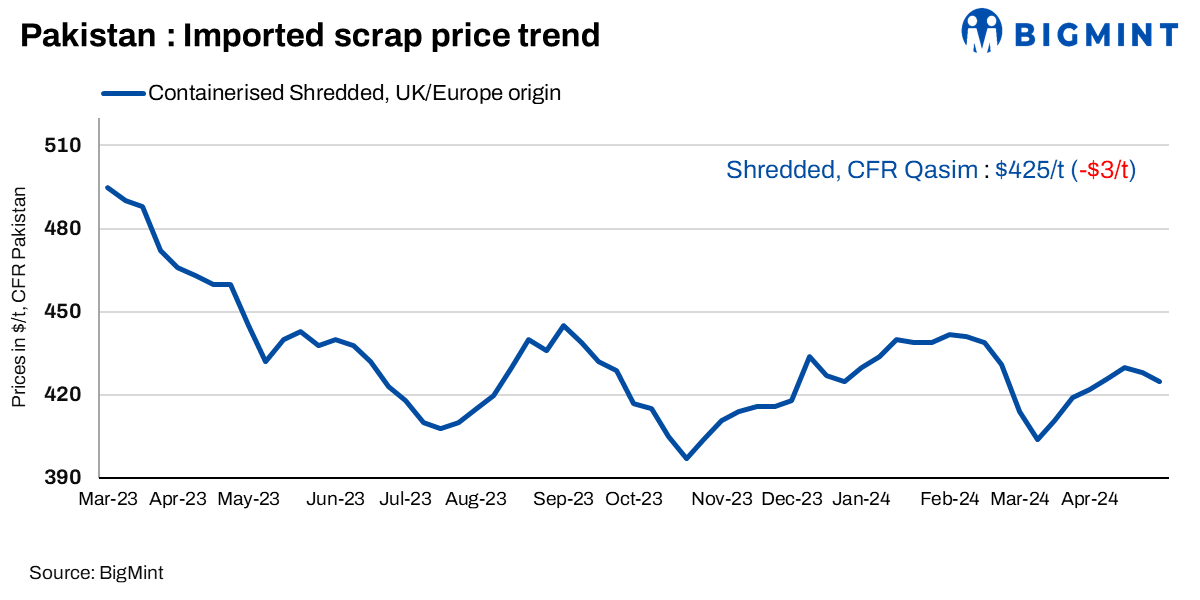

Imported ferrous scrap prices in Pakistan saw a $3/t decline over last week, with few signs of improvement. The local scrap market remains under pressure, with sluggish end-product demand and ongoing payment issues. Liquidity remains tight, contributing to the overall market slowdown.

Current shredded scrap offers declined slightly to $425-426/t, Market activity remains slow as mills are accumulating funds for paying bills with liquidity remaining a major concern.

Mills are expected to restart booking soon with slow restocking to manage production levels ahead of Eid in June. While some buyers are seeking materials for immediate delivery, others are adopting a wait-and-see approach. HMS from the UAE is offered at $410-415/t, limiting buyers’ flexibility in negotiations.

A steel mill official said, “The market is sluggish due to slow infrastructure development and a lack of major projects. Mills are focusing on accumulating funds to cover bills.”

BigMint’s assessment for Europe-origin shredded stood at $425/t, down by 3/t w-o-w.

Around 3,000-4,000 t of shredded scrap from the UK and Europe were booked at $423-427/t CFR Qasim last week.

Domestic market: In the domestic market, average rebar offers were heard at around PKR 240,000-250,000/t. Demand for finished products witnessed another dull weak with mills remaining cautious about domestic scrap procurement and declining production levels. Domestic scrap indicative offers were heard at PKR 155,000-158,000/t exw levels whereas the CC billet is priced between PKR 215,000-217,000/t.

A mill representative stated, “The market is not doing well, and mills, especially those with high leverage, are feeling the pinch of high interest rates. We are not procuring much because European domestic prices are much higher compared to PKR prices. It is hard to predict when the situation will improve. The recent MPC meeting kept interest rates unchanged, and the expectation is they will remain steady until the second half of 2024. The upcoming period will be challenging unless there is a business- or economy-friendly budget, but that is unlikely since we plan to enter another IMF programme.”

SBP receives IMF: The State Bank of Pakistan (SBP) announced that it has received the final $1.1 billion tranche from the International Monetary Fund (IMF) under its stand-by arrangement (SBA). This approval comes after the IMF’s executive board completed its second review, bringing total disbursements to about $3 billion. The IMF also recommended maintaining a market-determined exchange rate and broadening structural reforms for inclusive growth. Finance Minister Aurangzeb indicated Pakistan’s interest in a longer and larger economic bailout package with the IMF.

Outlook: Market observers suggest that while demand is expected to gradually increase, current high stock levels may limit scrap imports. Without a significant surge in demand, major scrap bookings are unlikely in the near term.