- Longs weighed down by excess inventory amid dull demand

- Flats pressured by excess supply, imports

- Lunar holiday lull may offer Indian mills scope to raise offers

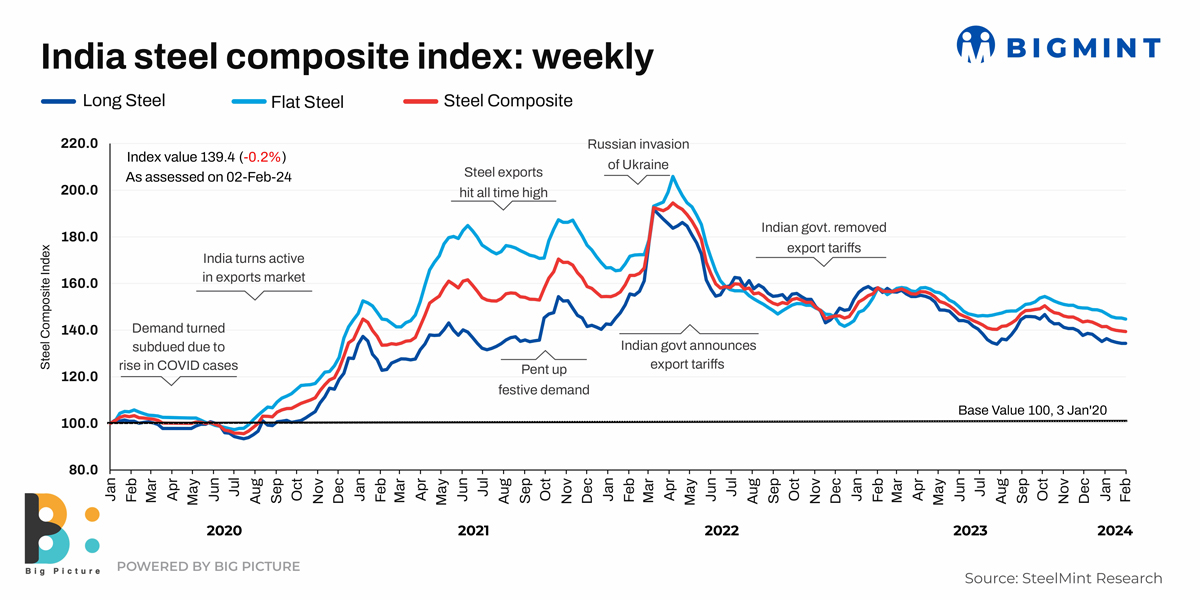

Morning Brief: The India Steel Composite Index remained stable for the week ending 2 February, 2024. It may be recalled, in the preceding week, the index had fallen to a two-year low. But the market can take heart from the fact that the index did not experience a further drop but remained flat at 139.40 points compared to the previous close of 139.60.

Factors which kept index stable last week

1) BF rebars weighed down by inventory: In the blast furnace-route rebar space, sluggish demand and need-based buying led to a rise in inventory by 8% or an additional 40,000-50,000 tonnes (t). Thus, January saw a stock pile-up of over 600,000 t which continued into early February. BigMint heard, the recent price hike of INR 500-1,000/t ($6-12/t) effected by tier-1 mills failed to get absorbed in a market already plagued by dull demand. The demand no-show is stemming from the fact that most pre-election infrastructure projects have been concluded or will close shortly. Thus, steel requirement has also tapered off despite Q4 being the best season from the demand perspective. Key bulk buyers have reduced purchases by almost half.

Trade-level BF-route prices hovered at INR 51,700/t ($623/t) exy-Mumbai and project prices, at INR 50,000-50,500/t ($602-608/t) FOR levels.

2) IF rebar sales sluggish despite discounts: Induction furnace mills, which command a larger 65-70% of the rebar market, are also nursing large inventory levels as they were able to sell only around 50% of their daily production amid a sustained liquidity crunch in the market. Thus, inventory volumes rose 25-30% in January. But mills were unable to lower their prices too much since sponge iron and billets prices have been fluctuating. The monthly average ex-Mumbai price in January dipped slightly to INR 48,700/t ($587/t) against December 2023’s INR 48,750/t ($587/t). Mills resorted to discounting but sales did not exactly perk up.

3) Trade-level flats remain range-bound: In flats, trade-level hot rolled (HR) coil prices stood flat w-o-w at INR 54,000/t ($651/t) while CR coil prices rose a modest INR 300/t ($4/t) to INR 62,000/t ($747/t). The range-bound trend was a function of the excess supply pressure amid subdued and need-based demand. Around 60,000 t from NMDC’s Nagarnar plant plus some amount from JSPL’s recently-commissioned 5.5-mtpa HSM at Angul are adding to domestic HRC supplies.

That apart, imports are dampening prices. Bulk HRC and plates imports in January touched over 586,451 t, surpassing December 2023 levels of 529,661 t.

“Domestic HRC and CRC prices stayed range-bound, increasing in some markets amid expectation of a hike in list prices of mills for February 2024 sales. Traders’ market demand is still lacklustre; participants are awaiting clarity on private mills’ February list tags and price support for January,” a source said.

4) Exports offers lacklustre amid small deals: The exports segment did not really have much to write home about except that offers were stable. Quotes to the Middle East remained flat w-o-w at $635-640/t CFR in a business-as-usual scenario, especially since Chinese quotes were stable.

So were the offers to the European Union, at $720-725/t CFR Antwerp. A deal of 20,000 t was sealed at similar price levels. Domestic EU prices remained propped up at $811-833/t, ex-works due to limited supply.

A few small deals were clinched for Vietnam while offers were flat at $610-615/t. With the Lunar holidays approaching, Southeast Asia is rather quiet.

Outlook

Prices may throw up a mixed trend in the short term. Longs, having already experienced a recent hike, are expected to remain stable especially since some production cuts may happen.

Domestic flats, on the other hand, may see an INR 1,000-1,250/t ($12-15/t) raise on the back of rising iron ore and coking coal prices on a quarterly basis. But the market is keenly awaiting mills’ list prices for February and the rebates for January. The buzz is, the price hike may not get absorbed because of excess supply unless buyers are offered handsome discounts. In such an eventuality, the potential price hike will get negated.

It was also heard, some tier-1 mills may opt for short maintenance schedules keeping excess supply in mind.

Export offers are a mixed bag. These are likely to remain a bit deadpan from other exporting countries till the Lunar holidays get over. But Indian mills may try to seize opportunities here by quoting higher in the absence of China, Japan and Vietnam.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

SteelMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, SteelMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.