- Mills focus more on higher domestic realisations

- China’s aggressive offers deterrent for Indian mills

- Europe remains tepid even as domestic prices drop

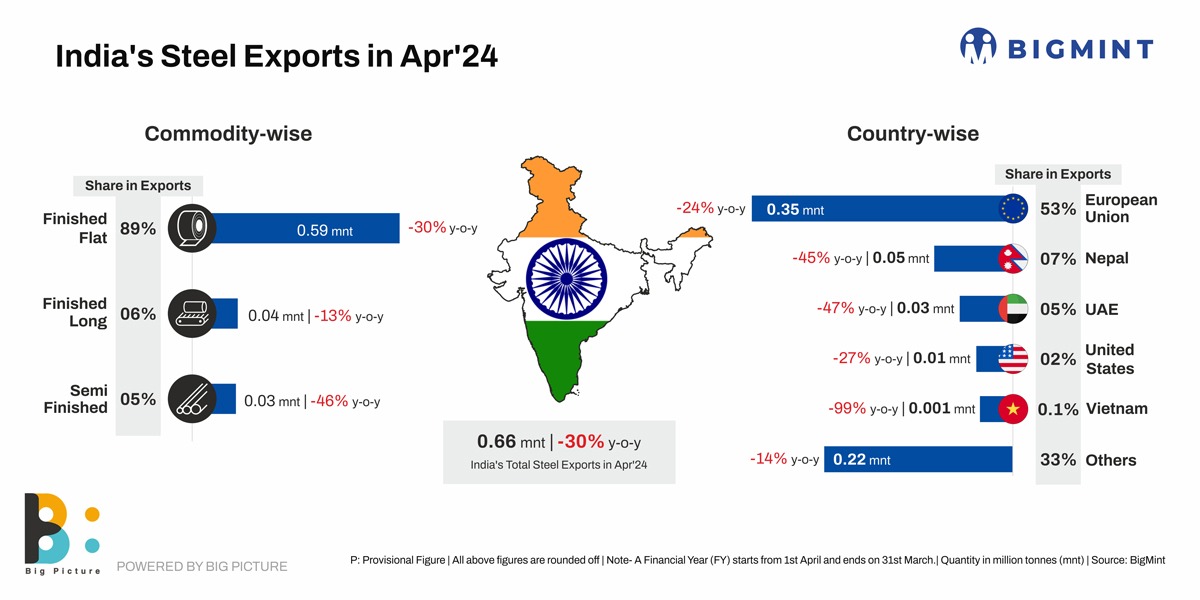

Morning Brief: India’s steel exports in April 2024 hit their lowest in five months. Volumes dropped to a provisional 0.66 million tonnes (mnt), since November 2023 when exports had touched 0.32 mnt, reveals BigMint data. M-o-m, volumes are down 35% compared to 1.01 mnt in March.

Commodity-wise break-up

Finished flats, which traditionally comprise the major portion of exports, led volumes in April too with a whopping 89% share of 0.59 mnt. However, these were down 27% m-o-m compared to 0.81 mnt in March.

Semi-finished (billets) plunged 76% to a little over 31,000 tonnes (t) from 1.30 mnt in March.

Finished longs declined a considerable 42% m-o-m to around 42,000 t (73,000 t).

Semis comprised a mere 4% and finished longs 6% of the total in April.

Country-wise break-up

Europe continued to lead the exports charts in April 2024 with 0.35 mnt (0.57 mnt). However, this dropped 38% m-o-m.

Vietnam saw volumes dropping to a dismal 500 tonnes from 91,000 t in March while those to the Middle East fell 16.5% to 33,548 t (40,184 t).

Reasons behind decline in exports in Apr’24

China factor continues to weigh on Indian mills: The China factor continued to sit heavily on Indian steel exporters. China’s exports spurted 16% y-o-y in April 2024 even though these fell 7% m-o-m. Domestic demand continued to plague mills. The real estate sector is still struggling. In April, the average daily trading volume of construction steel in 20 key cities was up 20% m-o-m, but down 2% y-o-y. The y-o-y decline in real estate investment is still a drag on construction steel demand.

The Qingming holidays in early April further added to slack consumption.

Naturally, China kept its exports ante up, to offset slow home demand.

Indian mills turn scanner on domestic sales: Indian mills, weighed down by inventory since early this year, especially in flats, strategically cut production or opted for maintenance and effected interim price hikes over the last couple of months. Although longs had seen some pre-election buying, flats had not been so lucky. The production cuts led to lesser supply and supported the price hikes, which helped to increase domestic realisations. For instance, ex-Mumbai trade-level HRC prices in April remained flat m-o-m at INR 52,630/t ($630/t) whereas export offers hovered at $562/t FOB. This encouraged mills to focus on the home market and avoid export allocations.

Declining export offers biggest challenge: China’s cut-throat pricing has been possibly the biggest challenge for Indian mills, almost pushing them out of the overseas market. For instance, in April, Chinese HRC export offers to Vietnam dropped 9% since January to $555/t CNF HCMC, whereas Indian mills and exporters found it unviable to lower beyond $567/t (also down 9% since January). Vietnamese end-buyers preferred either Chinese material or domestic, with Hoa Phat’s prices touching $553/t CIF HCMC.

Likewise, Indian April offers to the Middle East dropped 6% since January to $600/t CNF Jebel Ali but Chinese quotes fell 10% to $559/t in this period.

That apart, Japanese offers were also highly competitive. A Japanese HRC deal of 50,000-60,000 t was reportedly concluded at $580-590/t CFR for June shipments.

EU demand slow, domestic prices drop: End-user consumption in the European Union is slow. Distributors here are hesitant to make large purchases. This cautiousness has extended to spot buyers who are avoiding building up stockpiles, instead opting for smaller lots to meet immediate needs and minimize the risk of prices falling in the future. Post-Easter transactions continued to remain slow, forcing domestic HRC prices to downtrend in early April. But mills were reluctant to do later in the month amid cost pressures. This encouraged buyers to seek lower import offers. But, they were also cautious because of safeguard duty uncertainties.

Vietnam domestic prices drop: In April, Vietnamese steel major Formosa Ha Tinh reduced HRC prices by $10/t m-o-m for June-July, 2024 shipments. Subsequent to the revision, prices of SAE1006 skin pass stood at $585-595/t CIF HCMC and non-skin pass at $580-590/t CIF. But, due to uncertainties in global markets–caused by China’s rising steel futures–Vietnamese steel importers were also cautious, leading to fewer trades.

Outlook

The domestic market looks positive and BigMint heard no mill is booking exports deals at current offers as there are lesser HRCs available this month and next. Export allocations are likely to be available for only end-June or July shipments due to the outage in May and early-June.

On the other hand, Chinese mills are focused on reducing inventory which translates into higher exports and a continued challenge for Indian players.