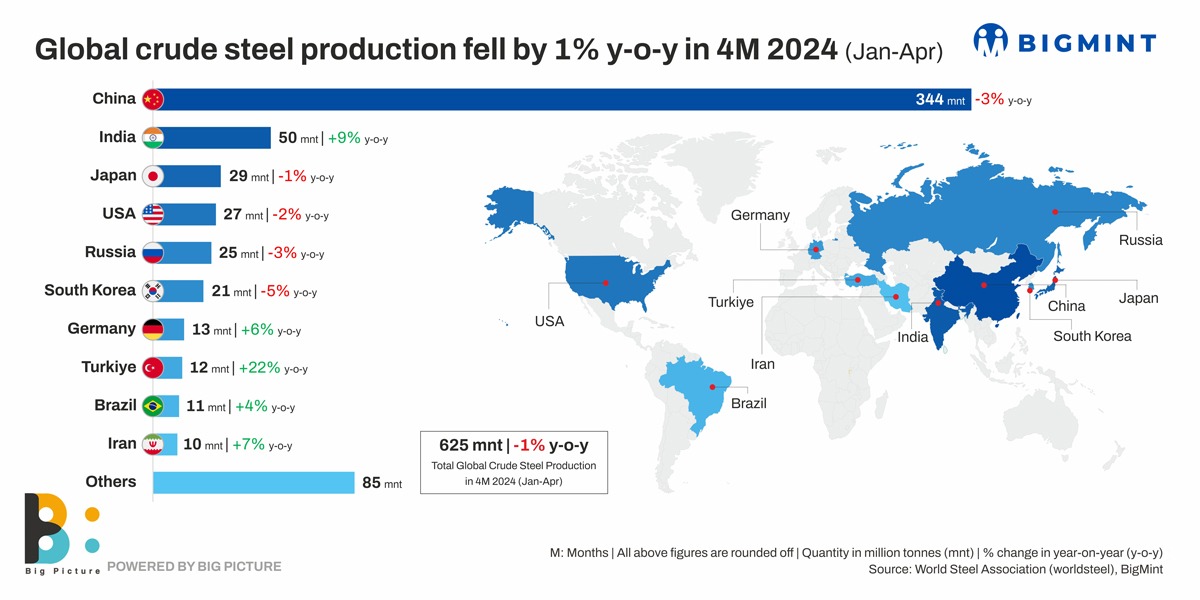

- China reduces output to deplete inventory

- India bucks trend on decent domestic demand

- Korean mills opt for maintenance shutdowns

Morning Brief: Of the top ten crude steel-producing countries, five showed a decline over January-April, 2024.

Notable amongst the ones who bucked the trend were India and Turkiye.

China’s production cuts necessary for inventory depletion: The world’s largest steel producer and guzzler showed a 3% decline over the period under review to 343.70 million tonnes (mnt). April too showed a 7.2% decline y-o-y to 85.9 mnt. The production drop was necessary for inventory depletion while it also dovetails with China’s net zero efforts. Mills have been nursing squeezed margins for a protracted period amid the sustained low demand from the real estate and construction sector, which consumes the lion’s share of around 60% of steel. Apparent crude steel consumption decreased 4.7% y-o-y to 232 mnt in Q1 (January-March).

That apart, the lower production dovetails with the government’s emission goals of carbon peaking by 2030 and net zero by 2060. It was heard, as of April, 2024, around 136 steel mills have fully or partially completed ultra-low emission transformation and assessment monitoring.

India sees decent pre-poll domestic demand: India showed a somewhat healthier trend. Output was up 8.5% to 49.5 mnt over January-April, 2024. April’s standalone production was also up 3.6% at 12.1 mnt.

Domestic demand was better compared to overseas amid a sustained pre-election infra push. March, especially saw some pre-poll traction as buyers stocked up to avoid poll-related disruption possibilities. Even though exports were a washout, domestic realisations were higher compared to overseas offers. For instance, export offers averaged $586/tonne (t) FOB over January-April, while benchmark BF-route rebars averaged INR 52,575/t or $632/t in dollar parity and HRCs, INR 53,400/t ($641/t) ex-Mumbai, encouraging mills to focus on domestic sales.

Japan hit by low construction steel, exports demand: Japan, the third-highest steel producer, witnessed a marginal 1.2% dip in production to 28.5 mnt in January-April, 2024. April production was down 2.5% y-o-y to 7.1 mnt. This marked the second consecutive month of decline underscoring the fact that demand, both domestically and internationally are sluggish.

Construction sector demand has been subdued amid rising raw material prices and labour shortage while China has taken away Japan’s export advantage with aggressively low offers.

Poor demand from some end-users in the US: The fourth-largest steel producer saw a slight 2.2% decline in crude steel production in January-April, 2024 to 26.5 mnt. April’s output was down 2.8% y-o-y to 6.7 mnt.

Although underlying demand was stable, some key end-user segments like residential housing displayed sluggish offtake trends amid high interest rates. However, automotive, non-residential construction and industrial and energy sectors remained stable.

Korea mills undertake maintenance: The sixth-largest steel producing country, South Korea, recorded the steepest decline, at 5.1% to 21.2 mnt for the period under review, while April 2024’s production was down 10.4% to 5.1 mnt.

The drop was a result of major mills opting for maintenance shutdowns. Largest mill POSCO’s no. 4 blast furnace, which has an annual production capacity of 5.3 mnt, underwent repairs for 125 days which reduced output by 1.7 mnt. A hot rolling mill also underwent repairs for 15 days. Another major, Hyundai Steel’s 2nd hot rolling plant and 2nd cold rolling plant were put on maintenance in February. Sectors like automotive, general machinery and steel are expected to show slight growth in the second half of the year after declining in the first half, as per sources.

Turkiye sees new capacities coming onstream: Turkiye has seen a rebound in steel production since January this year. Volumes rose 22.1% to 12.3 mnt over January-April and by 4.5% y-o-y in April at 2.8 mnt. Turkish mills fought back after facing challenges like natural disasters, geo-political upheavals, rising energy prices and a sliding lira. Fresh investments, new capacities launched in the second half of 2023 and stress on value-added products for the domestic market are supporting higher production.

Outlook

China’s production and demand may hover at 2023 levels while India may continue to remain the strongest driver of demand. Housing issues may continue into 2024 for the US amid rising raw material prices, high interest rates and labour shortage. The EU may remain challenged by geo-politics, high inflation, monetary tightening, and still higher energy prices.