The domestic steel scrap index (end-cutting) in Mandi Gobindgarh, as reported by BigMint on 3 February 2024, recorded a rise of INR 300/t, settling at INR 37,500/t on a delivered-at-plant (DAP) basis. Mills in Mandi are prioritising the procurement of domestic steel scrap at moderate levels due to the unviability of imported scrap prices at the moment. The observed price disparity has led to a lower level of buying interest in imported scrap.

In Mandi, the scrap arrival this week has been slightly slow, prompting mills to shift their focus towards procuring sponge iron for their steel-making charge mix. The supply of sponge iron is being sourced from the Durgapur market.

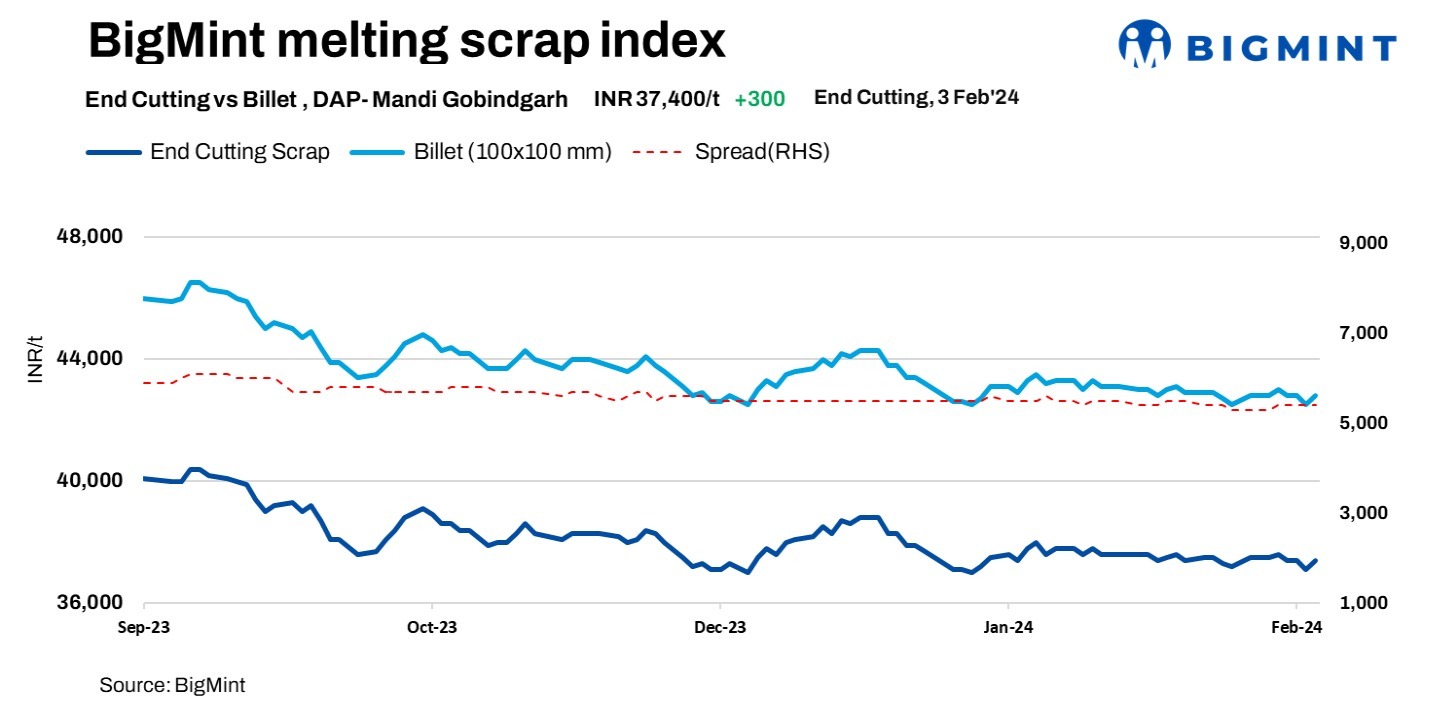

Semis’ market

In Mandi, the steel ingot prices recorded an increase of INR 300/t, reaching INR 42,800/t during reporting and price normalisation. At the same time, prices in various key markets witnessed a rise ranging from INR 100/t to INR 200/t today.

In the final trading session yesterday evening, ingot prices experienced an increase of INR 200/t as spot demand emerged in the market. However, today, buyers remained silent, and the market witnessed a pause in buying with a slower rate of increase.

Raw materials price update

In Mandi, the cost of sponge iron (CDRI) stayed constant at INR 31,200/t. Concurrently, pig iron (steel grade) prices in Ludhiana remained unchanged at INR 39,500/t on a delivered-at-plant (DAP) basis.

Overview of other markets

On 3 February, 2024, ship-breaking melting scrap prices in Alang, Gujarat, showed stability d-o-d. According to BigMint’s evaluation, HMS (80:20) prices were reported at INR 34,000/t ex-yard. Although, semi-finished steel prices saw a decrease in the previous trading session, the presence of moderate buying inquiries for scrap in the region encouraged suppliers to keep their offers stable today.

Weekly trend of imported scrap market

In India, demand for imported scrap remained sluggish as buyers hesitated due to the gap between bids and offers. Shredded scrap offers from Europe, on a weekly average, saw a slight decrease of $1/t, reaching $414/t CFR Nhava Sheva compared to the previous week’s $415/t CFR. Despite the overall tepid market conditions, some transactions were finalised during the week, but notably, these deals were sourced from Central America, West Africa, and Germany. Specifically, 500 t of HMS (80:20) were secured from Central America at $395/t CFR, approximately 2,500 t of HMS (80:20) were obtained from West Africa at $387-395/t CFR, and around 1,200 t of CR busheling scraps were booked from Germany at $415/t CFR.

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic Vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $390-$398/t, which equates to approximately INR 35,197/t(including freight),while local scrap-HMS(80:20) prices in Mumbai remained stable at INR 32,500/t d-o-d.

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,050/t.

To see SteelMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – info@steelmint.com.