- Iron ore, pellet exports rise sharply in CY’23

- Supplies tight on higher fines exports, increased pellet output

- Weak sponge iron margins hold back lumps prices from rising

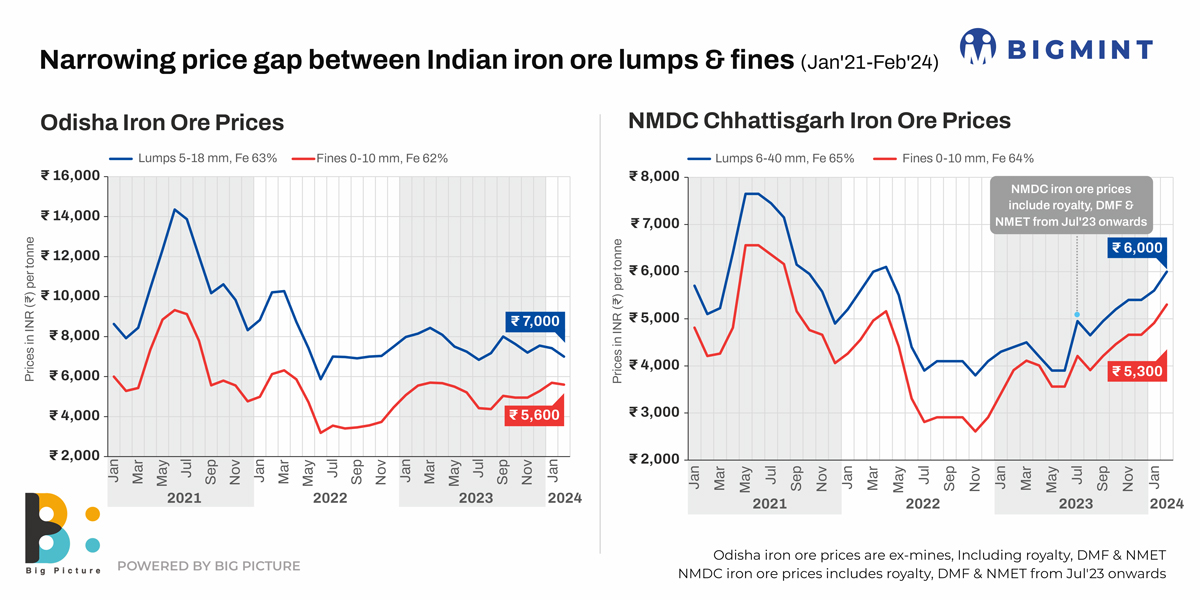

Morning Brief: The price gap or differential between iron ore lumps and fines in the domestic market seems to have narrowed significantly over the last two years, BigMint assessment reveals. This is to be understood as directly co-related with higher exports of iron ore fines and pellets during the period.

Data show that in Odisha, a state accounting for over 50% of the country’s annual iron ore output, the gap has narrowed since 2021. For instance, the differential between Fe63% lump ore (5-18mm) and Fe62% fines prices in Odisha, as assessed by BigMint, has reduced from INR 3,000/t in March’21 to INR 1,500/t currently.

In fact, the gap between Fe63% fines and lumps of the same grade in Odisha stands at around INR 1,000/t currently. Our assessment shows that NMDC iron ore prices, too, reveal the same trend.

Except during the phase of exceptionally inflated domestic iron ore prices in mid-2021, in tandem with the global surge in iron ore prices following post-COVID economic recovery, the trend of decreasing price gap between lumps and fines is quite evident.

Why gap is narrowing?

- Higher iron ore exports: Exports of iron ore, mainly fines of below Fe58% grade, as well as pellets rose to a three-year high of over 44 mnt in CY’23. Below Fe58% grade fines made up about 75% of total exports. Pellet exports increased by 43% y-o-y to over 10 mnt, which supported fines consumption and prices.

- Higher pellet output, fines demand: Production of iron ore pellets in CY’23 stood at around 91 mnt, higher by 10% compared with total output in CY’22. India’s pellet capacity has increased significantly to over 140 mnt and stronger production and capacity expansion has kept iron ore fines consumption well supported. So, naturally, fines prices were driven by surging pellet production.

- Sponge iron margins thin: Prices of iron ore lumps did not increase in tandem with fines as margins of sponge iron producers remained under pressure. Declining prices of sponge iron amid higher production have kept margins squeezed despite easing imported coal prices.

Outlook

Amid shrinking margins of producers, the price difference between iron ore lumps- and pellet-based sponge iron has also narrowed considerably. As per BigMint data, the differential between domestic CDRI and PDRI prices has narrowed to just INR 1,000-1,500/t currently from around INR 2,100/t some three months back.

It may be expected that fines consumption and prices will stay supported, thanks to significant expansion in blast furnace steelmaking capacity in the pipeline, as well as increasing pellet production capacity. However, lumps demand may not receive such support due to significant pressure on margins of DRI producers.

Moreover, the Indian steel industry may have a challenging FY’25 due to the general election and its impact on economic and industry activity, as well as near-term impact on steel-using sectors.