- Mills focus on home market amid higher realisations

- Exports to EU increase sharply as quotas get fulfilled

- SEA sees China factor, overcapacity, dipping demand

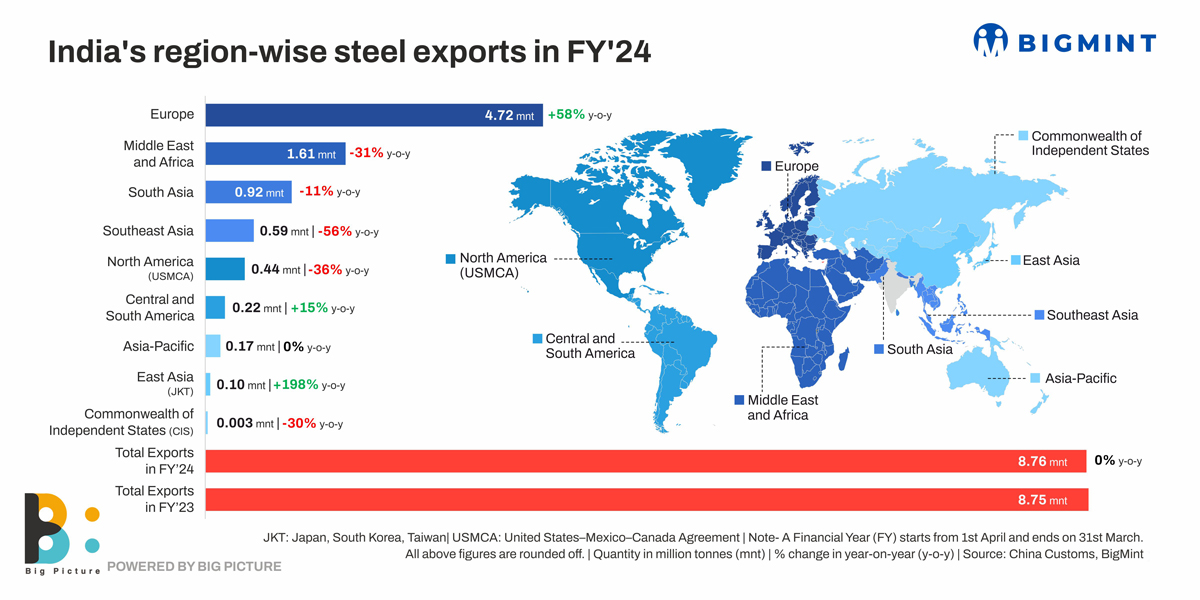

Morning Brief: India’s steel exports remained flat in financial year 2023-24 (FY’24) at around 8.76 million tonnes (mnt) compared to 8.75 mnt in FY’23. Exports to some of the key geographies showed a y-o-y fall, which kept total volumes flat.

Why did exports to some regions show y-o-y fall in FY’24?

Indian mills more focused on home demand: For Indian mills, home demand was better compared to overseas last fiscal because of a sustained pre-election infra push, and offering better realisations too. For instance, if Indian export offers averaged $596/t FOB last fiscal, then domestic realisations, in dollar parity, offered almost $673/t (INR 56,000/t) for benchmark (HRCs) and $653/t for domestic rebars (INR 54,325/t), creating a stronger case for home focus.

This allowed mills to concentrate on domestic sales rather than push for exports where offers fell steadily last year. And, data corroborate increased domestic demand. And, certain data corroborate this. For instance, reports indicate that the National Highways Authority of India (NHAI) spent a record INR 207,000 crore ($24.86 billion) in construction of national highways in FY’24, the highest-ever capital expenditure so far, and 20% higher compared to INR 173,000 crore ($20.77 billion) spent in FY’23. That apart, India’s eight core sector industries grew to a 3-month high of 6.7% in February 2024, whereas factory output hit a 16-year high in March, this year, helping the fiscal to bow out in a blaze of glory.

The automotive sector too revved up, with sales rising 9% last fiscal amid improved supply and demand. This is the first time that passenger vehicle sales crossed 4 million units.

Indias-regionwise-steel-exports-in-FY24.pdf

EU steel imports rise in Q4CY’23: Data reveals that Indian steel exports to Europe rose a considerable 58% to 4.72 mnt last fiscal compared to 2.99 mnt in FY’23.

In the fourth quarter of 2023, the EU’s steel-using sector’s output continued to grow, albeit slowed down, showing unexpected resilience despite the protracted impact of Russia’s invasion of Ukraine, global geopolitical tensions, overall manufacturing weakness along with above-average energy prices.

Although the EU’s apparent steel consumption dropped in 2023 to 126 mnt against 138 mnt in 2022, the fourth quarter saw a slight increase of 2.8% y-o-y after six consecutive drops. Steel imports into the EU reflected the demand rebound, rising 11% in Q4CY’23 although these dropped 8.5% for full year 2023.

Thus, even if demand was weak, limited supply allowed Indian steel mills to exhaust their quotas to the EU despite the fact that overall HRC offers fell to an average $726/t CNF Antwerp in 2023 from $833/t in CY’22.

Middle East & Africa volumes fall amid Chinese onslaught: Middle East and Africa emerged as a key export destination as the entire region is seeing frenetic infrastructure growth. However, Indian mills saw their opportunities slipping away into the hands of Chinese exporters who aggressively lowered their offers to capture large chunks of this market. Chinese offers to the region fell to an average $625/t CNF Abu Dhabi in 2023 compared to the Indian’s $664/t CNF Jebel Ali. Indian mills found it unviable to match the Chinese offers. Thus, Indian steel exports to this region fell 31% to 1.61 mnt last fiscal against 2.32 mnt seen in FY’23.

Southeast Asia (SEA) demand dips amid oversupply: Exports to this region fell a steep 56% to 0.59 mnt (1.32 mnt) in the year under review, Overcapacity, falling demand and Chinese imports at highly competitive offers took away this traditional market from Indian exporters.

The region’s current production capacity stands at 75 mnt, but is expected to exceed 160 mnt if all proposed projects materialize.

But steel demand in the six major countries of the Association of Southeast Asian Nations (Asean-6) fell nearly 2% y-o-y to 73.5 mnt in 2023, as per SEAISI. Asean-6’s net imports slid by 1.3% y-o-y to 24 mnt in 2023 amid contracting demand.

Lastly, Chinese rock-bottom offers spoilt Indian chances again. Chinese offers fell a significant 16% to $601/t CNF HCMC in 2023 from $716/t in 2022. Indian offers averaged $631/t CNF HCMC despite dropping 7% from 2022 levels.

US end-users hit by high interest rates: The US economy and its steel-consuming sectors were impacted by steep interest rate hikes. Particularly affected was residential construction, which is expected to contract in 2023 and 2024, although infrastructure and commercial building sectors had a better buffer. Indian steel exports to the United States-Mexico-Canada showed a 36% drop to 0.44 mnt (0.68 mnt).

Outlook

Chinese aggression on the exports front is likely to continue in the current fiscal. Demand in Europe may recover but still lag amid slack end-user demand, high interest rate, rising material costs and labour shortage. Southeast Asia is likely to feel the heat of overcapacity and Middle East may continue to be serviced by China. Thus, Indian mills may remain focused on the domestic market especially since there is optimism of a demand rebound post-elections.