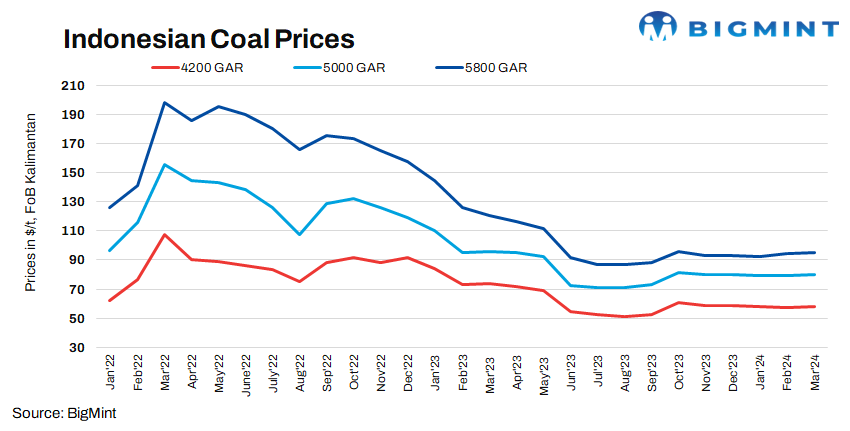

During the previous week, Indonesian thermal coal prices dropped. Prices of low-CV (3400 GAR) coal decreased by $1.04/tonnes (t), reaching $35.86/t, while high-CV (5800 GAR) coal fell by $1.33/t, settling at $95.08/t.

On the supply side in Indonesia, the regions of Sumatra and South Kalimantan have been experiencing unpredictable rain. Consequently, many spot vessels have become stranded at the ports, awaiting loading, which has kept the supply tight. The prolonged rainy season is preventing improvements in the hauling process at the mines, leading to a slowdown in operations. Additionally, as most of the mine workers are observing Ramadan, mines are operating intermittently, affecting output and causing delays in deliveries.

Demand in the Asian thermal coal market continued to be sluggish. Despite the reduced availability of March to first-half April 2024-loading cargoes, offer levels continued to decline due to limited buying interest from its largest buyers, India and China. China’s domestic prices are still on a downward trend, indicating extremely low coal consumption in the country at present. In addition to the Chinese power sector, demand from the steel and cement sectors of the country were also weak. Chinese domestic coal prices dropped due to ample stocks and a lack of economic stimulus, exerting downward pressure on Indonesian coal prices. Consequently, Chinese end-users are requesting deep discounts from Indonesian coal traders.

The current demand from India was subdued amid plenty of existing stocks and sound domestic production. Demand from India largely remained low, with only a few power plants occasionally purchasing Indonesian mid-CV coal. Seaborne coal demand is also weak, as most buyers have adopted a wait-and-watch approach amid market volatility. There are pockets of demand coming from some power plants stocking up for the summer.

India: Portside prices drop by INR 150/t

The thermal coal prices of 4200 GAR coal at Kandla Port have dropped to INR 6,450/tonnes. This decline in prices can be attributed to subdued demand.

Outlook

Prices in Indonesia may increase in the coming weeks due to the anticipated surge in demand for Indonesian coal from India, expected towards the end of March 2024, primarily from power plants coinciding with the full onset of summer. Additionally, demand from the cement sector may increase post-election due to an increase in new infrastructure projects. However, the domestic coal market in China continued to drop, affecting demand for the Indonesian thermal coal market and prices. Nonetheless, there could be supply constraints from Indonesia due to rainfall in Sumatra and other regions of the country. These supply constraints are resulting in less availability of cargo in the spot market.