A few of the leading primary steel mills have announced their list price levels for hot-rolled coils (HRC) and cold-rolled coils (CRC) for early April 2024. These mills have extended rebate of INR 1,500/t for March towards the month’s end, however, they have raised their list prices by INR 500/t for April sales, BigMint learnt from credible industry sources.

After the announcement, the list price of HRC (IS2062, Gr- E250, 2.5-8mm) stood around INR 53,500-54,000/t ex-Mumbai, while that for CRC (IS513, Gr-O, 0.9mm) around INR 58,800-60,500/t ex-Mumbai for the early-April 2024 sales. These prices are for the coil form, and exclude GST at 18%. However, the list price levels from a few private mills remained elusive.

1. Exports take front seat: The bulk HRC export volumes have been increasing since the low of 47,688 t in December 2023, as per the vessel line-up data maintained with BigMint. The bulk HRC export volumes aggregated to 690,197 t in March 2024 compared with 642,422 t a month back.

Meanwhile, bulk HRC import volumes started softening from February this year. The volumes for bulk HRC imports have dropped to 381,794 t in March 2024 from 465,276 t a month ago.

The closing of the financial year (FY) 2023-24 had propelled mills to seek avenues of offloading their inventories. However, imports dropped because of the reduced gap between the landed prices of imported HRCs and the domestic market price levels over the past three months.

The market participants are still concerned about the need-based buying pattern of domestic buyers, informed a few distributor sources.

2. Manufacturing indices show increase: The Manufacturing Purchasing Managers’ Index (PMI) continued to trek upwards every month in the Q4 FY2023-24 (January-March). Moreover, the PMI for March 2024 was reported at 59.1, which has climbed to a 16-year high, as per data from S&P Global.

Although the growth in the index was driven by improved demand in the manufacturing sector during the last three months, industry sources have pointed out the high-cost burden for end-industrial buyers during the Q4 FY2023-24. Also, only a few manufacturers disseminated the cost burden by increasing the end-product prices over this period, while others averted such actions to retain their customers, as per an S&P Global press release.

Furthermore, most industry participants have highlighted that the increase in direct business-to-customer (B2C) sales by steel manufacturers has been a prominent factor whereas the demand for flat steel products was lacklustre in the traders’ market.

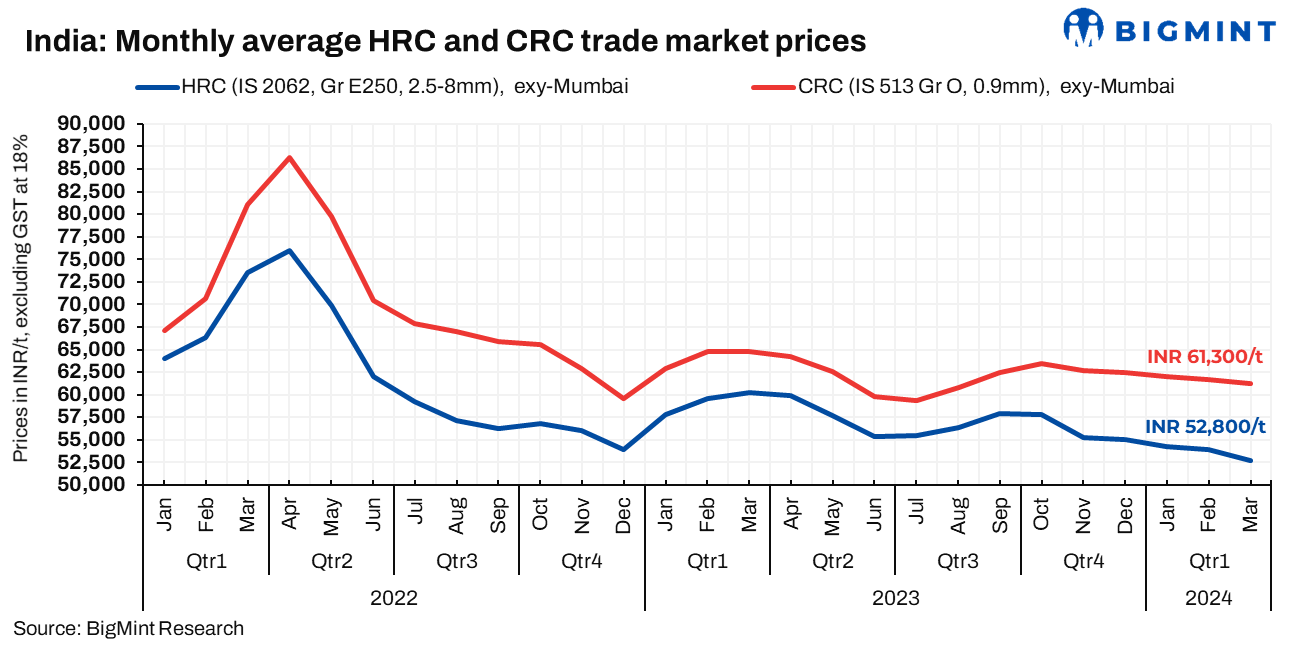

3. Monthly average trade-level HRC, CRC prices fall by up to INR 500/t in March’24: The monthly average prices of trade-level hot-rolled coils (HRC, IS2062, Grade E250, 2.5-8mm) have registered a m-o-m decline, decreasing by approximately INR 1,100/t to reach INR 52,800/t in March 2024, as opposed to the previous month’s figure of INR 53,900/t exy-Mumbai. Simultaneously, cold-rolled coils (CRC, IS513, Gr-O, 0.9mm) have experienced a reduction of INR 400/t on a m-o-m basis, settling at INR 61,300/t in March 2024, compared to the preceding month’s INR 61,700/t exy-Mumbai.

Meanwhile, in the BigMint’s bi-weekly benchmark evaluation on 2 April, 2024- HRC prices fell by INR 200/t to INR 51,800/t exy-Mumbai. Whereas that of CRC remained stable at INR 61,100/t exy-Mumbai. These prices mentioned above exclude GST at 18%, and are for cut-to-length (CTL) form.

Outlook:

The central elections around the corner continued to keep the traders’ market sentiments cautious with distributors and end-industrial buyers cautious about their procurement volumes. The declining traders’ market prices over the past few months is also impacting the market participants’ procurement decisions and making them to stay on sidelines at the beginning of the new fiscal year (FY) 2024-25. Furthermore, the participants are skeptical about the absorption of the list price increase by mills for April and doubt its absorption. Thus, the trade level prices are likely to stay under pressure in the near term which might continue on a slow downward trajectory.