Today, South Asian ferrous scrap prices displayed a mixed trend. Indian buyers refrained from active participation due to unviable import offers and abundant stocks available before year-end closures. In Pakistan and Bangladesh, markets encountered challenges related to letters of credit (LC), along with a slowdown in the domestic finished steel market.

Shredded scrap offers increased marginally by $1/t in India and Bangladesh but decreased by $2/t in Pakistan. Meanwhile, US bulk HMS (80:20) offers to Turkiye remained unchanged for the day.

Overview

In the current Indian market scenario, purchasing activity remains sluggish, particularly with regard to European transactions which have been muted lately. Shredded scrap offers from European sellers at approximately $415-420/t CFR Nhava Sheva are still deemed unfeasible for buyers. Additionally, downstream purchasers are not exhibiting urgent demand for scrap materials, as they possess an ample inventory of raw materials and finished steel. Additionally, steel sales are reportedly low in certain regions.

According to a representative from a steel mill,”We currently have a one-month inventory on hand, and given the approaching year-end, we’ve adjusted our purchasing pace accordingly.”

Another steel mill representative noted, “Sales of finished steel are sluggish in the northern region. Market conditions are challenging due to recent farmer protests and ensuing roadblocks. Moreover, with upcoming elections and associated regulatory constraints, market pressures are expected to intensify, potentially leading to a liquidity crunch.”

Market activities in Pakistan and Bangladesh remained subdued today, as buyers encountered difficulties in opening letters of credit from banks.

A steel mill based in Pakistan shared their perspective, noting that “demand for finished steel also remains sluggish. Although steel mills have gradually resumed bookings, delays in letters of credit continue to pose a challenge for import-dependent mills.”

Additionally, Turkish imported ferrous scrap remained stable at $411/t CFR following the recent European deal. Buy-side sources anticipate further price drops due to oversupply and sluggish rebar sales. Turkish mills bid low, with EU-origin HMS (80:20) at $400/t CFR and US-origin at $405/t CFR. European recyclers wait for price recovery or improved demand, while some withdraw due to unworkable Turkish mill targets. HMS collection costs in the Benelux region were Euro 340-345/t delivered to docks.

Price assessment

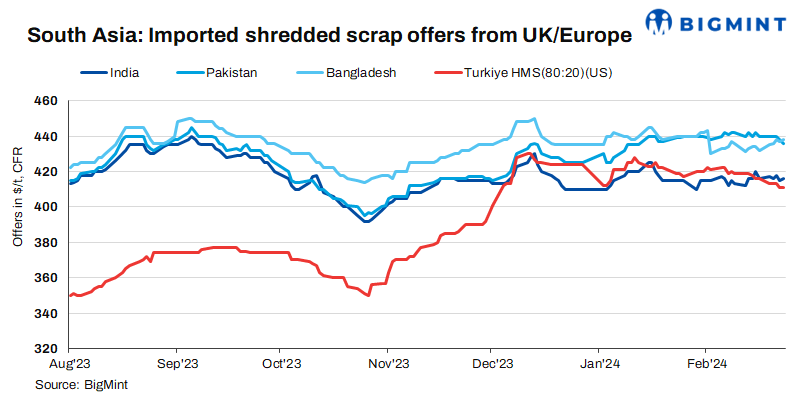

India: UK-origin shredded scrap indicatives were assessed at $416/t CFR Nhava Sheva, up by $1/t d-o-d.

Pakistan: UK-origin shredded scrap indicatives were inched down by $2/t to $436/t CFR Qasim.

Bangladesh: UK-origin shredded scrap prices were assessed at $438/t CFR Chattogram, up by $1/t.

Turkiye: US-origin HMS (80:20) bulk prices were assessed at $411/t CFR Turkiye, unchanged d-o-d.

Outlook

In the near term, imported scrap offers are expected to undergo slight corrections. In India, numerous distress cargo sales are occurring, prompting buyers to wait for offers to reach their desired levels before making fresh bookings. Similarly, markets in Pakistan and Bangladesh have slowed down purchases, anticipating a decrease in offers. Turkish mills also anticipate a drop due to an oversupply of scrap and subdued sales in the domestic market.