- Iron ore imports, steel exports ride higher crude steel output

- Coal production falls amid production curb diktats

- March steel output may fall amid rising stocks, lower prices

Morning Brief: Performance of China’s key economic indicators improved over January-February, 2024, reveals National Bureau of Statistics data maintained with BigMint. Crude steel surprised markets, while iron ore benefitted from it. Exports sustained their uptrend amid the still struggling realty sector.

It may be noted that China releases combined data for January and February every year to iron out any inconsistencies that may arise from the lull seen during the week-long Lunar New Year holidays, which fall at different times in the first two months of the year.

Crude steel production rises

China, despite maintaining a flat crude steel production trend for the full year of 2023 at 1,019 million tonnes (mnt), has seen a slight uptrend yet again. NBS data maintained with BigMint shows that crude steel production rose 1.60% over January-February, 2024 to almost 168 mnt. This slight increase surprised markets as the expectation was the volume would fall especially against the backdrop of a still struggling real estate sector and falling domestic demand.

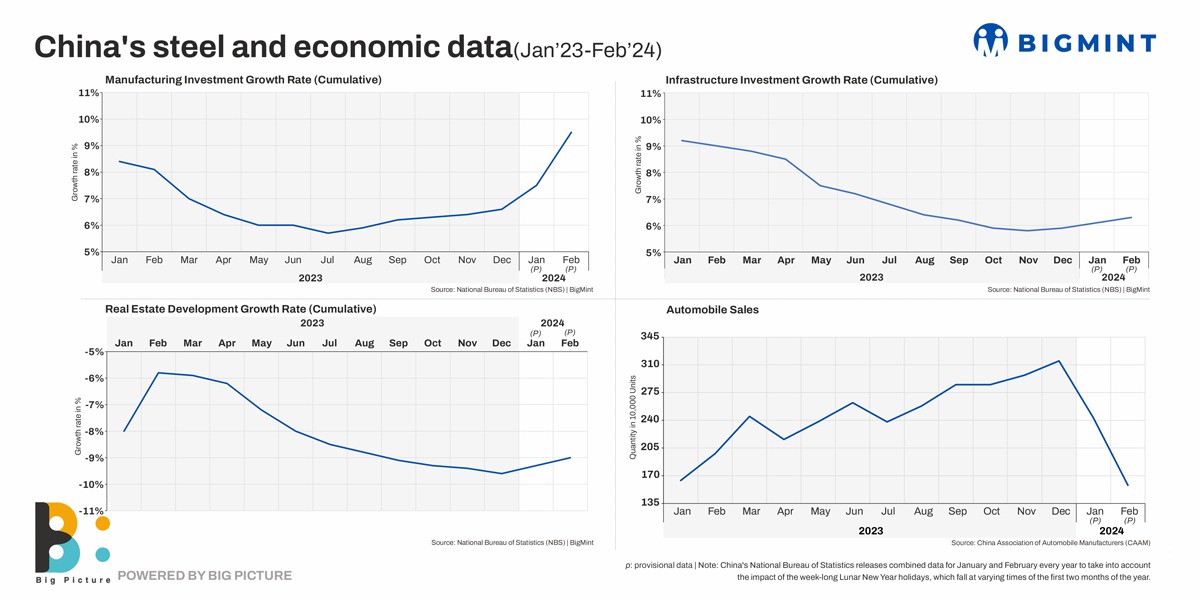

The rise in output can be a function of a few factors. First is the sharp increase in steel exports over January-February, 2024. Secondly, the better performance of some of the downstream sectors. Manufacturing investment saw a significant 9.5% increase in February from 6.6% in December 2023, thanks to the government’s stimulus measures. Infrastructure investment also showed a 6.3% growth from 5.9% in December 2023.

But, real estate development growth dropped 9% in the first two months compared to an already 9.6% decline in December, 2023. Realty pulled down cement production by 1.60% y-o-y to 183 mnt over January-February, 2024. In 2023, volumes fell nearly 1% to 2,023 mnt.

Automotive sales, even if they showed m-o-m drop in January and February, combined figures for the two months show a growth to 4 million units (MU) against 3.15 MU in December.

Pig iron production dipped a slight -0.60% in the period under review to 141 mnt while in 2023 the volume upped a marginal 1% to 871 mnt.

Iron ore imports ride higher output, lower prices

Iron ore imports rode the increased crude steel production, rising 8% to 209 mnt in the first two months of 2024 while 2023 volumes were up 7% to 1,179 mnt. Buyers also capitalized on the lower prices. From $136/t CFR China in December 2023, prices fell to $126/t in February.

Steel exports rise to 8-year high?

Steel exports rose 33% to almost 16 mnt in the two months under review, the highest for the period since 2016, as per some sources. Subdued domestic market sentiments and competitive offers helped China gain an edge over other suppliers globally and capture large chunks of the export market and offset some losses.

China’s steel exports for the entire calendar of 2023 closed at 91 mnt, up 35% over 2022.

Steel imports drop amid weak yuan, global offers

Steel imports dropped 8% in the first two months to 1.13 mnt while for 2023 these showed a steeper 28% decline to 8 mnt.

Weak domestic demand and a falling yuan colluded to keep imports down. The yuan fell 9% against the dollar last year. Plus, weak global offers, in which China itself had a hand, also discouraged exporting countries. These included Southeast Asia, Japan and Korea who preferred to explore alternative markets to reduce dependency on China or focus on domestic demand.

Coal production dips, imports rise

Coal production dipped 4% to 710 mnt in the first two months under review although for the whole year of 2023 volumes rose 4% to 4,660 mnt.

The drop in production so far this year is an offshoot of the output curbs ordered in Shanxi, China’s largest coal-producing province, last month. The move comes close on the heels of a rise in coal mine fatalities in the northern region by around 50% last year. Despite the curbs, a couple of accidents still occurred during the key National People’s Congress held over 5-11 March, 2024. Thus, analysts believe, the output curbs could spread to other coal-producing provinces as well.

Coal imports, meanwhile, showed a 23% increase to 75 mnt in January-February, 2024. On a full year basis, imports spurted 62% to 474 mnt. Imports rose mainly on account of two reasons. One was to take care of the drop in domestic coal production. Two, Chinese buyers took advantage of the sliding prices of both coking and thermal coals.

Outlook

Crude steel output may drop in March because the supply glut amid weak domestic demand led to inventory pile-up and falling prices. Moreover, the dull period following the Lunar holidays impelled some mills to curb production. Iron ore imports will be governed by output.

Since demand recovery is expected to remain slow, exports may sustain their uptrend in the current month.

Coal production may stabilize amid the output curb.