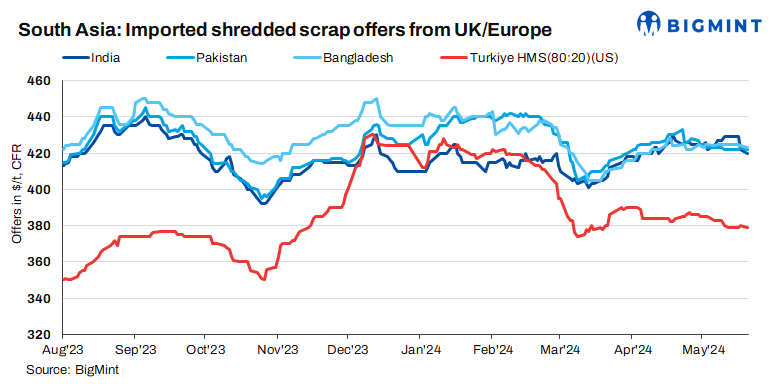

Today, the South Asian ferrous scrap market continued to exhibit sluggishness, with Indian buyers proceeding cautiously amidst bid-offer disparities. In Pakistan, the presence of cost-effective domestic scrap and sluggish finished steel sales have constrained buyer activity. Meanwhile, Bangladeshi buyers leaned towards bulk vessel purchases over containers, maintaining a steady preference. Notably, shredded scrap offers saw a $2/tonne (t) decrease in India, a $3/t decrease in Pakistan, while remaining unchanged in Bangladesh. Additionally, US bulk HMS (80:20) offers to Turkiye saw a $1/t uptick d-o-d.

Overview

India: In India, buyers have adopted a “wait and watch” approach toward imported scrap bookings due to a significant disparity between offers and bids, leading to a slowdown in purchases. With numerous bookings already made in April and the first two weeks of May, there was no rush for fresh bookings, according to market participants.

Shredded scrap offers from the US and Europe were assessed at $415-420/t CFR Nhava Sheva, while buyers’ bids were around $410/t CFR. HMS (80:20) offers were heard at $400-405/t CFR, with buyers targeting $395-400/t CFR.

Pakistan: Pakistani buyers continued to stay on the sidelines due to the disparity between bids and offers, along with the availability of cost-effective scrap in the domestic market. Additionally, poor finished steel sales have led to a slowdown or temporary halt in production at major mills.

A steel mill official stated, “Buying was nil, and sentiments are really poor. With Eid approaching, no work will be happening for the next 1-1.5 months. Production levels are at 30%, and we will take a two-week shutdown during Eid. There is almost a $20/t gap between domestic and imported scrap.”

Offers for shredded scrap from the UK/Europe were assessed at $415-420/t CFR Qasim.

Bangladesh: Bangladeshi buyers were reported to be preferring bulk vessels over containers. Containerised shredded scrap offers from the UK and Europe were assessed at $420-425/t CFR Chattogram, while HMS (80:20) offers were noted at $405-410/t CFR.

Turkiye: Turkish imported ferrous scrap prices saw a slight increase with expectations of near-term stability in a balanced market. Offers of bulk HMS (80:20) from the US were assessed at $380/t CFR, up 1/t from the previous day. The recent surge in bookings was attributed to improved rebar sales domestically, particularly in the Iskenderun region, where higher domestic rebar prices were observed. Additionally, positive developments in the Chinese market may bolster Turkish mills, with potential increases in scrap prices anticipated. While demand for scrap remains favourable compared to billet imports, sluggish rebar demand suggests limited upward pressure on scrap prices. Despite challenges such as a strong Euro hindering export competitiveness, shortsea scrap prices have shown firmness recently due to high collection costs and strong local demand.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $418/t CFR Nhava Sheva, down by $2/t d-o-d.

Pakistan: UK-origin shredded indicatives were assessed at $419/t CFR Qasim, down by $3/t d-o-d.

Bangladesh: UK-origin shredded prices were assessed unchanged at $423/t CFR Chattogram, d-o-d.

Turkiye: US-origin HMS (80:20) bulk prices were assessed at $380/t CFR Turkiye, up by $1/t d-o-d.

Outlook

In the near term, imported ferrous scrap offers in the South Asian region may experience a slight correction due to muted demand across key areas. The upcoming Indian general election results in June are expected to further disrupt market sentiments, compounding the already slow demand. Additionally, with Eid approaching in June, market participants in Pakistan and Bangladesh are likely to adopt a festive mood, resulting in limited buying activity.