Turkish steelmakers resumed deep-sea scrap market activity last week, aiming for late-April shipments after a brief pause. Approximately five additional deep-sea cargo bookings were expected for April shipments, which were done during the middle of the week, Turkish steel producers continued restocking imported scrap, with reports indicating firm price levels for sales from the US and Europe with around five deep-sea deals heard from the market in a single day.

On 28 March, the market heard a couple of deals from Europe and the Baltic region at $385/t and $384/t respectively, projecting a fluctuating trend in recent days.

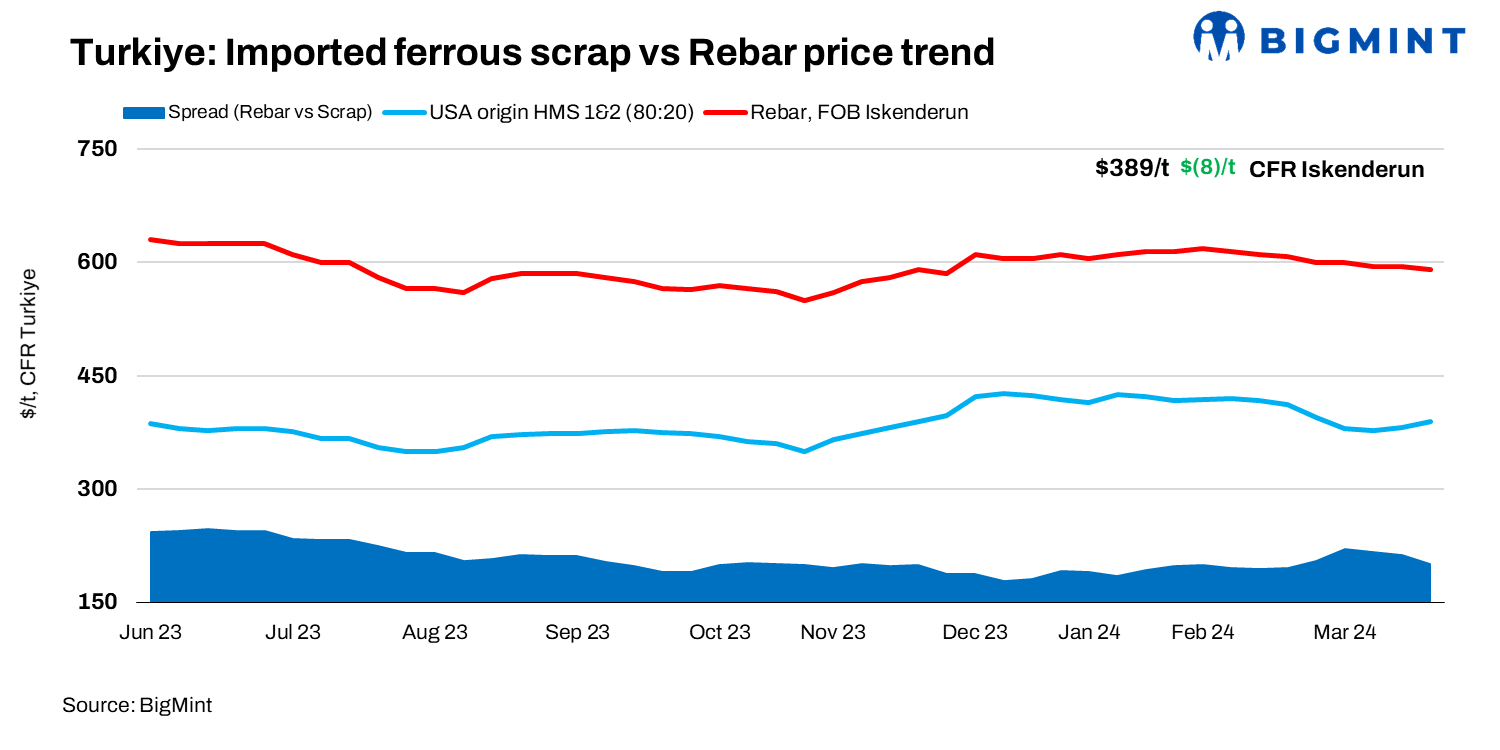

BigMint’s assessment for US-origin HMS (80:20) bulk scrap stood at $389/t CFR, an increase of $8/t w-o-w.

BigMint’s assessment for bulk HMS (80:20) from the US East Coast stood at $365/t FOB, up $9/t w-o-w.

Benelux scrap export prices saw a slight uptick this week in response to a stronger Turkish scrap market, although dockside prices have yet to reflect this increase. While Benelux scrap exporters were not actively participating in international negotiations, suppliers from the US, Baltics, and other EU countries managed to sell their material to Turkiye at higher prices due to improved demand.

As per recyclers, despite some target levels reaching even $400/t CFR for HMS (80:20), no price increase above $390/t CFR was confirmed in recent trades. Turkish mills were resisting higher scrap offers as rebar sales seem to be challenging.

As per a few market sources, it is not expected that there will be much of a price increase; the uptrend is not anticipated to continue to $400/t CFR Turkiye due to the lack of particularly strong steel demand.

Short-sea scenario: The sentiment in the short-sea scrap market was also bullish; however, no new bookings were reported by sources. The target level for shortsea Balkan-origin HMS (80:20) from sellers was $370/t CFR with tradable values at a minimum of $365/t and the indicative workable level at around $365-370/t CFR.

Turkish exported rebar stands at $595/t FOB. The scrap-to-rebar spread was assessed at $205/t FOB, narrowing from $213/t last week.

Recent deals:

- A mill in the Aegean region secured a Netherlands-origin cargo for early-May shipment: 22,000 t of HMS (80:20) at $385.5/t and 8,000 t of bonus scrap at $405.5/t CFR Turkiye.

- East Marmara mill purchased Europe-origin HMS (80:20) at $385/t CFR Turkiye.

- West Marmara mill booked US-origin bulk cargo: HMS (80:20) at $387/t and Bonus scrap at $407/t CFR.

- Aegean mill concluded US-origin deal: HMS (80:20) at $389/t/Shredded & Bonus at $409/t CFR Turkiye.

- East Marmara mill booked Lithuania-origin bulk cargo: HMS (80:20) at $389/t CFR Turkiye.

- A Europe-origin bulk scrap cargo was booked by a Mediterranean region-based mill at $385/t on a CFR Turkiye basis.

- A Baltic region bulk cargo was booked by a Mediterranean region-based mill at $384/t on a CFR Turkiye basis.

- Europe-origin bulk cargo shipment was booked by a West Marmara region-based mill at $382/t for HMS (80:20) and $402/t for shredded/bonus scrap for mid-April shipments.

Domestic market-

Kardemir initiates round of sales: Kardemir, a major Turkish steel producer, raised semis prices by $10/t in its latest sales round, reflecting developments in the scrap segment. While some find this move justified, others question its feasibility for customers. Local suppliers also reported sales activity, with Kardemir’s new prices for Semis S235JR and B420 at $555/t EXW and $565/t EXW respectively. Business results remain uncertain, with varying reports on sales volumes. Other Turkish suppliers adjusted billet prices to $570-575/t EXW, citing rising scrap prices. Import deals are anticipated.

Isdemir’s renewable rnergy pursuit: Isdemir, a subsidiary of OYAK Mining Metallurgy Group, is actively pursuing energy sufficiency through renewable sources, particularly solar power. Applications for solar power plants in three provinces represent a total investment of TRY 4.5 billion ($139.8 million). The move aligns with the industry’s green transformation, aiming to reduce carbon emissions and lower energy costs. Construction is estimated to take 25 months, with potential equipment installation by late 2024. OYAK aims for net zero emissions by 2053.

Colakoglu Metalurji’s carbon reduction targets: Colakoglu Metalurji announced ambitious carbon reduction targets aligned with Turkiye’s net zero emission goals by 2053. Plans include increasing green energy capabilities, process improvements, and digitalization. With a diverse product portfolio and a commitment to sustainability and innovation, the company aims to cut carbon emissions by 55% by 2030 and achieve zero emissions by 2050.

Challenges in construction sector: Turkiye’s construction sector faces structural economic challenges, with a recent decline in the confidence index. March saw a 3.6% month-on-month drop, with subsequent declines in key indexes such as overall order books and employment expectations. Financial constraints affect 30% of companies, while a 16.6% rise in demand scarcity further impedes sector growth, impacting the steel industry as well.

Outlook: Despite subdued demand for finished long products, Turkish steelmakers are poised to pursue rebar and billet price hikes in the coming days. Anticipated increases in scrap supplier offers coincide with declining scrap collection rates. Steelmakers are expected to maintain activity, focusing on early May shipment bookings following the completion of April shipments.