- Spread narrows by INR 400/t to INR 2,100/t in Feb

- Rebar remains stable m-o-m on production cuts and higher cost of production

- Imports, dull exports, global prices keep HRC muted

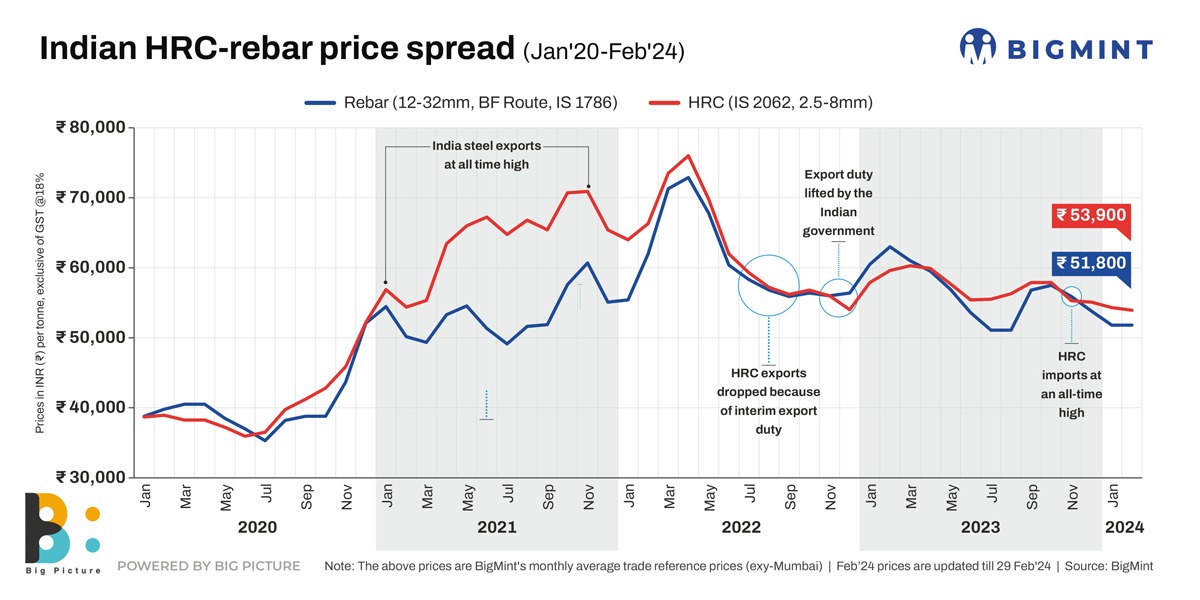

Morning Brief: The spread between benchmarked hot rolled coils (HRCs) and blast furnace-route rebar narrowed by INR 400/tonne (t) ($5/t) m-o-m to INR 2,100/t tonne (t) ($25/t), in February 2024, as per data maintained with BigMint. The gap tightened a bit mainly on account of the slight resilience shown by rebar compared to HRCs, even as the latter moved in a narrow range.

Trade-level HRCs, ex-Mumbai, fell by around 1% in February to INR 53,900/t ($650/t) from INR 54,300/t ($655/t) in the preceding month. On the other hand, the benchmark blast furnace (BF)-route rebar, ex-Mumbai, remained static at INR 51,800/t ($625/t).

However, it may be noted both HRC and rebar prices have fallen steadily since October last year.

Factors that narrowed the spread

Production cuts by tier-1 mills: Saddled with rising inventory, tier-1 mills effected production cuts in February, of 80,000-100,000 t.

The production cuts were impelled by a few reasons. One was to restore the supply-demand imbalance plaguing the market for many months now. Two, project prices of blast furnace-route rebar fell below the psychological 50k-mark to hover at INR 49,500-50,000/t ($597-603/t) FOR, while retail prices, ex-Mumbai, remained more or less stable at INR 51,000-51,500/t ($615-621/t). Three, prices fell because of the tepid demand scenario prevailing for many months now. Projects have lessened off-take ahead of the elections this year.

Rebar inventories fall: Rebar inventories, which had climbed up by around 8% m-o-m in January, showed signs of easing in February thanks to the production cuts. Inventories with tier-1 mills dropped by around 10% last month to around 550,000 tonnes (t) against the well over 600,000 t seen in the previous month. While State-based mills did still nurse huge stockpiles, the private ones were able to liquidate to some extent.

IF mills see drop in inventory: The induction furnace mills, which command 65-70% share of the rebar market, and influence price dynamics of tier-1 mills, too witnessed a drop in inventory in February compared to the 25-30% increase seen in January. Thus, their stocks idling period dropped off to 7-day levels against the usual 10-15. But the stocks fell essentially because they too undertook some amount of production cuts across regions except in western India, where the units operated at 100% capacity. Secondly, trade improved, which also encouraged lower rebates.

Imports still land on Indian shores: On the flip-side, HRCs were not so lucky, even if these did not fall sharply but by a minor 1%. One key factor was imports. Bulk HRC and plates imports did decline from 660,000 tonnes-plus in January to over 400,000 tonnes in February. This was mainly because no fresh cargoes were booked from late last year. Mills are hoping volumes will taper off in the short to medium term especially since the BIS licences of exporters are yet to be renewed by the Indian government.

Dull exports fail to pull up domestic HRCs: Indian steel exports, in which HRCs command the highest share, continued to remain dull as EU buyers turned slow after exhaustion of quotas for Q1 and lack of clarity on Q2 portions. Secondly, EU buyers avoided imports on expectations of further price falls in their domestic market. India’s HRC export index nudged down to $597/t FOB in February against $601/t in January while offers to the Middle East dipped 1% and to Vietnam 2% m-o-m. Weak exports failed to pull up domestic prices.

Global prices fall: Prices of steel and raw materials in global markets fell amid the Chinese Lunar New Year, Vietnam’s Tet holidays and the overall dull demand trend in Europe and other geographies. Chinese and Japanese HRC offers dropped by $11/t and $10/t respectively to $563/t and $600/t FOB respectively, influencing Indian HRC prices too. Globally, raw material prices stayed depressed on lack of buying from China.

Domestic raw materials fall: Domestic raw material prices fell slightly or remained flat m-o-m in February. From iron ore and coals, to sponge iron, scrap and billets, prices showed a highly dull trend, as a result of which finished products like rebar and HRCs also failed to find support last month. Thus, even if rebars did not fall, they remained static while HRCs showed a slight dip.

Outlook

Rebar prices may remain supported, thanks to the recent production cuts. Raw material prices will be keenly watched too. HRCs may continue to remain under pressure as domestic and global market fundamentals are unlikely to change in the short term.