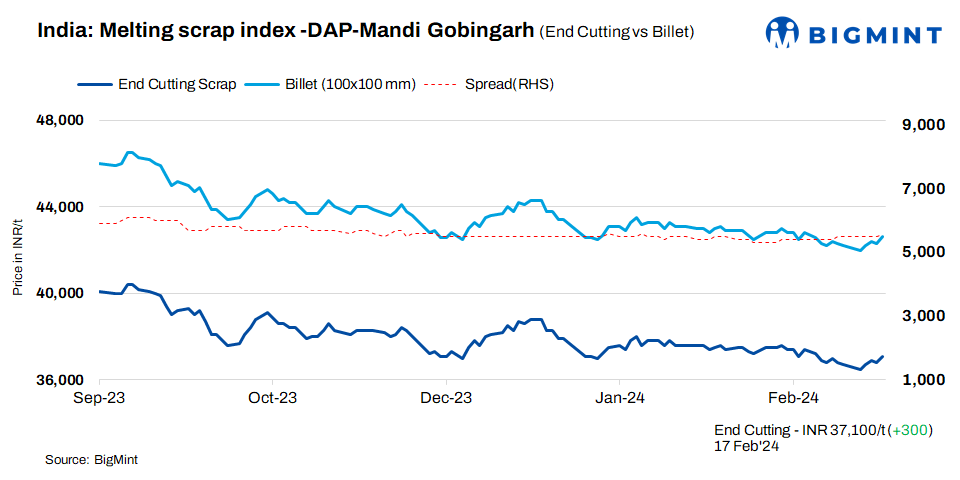

The domestic steel scrap index (end-cutting) in Mandi Gobindgarh, as reported by BigMint on 17 February 2024, recorded a rise of INR 300/t, settling at INR 37,100/t on a delivered-at-plant (DAP) basis. The Mandi steel market witnessed improved demand in the previous trading day, and today’s market displayed moderate activity, accompanied by increasing prices. Weekly figures showed a positive trend, with scrap prices improved by INR 400/t.

Steel market

Steel ingot prices in Mandi witnessed a INR 250/t increase to INR 42,650/t during reporting and price normalisation. Concurrently, prices in other key markets rose by INR 50/t to INR 450/t. The Mandi Gobindgarh semi-finished and finished steel markets showed decent trade today, leading to a INR 200/t uptick in rebar prices, which reached INR 46,900/t ex-works.

Overview of other markets

Alang: Ship-breaking melting scrap prices inched up by INR 100/t d-o-d in Gujarat’s Alang market on 17 February, 2024. BigMint assessed opening prices of HMS (80:20) at INR 34,000/t ex-yard. Semi-finished and finished steel prices improved in the late hours of yesterday’s trading session and moderate buying interest for scrap prompted suppliers to hike offers today.

Imported scrap market weekly trend

This week, market activities in India remained lacklustre as buyers leaned towards domestic scrap procurement and other available alternatives due to a significant gap between landed imports and domestic scrap prices. On a weekly average basis, imported offers for shredded scrap from Europe edged up slightly by $1/t to $416/t CFR Nhava Sheva from $415/t CFR in the previous week, while HMS (80:20) offers dropped by $9/t on the week to $389/t CFR.

A representative from a trading company remarked, “The current market suggests that shredded scrap should not exceed $400/t. However, indicative prices from the EU/UK are higher at $430-435/t, creating a $30/t gap that makes it economically unviable.”

Another trader commented, “Imports have become economically impractical in India, leading buyers to favour local sources or alternatives like sponge. The few transactions happening involve arrival cargoes, with the maximum price for HMS capped at $385/t. Fresh bookings in the market are currently scarce due to these prevailing circumstances.”

Throughout the week, approximately 1,000 t of shredded scraps were sold at $419/t CFR, followed by 500 t of HMS (80:20) at around $365-370/t CFR and around 250 t of turning boring scraps at $345/t CFR.

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic vs imported scrap market: Imported melting scrap prices at Nhava Sheva Port were at around $385-$388 (average $387/t), which equates to approximately INR 34,300/t(including freight),while local scrap-HMS (80:20) prices in Mumbai remained stable at INR 32,500/t d-o-d.

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 12,850/t.

To see SteelMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – info@steelmint.com.