024 grew a slower 23% y-o-y compared to the 30% seen over January-February and 28% in Q1CY’24 (January-March). Over January-April, exports rose 25%. The government is adopting a conscious strategy to stress on high-value, special steels rather than commercial grades. In the latter, bulk of the production happens, but where export offers have seen steady erosion in value amid bleak global demand.

Govt seeks production cut targets: China is once again resuming its strategic focus on reducing emissions. The National Development & Reforms Commission (NDRC) recently mandated each province to submit their production reduction targets by 20 June, 2024. Plans are afoot to reduce about 53 mnt of steel industry CO2 emissions by 2025. Around 15% of crude steel production capacity has not yet reached the benchmark in terms of energy efficiency.

Thus, China has also issued special action plans for energy conservation and carbon reduction in four industries, including steel which is one of the leading polluters.

Outlook

More production cuts are possibly in the offing over June-July as end-user demand remains bearish. The declining prices are not incentivising mills on production either. It seems, even if some blast furnaces are brought back into production, a larger number will be taken off in July.

Leave a Reply