- Production cuts keep rebar prices supported

- HRCs feel poll pressures as infra goes cold

- Will demand, prices see upturn post-elections?

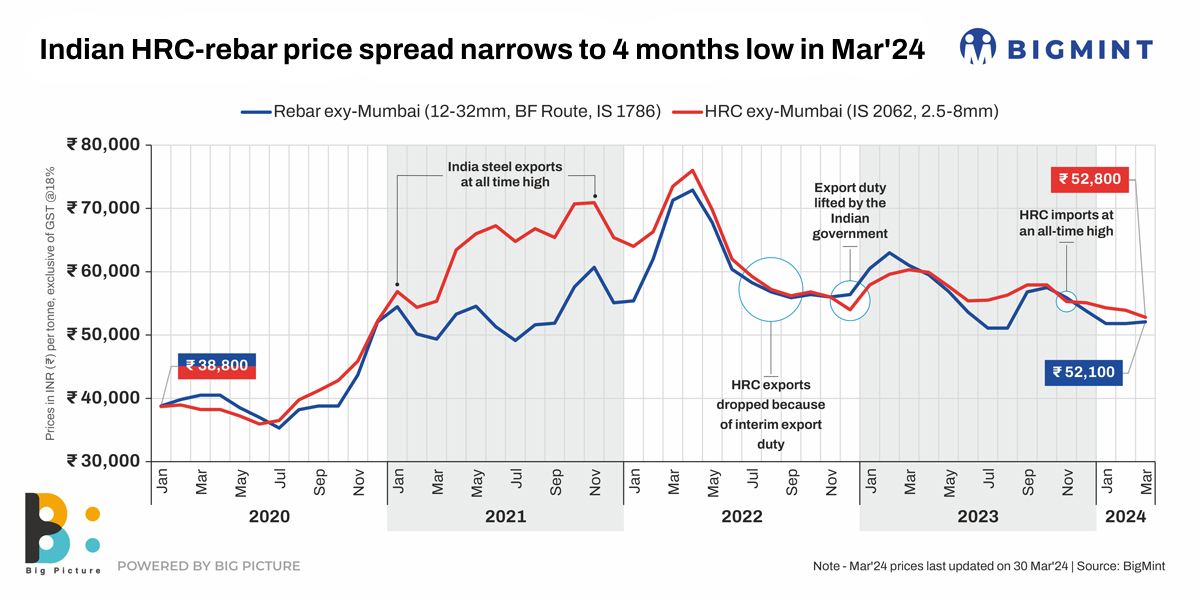

Morning Brief: March, 2024 saw the spread between benchmarked hot rolled coils (HRCs) and blast furnace-route rebar narrowing to a four-month low of INR 700/t ($8/t), reveals data maintained with BigMint. The gap tightened further m-o-m mainly on account of the slight resilience shown by rebars which actually gained by INR 300/t ($4/t) while HRCs eroded by a sharp INR 1,100/t ($13/t).

Trade-level HRCs, ex-Mumbai, fell to INR 52,800/t ($633/t) against INR 53,900/t ($645/t) in February. On the other hand, the benchmark blast furnace (BF)-route rebar, ex-Mumbai, rose m-o-m to INR 52,100/t ($625/t) from INR 51,800/t ($621/t). In rebar, the continuous fall since October 2023 was arrested in March, whereas HRCs have been seeing an unabated fall since the last six months, buffeted by excess supply, and dull home and away demand.

Factors that further narrowed the spread

Rebar

Production cuts support prices: As already mentioned, the spread narrowed mainly because rebars were able to arrest their price fall last month. This happened on the back of the production cuts of 80,000-100,000 t effected by tier-1 mills in February. Longs producers, saddled with an 8% increase in inventory in January, had no choice but to cut production in February to regain the supply demand balance. The formula worked in March. Rebar inventories with tier-1 mills hit a three-month low of around 500,000 t in early-March. The production cuts were forced by the lack of demand in an election year that is characterised by tight liquidity in the market and slowdown in announcements of new projects. The fall in inventory supported rebar prices.

IF rebar prices rise marginally amid sales uptick: The induction furnace mills, which command 65-70% of the market, saw a mixed trend last month. Mills held some amount of orders in hand ahead of the year-end which saw deals happening in patches throughout last month. This allowed the IFs to raise prices slightly from around INR 48,200/t (ex-Mumbai) ($578/t) in February to nearly INR 49,300/t ($591/t) in March. Since IFs command the lion’s share of the market, any price movement also influences tier-1 rebar.

HRCs

Excess capacity in the face of dull demand: Imports of bulk HRCs and plates dropped off to around 213,000 t in March against 465,000 t in February. But domestic supply was up by an additional 60,000 t from NMDC and 160,000 t from JSPL.

Pre-election liquidity crunch: That apart, the year-end blues and pre-election caution caught up with flats. Lack of demand along with liquidity crunch ensured lack of buying. The infrastructure segment, which has been at the forefront of all demand-driving sectors, has gone cold ahead of the polls, hitting HRCs hard.

Export offers fall further m-o-m: The BigMint India HRC export index fell further by $14/t m-o-m in March to $583/t in a dull exports market. The Middle East (ME) was quiet with the onset of Ramadan. Only a single 20,000 t parcel, sealed at $625/t, was seen headed for ME. Vietnam preferred to buy from the Chinese at rock-bottom prices. Only around 14,000 t of cold rolled coils found takers in the European Union.

Outlook

The short term is likely to remain unchanged because of the upcoming elections which will be held over 19 April-1 June, 2024 in seven phases. The market may remain slow in this period, post-which the rainy season will set. However, an upturn in demand and prices is likely post-elections.