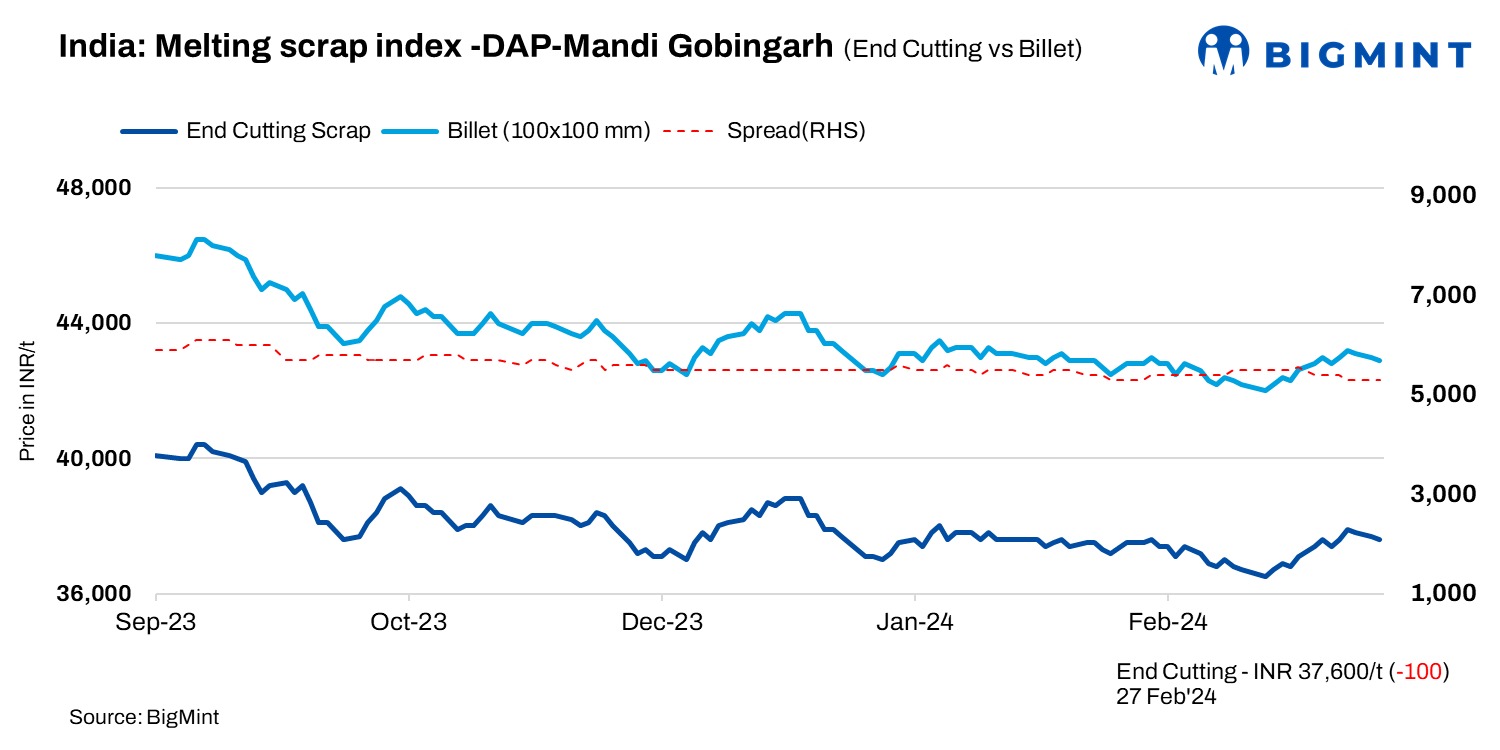

According to BigMint’s report dated 27 February 2024, the Mandi Gobindgarh steel market experienced a decrease in prices for domestic end-cutting scrap. Prices declined by INR 100 per/t, reaching INR 37,600/t delivered at the plant.

Steel market

In Mandi, there is a notable lack of interest among buyers in imported scrap, primarily due to price disparities. Consequently, mill owners are directing their attention towards domestic steel scrap, which is being sourced from neighbouring states. In terms of the charge mix for steel making, mills are incorporating a ratio of 80% scrap and 20% sponge iron, either based on standard proportions or adjusted according to specific grade requirements.

Today, prices of steel ingots dropped by INR 150/t to INR 42,900/t during reporting and price normalisation. Similarly, prices in several significant markets witnessed a decrease, ranging from INR 100/t to INR 300/t.

Rebar (Fe500) prices witnessed a decrease of INR 200/t, settling at INR 47,500/t ex-works amid sluggish trading conditions today.

Steel prices have been on a downward trend for the past few days amidst limited activity, yet the overall market outlook suggests a range-bound movement on a weekly basis, a mill owner told BigMint.

Raw material price update

In Mandi, the price of sponge iron (CDRI) declined by INR 100/t to INR 31,000/t today, while pig iron (steel grade) prices in Ludhiana remained stable at INR 39,300/t on a delivered-at-plant (DAP) basis.

Overview of other markets

BigMint’s assessment reveals a decline of INR 200/t in ship-breaking melting scrap prices in Gujarat’s Alang market on 27 February, 2024. HMS (80:20) rates stood at INR 33,500/t ex-yard. Limited demand for semi-finished and finished steel in the market yesterday, combined with subdued buying inquiries for scrap, have resulted in suppliers reducing their offers today.

Today, the Raipur steel market experienced sluggish trade activity, with prices for semi-finished and finished steel witnessing a decline due to limited buyer interest. While mills have sufficient inventory of finished steel, there is selling pressure in the market. Billet prices fell by INR 150/t to INR 39,250/t, while rebar(Fe500) prices down by INR 42,800/t d-o-d.

Imported scrap market

The pace of India’s imported ferrous scrap market remains sluggish, with buyers showing a preference for materials that have already been booked and are scheduled to arrive at Indian ports in March and April at lower prices compared to current offers for fresh shipments. This subdued buying trend is influenced by the slow domestic steel market and a growing interest in non-European cargoes due to significant price gaps with European-origin shipments.

Indicative offers for shredded scrap from Europe hovered around $430-$435/t CFR Nhava Sheva, while practical prices for imminent shipments were reported at $415-$420/t CFR.

A steel mill official commented, “We’re only securing shipments slated for March and April arrivals, given subdued sales of finished steel. Consequently, we’ve reduced our production and are incorporating sponge iron into our charge mix.”

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $382-$394/t, which equates to approximately INR 34,855/t (including freight), while local scrap-HMS (80:20) prices in Mumbai increased by INR 100/t to INR 33,600/t d-o-d.

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,150/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – info@steelmint.com.