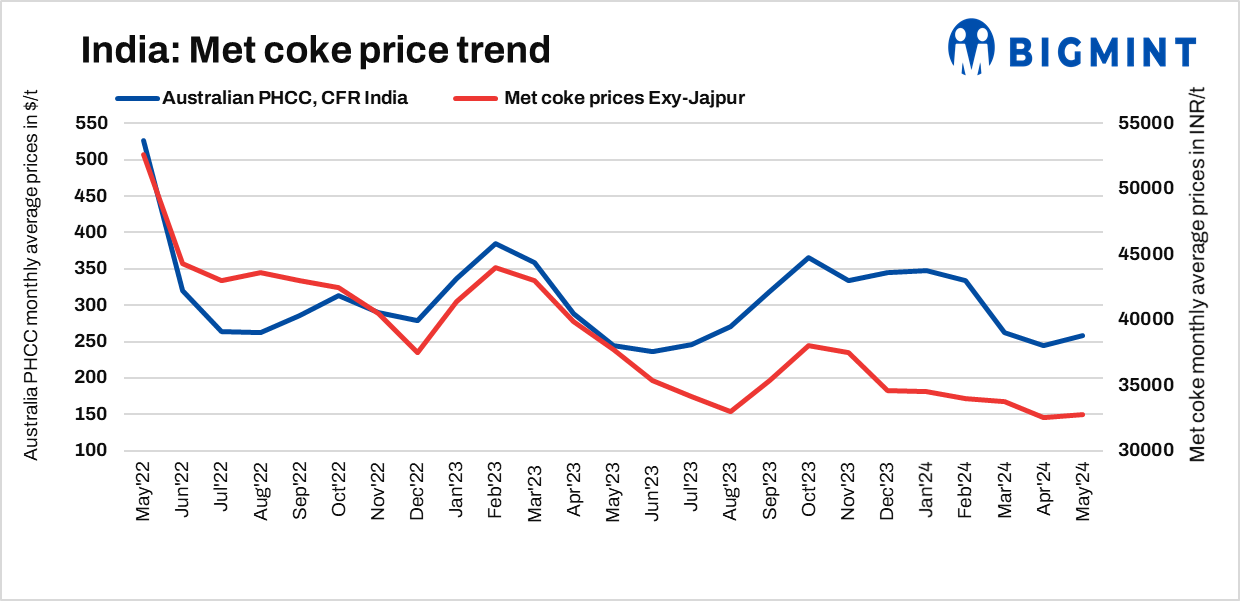

Indian met coke prices have been recorded at INR 33,000/tonne (t) ex-Jajpur, marking an increase w-o-w. Prices have picked up slightly as demand has emerged from the buyers.

Met coke prices in western India have been recorded stable m-o-m. Production remains curtailed as Indian cokeries have cut output. Met coke capacity utilisation in western India has dropped to 50% levels.

Indian coke imports have been recorded at 0.28 mnt in April as against 0.22 mnt in March 2024, as per data maintained with BigMint.

Australian premium hard coking coal (PHCC) prices stood almost stable w-o-w at $241/t FOB against $243/ t FOB on 1st May, 2024.

The metallurgical coal market experienced a slight decline towards beginning of week as sellers faced challenges in selling off their stocks, even after China resumed trading post the Labour Day holidays. The market outlook remained uncertain, prompting sellers to reintroduce floating offers.

A significant supply-demand gap persisted in the beginning of the week, with only the smaller Indian mills, which have limited needs, actively participating.

Prices picked in the middle of the week due to anticipation of strengthening steel fundamentals in both the Chinese and Indian markets. Some participants pointed to upcoming maintenance by Australian miners in July and the anticipated increase in demand from India post general election as factors driving the pricing of July-loading cargoes at a premium.

India-based buyers exhibited mainly bearish sentiment, while Chinese mills opted for a cautious approach, focusing on maintaining low inventory levels rather than rushing to secure seaborne prime coal.

Chinese mills showed a preference for purchasing seaborne cargoes that had either arrived in China or are about to arrive. Consequently, traders are primarily focusing on acquiring forward cargoes and assuming the associated risks of potential price fluctuations.

Chinese met coke prices are currently assessed at around $340/t CFR India.Following the Labour Day holidays, market participants in China have re-entered the fray, though many are adopting a cautious stance to assess market trends. International uncertainties have seeped into the CFR China market, contributing to this cautious approach. Speculation has emerged regarding the possibility of Chinese mills implementing initial cuts to met coke prices in late May due to shrinking profit margins. However, there is also talk of cokeries considering another round of price hike.

Certain mills have been heard to be rejecting the fifth price hike. The subdued sentiment in China reverberated across international markets, with Indonesian cokeries maintaining offer levels at $315-$320/t (CSR 63/64), consistent with previous weeks.

A few market participants noted limited demand for June from the Indian market, attributing it to the forthcoming monsoon season, which is expected to dampen market activity.

Indian pig iron prices rose by INR 150/t w-o-w to INR 43,800/t Durgapur on 9 May. Similarly, prices rose by INR 2,850/t w-o-w in the Raipur market to INR 44,000/t DAP.