Indian demand subdued amid sufficient stocks

PT Bukit Asam resumes coal railing activities after flyover collapse

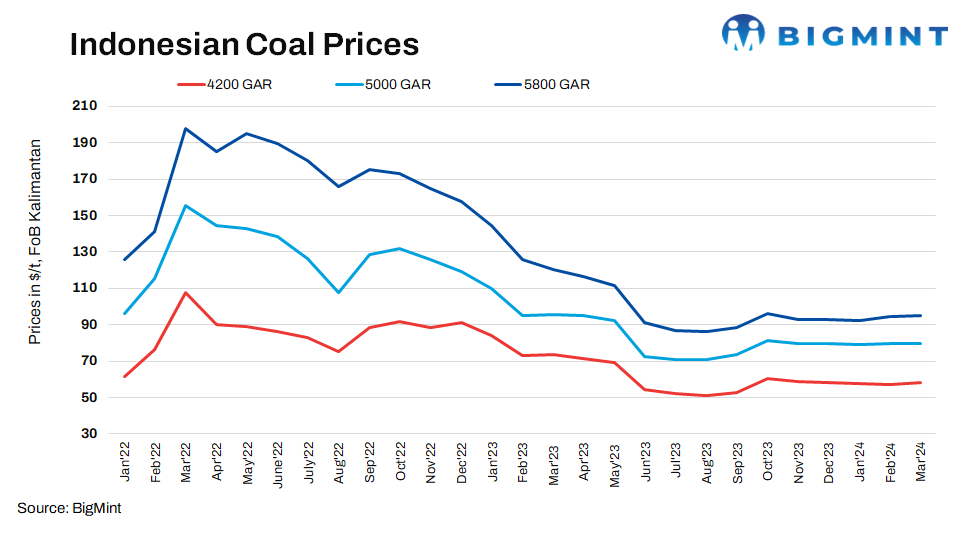

During the previous week, Indonesian thermal coal prices displayed varied trends. Prices for low-CV (3400 GAR) coal decreased by $0.47/tonnes (t), reaching $63.90/t, while high-CV (5800 GAR) coal observed a minor increase of $0.24/t, settling at $96.41/t.

On the supply side in Indonesia, the fundamentals remained unchanged, with some mines in the Sumatra region are still experiencing disruptions in hauling and transportation, thereby restricting the availability of spot cargoes from the region.

PT Bukit Asam resumed coal transport via rail activities after a flyover collapse disrupted its rail operations in South Sumatra. Mines in South Sumatra were not impacted by the train derailment, as they were able to utilise an alternative route, thus minimising the impact on supply in the market.

Demand in the Asian thermal coal market remained subdued as Chinese domestic coal prices dropped due to ample stocks and a lack of economic stimulus, exerting downward pressure on Indonesian coal prices. Due to the decrease in Chinese domestic coal prices, Chinese end-users are requesting deep discounts from Indonesian coal traders. Chinese buyers had booked cargoes well in advance, factoring in weather-related supply challenges in Indonesia. With ample existing stocks at Chinese power plants and a consistent drop in domestic prices, they are currently not actively participating in the market.

Demand fundamentals in India also remained unchanged. Demand from India largely remained subdued, with few power plants occasionally purchasing Indonesian mid-CV coal. Seaborne coal demand is also weak, as most buyers have adopted a wait-and-watch approach amid market volatility. Indonesian coal demand is expected to increase from the end of March, driven by improved demand from power plants due to summers, particularly for high-CV coal.

India: Portside prices increase by INR 150/t

Thermal coal prices for 4200 GAR coal at Kandla Port increased to INR 6,450/tonnes. This uptick in prices can be attributed to increases in freight rates and supply constraints in Indonesia.

Outlook

Prices in Indonesia may increase in the coming weeks due to the anticipated surge in demand for Indonesian coal from India, expected towards the end of March, primarily from power plants coinciding with the full onset of summer. Additionally, demand from the cement sector may increase post-election due to an increase in new infrastructure projects. However, there could be some supply constraints from Indonesia due to rainfall in Sumatra and other regions of the country. These supply constraints are causing less availability of cargo in the spot market.