- Subdued pellet demand from China

- Sellers waiting for favourable export prices

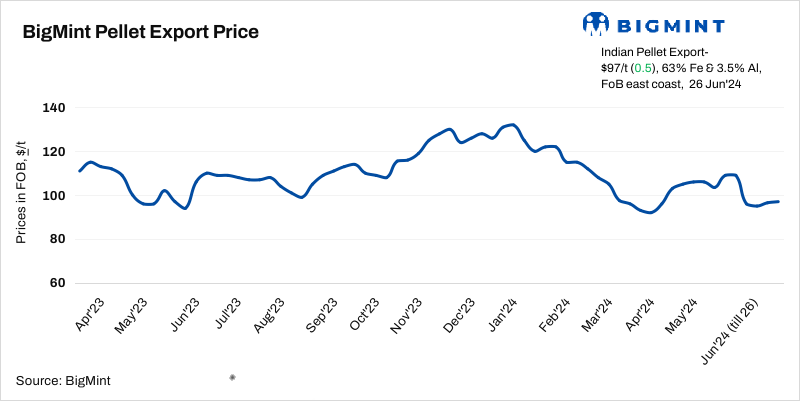

BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) inched up by $0.5/t w-o-w to $97/t on 26 June 2024. An eastern India-based pellet producer concluded last week an export deal for 60,000 t of pellets (Fe63%, 8% SiO2+ Al2O3) at around $116-117/t CFR China for July, 2024 shipment. However, no other sellers’ deal was recorded as Indian pellets demand remained weak in the Chinese market as mills were seeking cheaper material.

The overseas market for seaborne pellets remained range-bound as most of the producers did not receive a viable bid for pellets. The Chinese buyers still stood on the lower bids to keep a favourable import margin. Only a single pellet cargo deal was concluded by an Odisha-based pellet producer in the last one week, as per data maintained by BigMint.

An Odisha-based producer said that domestic pellet prices sharply dropped in June following weak sponge and steel markets. Export prices were also not favourable therefore domestic and export gap has been reduced amid a sharp drop in the Indian domestic pellet prices in the central-eastern regions.

However, domestic prices are still around INR 900-1,000/t ($11-12/t) higher than export realisations. Pellet (Fe 63%) prices in Barbil fell by INR 600/t ($8/t) w-o-w to INR 7,450/t exw ($89/t). However, ex-plant realisation for pellet exports in Barbil was recorded at INR 6,500/t exw ($78/t).

An exporter commented that the market increased by around $2-3/t today. However trades remained sluggish amid bid-offers disparity and buyers’ thinner interest for the Indian premium material.

As per sources, the current lump premium is slightly higher in the China market, making pellets a more cost-effective option, but Chinese steel mills’ procurement of lump remains driven by essential demand. The Chinese buyers preferred cheaper iron ore fines for the production margin on the other side Indian pellets remained under pressure.

Rationale:

- One (1) pellet export deal was recorded in this publishing window but not taken under price calculations. Hence accorded 0% weightage in the index calculation Click here for detailed methodology.

- Twelve (12) indicative prices were received and all were considered for calculation of the index and given a 100% weightage.

What factors affecting pellet export market?

- Iron ore fines down w-o-w: The benchmark iron ore fines index decreased w-o-w by around $2/t to $104/t CFR China on 25 June. Prices were driven by weak buying interest and low demand. Steel mills primarily purchase on a need-basis as finished steel demand shifts to off-peak periods. Due to improved import margins, mills are increasingly procuring from the seaborne market and selling existing port cargoes.

- DCE futures stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2024 contract remained stable w-o-w at RMB 826/t ($113/t) on 26 June, 2024. On a d-o-d basis, future prices increased by RMB 25/t ($3/t) against RMB 801/t ($109/t) yesterday.

- Portside pellet prices stable w-o-w: Chinese sources said that Qingdao portside offers for Indian pellets (Fe 63.5%) remained stable w-o-w at around RMB 990/t ($135/t), inclusive of all import taxes and port charges. However, prices rose by RMB 20/t ($3/t) d-o-d.

- Pellet inventories stable w-o-w: Pellet inventories at China’s major ports remained stable at 6.5 mnt on 20 June, 2024 compared to the last week, according to SteelHome data.

Outlook

Pellet export offers in the seaborne market are anticipated to remain under stress in the near term too due to slowdown in China and insufficient margins for pellet imports.

Leave a Reply