The Vietnamese imported ferrous scrap market witnessed a downtrend in terms of prices, with a limited recovery in demand before the lunar holidays. according to a source from a Vietnamese mill.

As per a trading source, “The market is very quiet here as the holiday is coming. We are receiving the same offer prices but have not concluded, seems like the situation is getting worse due to the Chinese closure.”

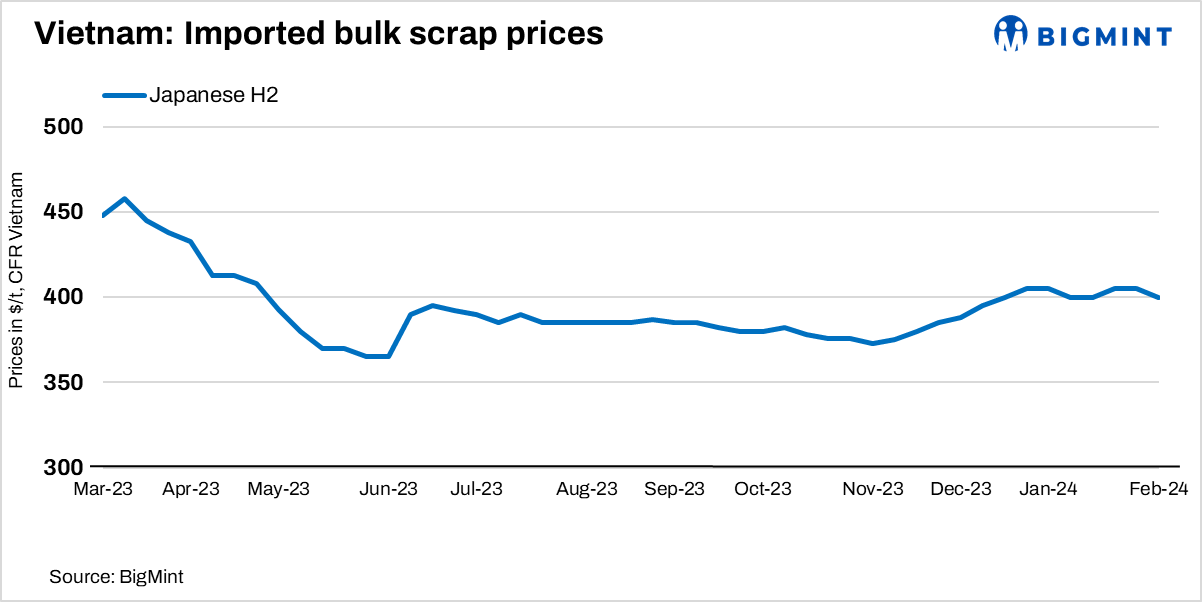

A Vietnamese mill source mentioned low demand after the previous week’s uptick, with anticipation building for the Lunar New Year.

US-origin HMS (80:20) bulk scrap hovered at around $405-410/t with no major inquiries heard from market participants for the week. On the other hand, H2 offers as of last weekend hovered around $400/t CFR Vietnam, as per a market source.

Vietnamese HS buyers held firm at $415/t CFR Vietnam, while traders stood at $420/t CFR, signaling a deadlock before the Lunar New Year holidays. Traders, not in a hurry to sell, reported steady offer levels but a lack of buyer interest. In South Korea, mills remained disinterested in the seaborne market, citing ample local scrap and higher overseas scrap prices compared to local rates.

A Japanese trader noted subdued demand from Vietnam, attributing it to Tokyo Steel’s recent price cut and a decline in supply-side prices.

Domestic market: Domestic Type 1 (thickness 3-6mm) bid prices on the last closing were observed at VND 9,900-10,300/kg delivered to a northern region mill, excluding VAT, as reported by a mill source. Similarly, in the southern region, bid prices for the same type were noted at VND 9,350-9,950/kg on the same period.

Hoa Phat has dropped monthly HRC (SAE1006, non-skinpass) prices for April-May’24 sales by $30/t m-o-m. Post-revision, effective prices are at VND 14,852/kg or $610/t CIF HCMC (southern region) against the previous price of VND 15,653/kg ($640/t) excluding VAT. The price drop came amid slow domestic demand along with competitive import offers from China with slow Chinese SHFE HRC futures

In the best-case scenario, Vietnam’s GDP could grow by 6.48% this year, according to the Central Institute for Economic Management. To navigate uncertainties, experts recommend the government capitalise on the country’s strengths, prioritise infrastructure projects, and invest in initiatives supporting short- and long-term growth. HSBC emphasises the need to enhance infrastructure, the workforce, and the business environment to attract investors. Board IV suggests implementing more support policies for businesses in 2024 while acknowledging that recovery requires time, resources, and support.

Exchange rate: The State Bank of Vietnam (SBV) lowered its reference rate by 0.02% to VND 23,954, while the dollar edged up 0.12% to VND 24,970 on the black market. Year-to-date, the dollar has increased by 0.61% against the dong. Globally, the dollar reached an eight-week high against major peers on Monday, with traders adjusting expectations for aggressive rate cuts by the Federal Reserve due to the resilient U.S. economy. The yen, Australian dollar, New Zealand dollar, and euro all saw declines against the stronger dollar. The dollar index hit 104.18, its highest level since December.

Outlook: Scrap imports into Vietnam are expected to stay low during the upcoming Lunar holidays as buyers are absent. Traders predict that domestic prices will receive short-term support post-holidays.