Today, the South Asia ferrous scrap market witnessed a mixed trend. In India, there was a notable surge in demand for imported scrap. This can be attributed to a temporary scarcity exacerbated by local suppliers and an anticipation of heightened demand for finished steel ahead of elections. Conversely, Pakistani buyers scaled back their purchases due to sluggish local steel demand, impacting scrap consumption. Bangladesh encountered hurdles in opening letters of credit (LCs) from banks, influencing procurement patterns.

Shredded scrap offers experienced a slight increase of $1/t in India, while dropping by $7/t in Pakistan and remaining unchanged in Bangladesh. Offers of US bulk HMS (80:20) to Turkiye also maintained stability, showing no change d-o-d.

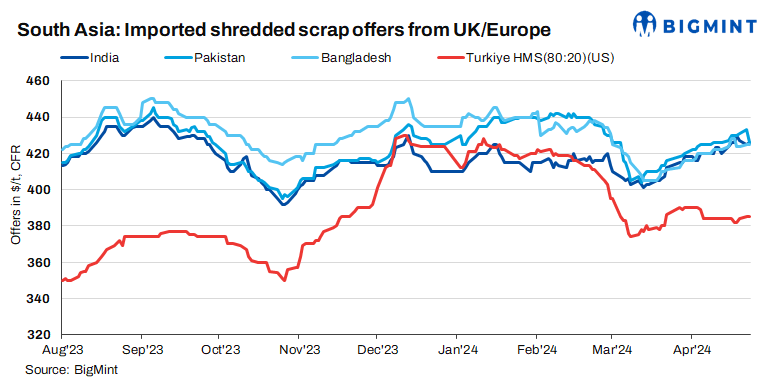

Overview

India: In India, the demand for imported scraps has surged due to a temporary scarcity in the market caused by local suppliers, coupled with the anticipation of increased demand for finished steel ahead of elections. Indicative offers for shredded scrap from the US and Europe are being offered at approximately $425-430/t CFR, while HMS (80:20) offers from West Africa and Europe were assessed at $400-405/t CFR.

According to a source in the trading sector, “Indian buyers in the domestic scrap market are experiencing shortages and are eager to secure both container and bulk scrap quickly. With the Lok Sabha elections underway, there’s an expectation of passive activity for about a month. However, once it concludes, there’s likely to be a surge in demand for project-related requirements and towards the end of the summer construction season.”

A steel mill official commented, “Demand remains strong due to the scarcity of scrap in the market.”

Pakistan: Pakistani buyers have reduced their purchases of imported scrap due to sluggish local steel demand, leading to lower scrap consumption. Offers for shredded scrap from the UK/Europe were heard at $425-427/t CFR Qasim.

In the domestic market, demand for rebars remained slow, resulting in increased inventory levels. Some steel mills reportedly lowered their grade 60 rebar prices unofficially. Present rebar prices were reported at PKR 245,000-255,000/t ex-factory, while local scrap offers ranged between PKR 155,000-160,000/t and billets were at PKR 220,000-225,000/t ex-factory.

A steel mill official stated, “The market for finished products is very slow, with no demand. Shredded scrap is priced at $430/t, and no government projects are currently underway.”

Another mill official commented, “The market is still sluggish, contrary to expectations for improvement post-Ramzan and Eid. Although, we’ve informally reduced rebar prices, it’s not yet official. Weak sales prompted this drop. Most mills are occupied with paying electricity bills this week, with no major activities happening. We anticipate some improvement post-June budget announcement. Production levels remained low at around 40%, with the industry operating at 35-40% capacity.”

Bangladesh: Bangladeshi buyers are procuring imported scrap on an as-needed basis, with some still encountering challenges in opening LCs from banks. Indicative offers for shredded scrap from the UK/Europe were heard at $420-425/t CFR Chattogram, while HMS (80:20) was priced at $400-405/t CFR.

Offers for PNS scraps from Malaysia stood at $445/t CFR, while buyers’ bids hovered around $440/t CFR Chattogram.

Turkiye: Turkish imported scrap prices held steady despite sluggish rebar sales by Turkish mills. The US recyclers actively pursued sales in various export markets, potentially driving prices to $390/t CFR in the near future. Challenges persisted for Turkish mills with limited rebar demand, impacting their purchasing patterns. Despite this, Turkish mill sources anticipate scrap prices to remain relatively stable in the near term, subject to restocking levels. Exported rebar offers stood at $585/t FOB, with similar deals reported to Latin America.

Notably, approximately six bulk scrap cargoes were reportedly booked, including three from the US comprising HMS (80:20), HMS (95:5), and bonus scrap at $382-404/t CFR. The remaining shipments originated from the Netherlands, the UK, and Europe, mainly comprising HMS (80:20) at approximately $380-381/t CFR.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $426/t CFR Nhava Sheva, up by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives were assessed at $426/t CFR Qasim, down by $7/t d-o-d.

Bangladesh: UK-origin shredded prices were assessed stable at $425/t CFR Chattogram, d-o-d.

Turkiye: US-origin HMS (80:20) bulk prices were assessed unchanged at $385/t CFR Turkiye.