- Lacklustre trading activities amid lower buying interest from China

- Bunker prices see an upward movement this week

Dry bulk iron ore freight rates exhibited diverse trends this week on key routes. Notably, inquiries for iron ore in the global market have slowed down amid lower buying interest from China. Meanwhile, scarcity of pacific cargo volumes and lower trading activities have been recorded in global markets. Furthermore, some shipbrokers are out of the market amid weak sentiment of iron ore export activities.

One of the shippers informed ,”Cargos are shifting to other commodities owing to fewer demand for iron ore from China led the vessel freight supported this week.”

Spot prices of iron ore fines (Fe 62%) inched down by $3/tonne (t) w-o-w to $103.8/t CFR China on 11 June, 2024 following weak market fundamentals post-Dragon Boat festival despite the strong buying interest. The upcoming rainy season will have a significant impact on transportation and outdoor construction at downstream sites.

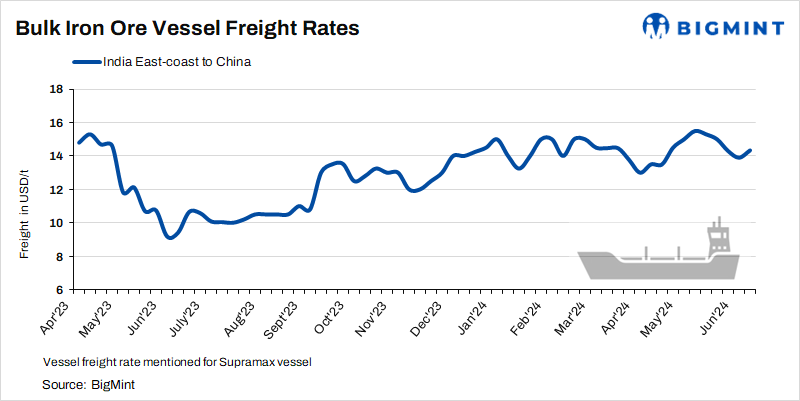

Asia-Pacific Supramax dry bulk (50,000-55,000 t) freight rates for an iron ore vessel from the east coast of India to China rose by $0.44/t this week to $14.34/t on 12 June, as per BigMint’s assessment.

Route-wise freight specifications:

- India-China: Freight rates from the Indian Ocean to China increased this week. As per sources, a miner have booked a cargo from East coast of India to China at a freight of around $14.34/t for end June shipment, sources informed BigMint.

- Australia-China: Australian mining company Rio Tinto is actively seeking tonnages for end-June shipments at levels of $10.85/t. Limited inquiries have been witnessed for end-June deliveries, which are still under negotiation. Meanwhile, freight rate from the Australia-to-China route have dropped this week by $0.24/t to $10.76/t today. Notably, Australia’s iron ore and pellet export shipments marginally rose by 2% y-o-y to 347 million tonnes (mnt) in January-May 2024 compared to 340 mnt in Jan-May 2023, as per vessel line-up data maintained with BigMint. Meanwhile, shipments rose by 8% m-o-m to 74.6 mnt in May, 2024 compared to 69.3 mnt in April, 2024. As per sources, Rio Tinto booked one Capesize vessel from Dampier, Australia to Qingdao Port, China, at $10.85/t, for 25-27 June shipment.

- Brazil-China: Enquiries in the Pacific region have been seen this week. However, freight rates have seen a slight increase this week. A Capesize vessel was seen booked for shipments in the first week of July at freight rates of around $25.65/t. Brazil’s iron ore exports dropped by 6% y-o-y to 32.83 mnt in May, 2024 compared to 35.04 mnt in April, 2023, as per Customs data. However, volumes increased by 21% m-o-m as against 27.2 mnt in April.

- South Africa-China: Freight rates from Saldanha Port to Qingdao have increased this week. However, an enquiry for a Capesize vessel for mid-June shipment is under negotiation. South Africa’s iron ore exports rose by 13% m-o-m to 5.41 mnt in May, 2024 compared to 4.77 mnt in the previous month, as per vessel line-up data maintained with BigMint. China was the largest importer at 1.97 mnt followed by South Korea at 0.47 mnt.