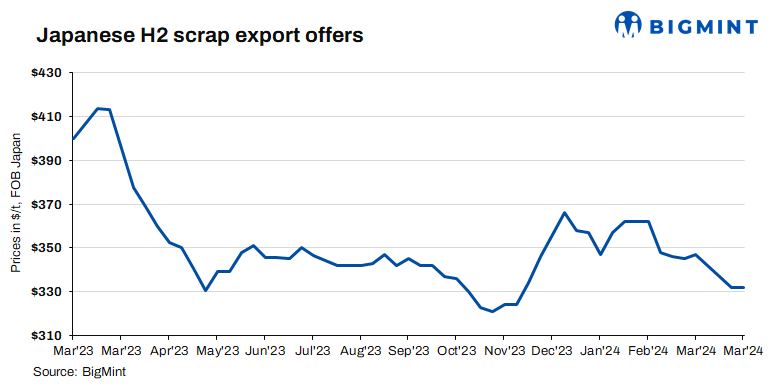

Japanese export offers for H2 scrap remained steady for the second consecutive week, despite subdued interest from major importing nations.

According to BigMint’s latest assessment, Japanese H2 scrap export prices held firm at JPY 50,200/tonne (t) ($332/t) FOB Tokyo Bay.

In the domestic market, Japan’s Iron and Steel Association reported a decline in average prices for H2 across three regions. Prices dropped JPY 300/t w-o-w, with prices in Kanto falling by JPY 400/t to JPY 48,800/t. Prices in Chubu were assessed at JPY 45,900/t (down JPY 600/t), and in Kansai at JPY 47,600/t (down JPY 200/t).

Dockside H2 scrap prices in Japan were observed at JPY 50,000/t FAS Tokyo Bay, reflecting a JPY 200/t increase from the previous week. FAS prices, adjusted to an FOB basis by adding a JPY 1,000/t premium for port charges, indicate indicative offers for H2 at JPY 51,000/t FOB Japan.

Snapshots of other markets

Vietnam: Vietnamese buyers exhibited limited interest in acquiring Japanese scraps due to discrepancies between bids and offers. Offers for H2 scrap from Japan were reported to be in the range of $370-375/t CFR Vietnam, whereas bids from buyers were hovering around $365/t CFR.

As per market participants, Vietnamese mills are actively purchasing local scrap, which offer quicker delivery, and they also have high inventory levels, thus diminishing the necessity to procure large volumes of imported scrap.

South Korea: South Korean mills continued to remain absent from the seaborne market as a result of subdued rebar and scrap sales, alongside reduced factory operating rates contributed to limited procurement activity in the South Korean domestic scrap landscape. Some sources also expressed bearish sentiment in noting the absence of signs of recovery for long products and construction markets in the near term.

Furthermore, Japanese suppliers have ceased providing offers to Korea in light of the market conditions prevailing in South Korea.

Taiwan: During the week, Taiwanese steel makers took a cautious “wait and see” approach, seeking more clarity on pricing dynamics. Additionally, recent reports indicating an impending increase in electricity prices in Taiwan in April 2024 are anticipated to elevate steelmaking costs. Consequently, this tariff adjustment may prompt more industry participants to shift their focus towards billet.

Outlook

In the near future, export offers for Japanese H2 scrap are expected to face continued downward pressure, primarily driven by subdued buying interest from regional markets.