Domestic induction furnace finished long steel offers witnessed a downtrend in prices. Prices dropped by INR 300-1,100/t. Trade reference prices for hot rolled coil (HRC) and cold rolled coil (CRC) fell by INR 100-500/t.

Iron ore and pellets

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, remained stable w-o-w at INR 9,850/tonne (t) DAP Raipur on 2 February, 2024. Total deals of 21,000 t were recorded from the Raipur region in the last one week. Buyers booked need-based material and remained cautious about bulk deals in expectation of price reduction.

- A southern India-based miner has concluded around 80,000 t of iron ore fines (Fe 54%) and 80,000 t of lumps (Fe 54%, 6-40mm) export deal recently, sources informed BigMint. It was heard that deals for the fines and lumps were concluded at around $104/t and $108/t CFR China, respectively. Notably, around 33 million tonnes of iron ore were exported from India in calendar year 2023 (CY’23).

- On 27 January, NMDC Bacheli had auctioned off 21,000 t of DRCLO (10-40mm, Fe 67%), which got booked at INR 7,900/t against the base price of INR 7,280/t and 50,400 t of fines (Fe 64%) got booked at INR 5,610/t against INR 5,350/t. Also, NMDC Kirandul had auctioned 21,000 t of iron ore fines (Fe 64%) that got booked at INR 5,440/t against the base price of INR 5,350/t. Prices are inclusive of royalty, DMF and NMET.

- Odisha Mining Corporation (OMC) is likely to stop the iron ore dispatches from its Daitari mines from 1 February, 2024 onwards as it is awaiting clarification for excess dispatch. Notably, Daitari mines have EC of 5 mnt for FY’24, out of which 4.968 mnt material was dispatched. Total production from OMC stood at 31 mnt in CY’23, up by 11% y-o-y.

- Asia-Pacific Supramax dry bulk (cargo capacity 50,000-55,000 t) freight rates for an iron ore-loaded vessel from the east coast of India to China was recorded at $15/tonnes (t) on 31 January, 2024, recording an increase of around $1/t w-o-w, according to BigMint’s assessment. Dry bulk freight trade activities have decelerated, experiencing reduced trading engagement as Chinese mills concluded restocking efforts ahead of the upcoming holidays.

Coal

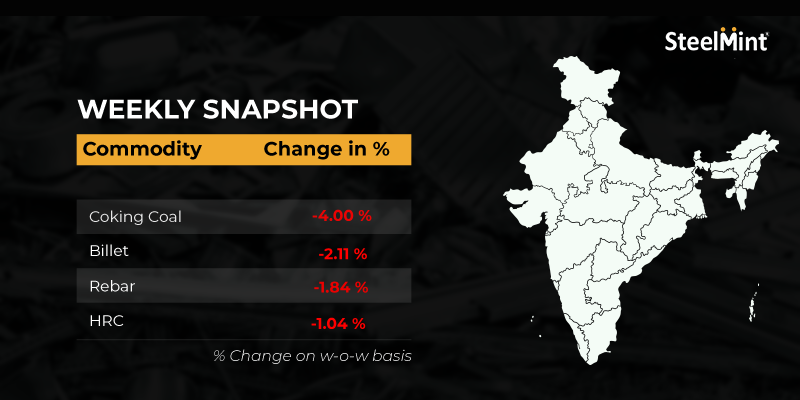

- Australian premium hard coking coal prices dropped by 2% w-o-w to $322/t FOB and $336/t, CNF on 3 February, 2024 amid reduced offer levels.

- RB1 (6000 NAR) grade prices remained stable w-o-w at $92/t FOB. Also, RB3 remained unchanged w-o-w at $63/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port were recorded at INR 7,300/t, down by INR 400/t w-o-w.

Ferrous scrap

- In India, demand for imported scrap remained sluggish as buyers hesitated due to the gap between bids and offers. Shredded scrap offers from Europe, on a weekly average, saw a slight decrease of $1/t, reaching $414/t CFR Nhava Sheva compared to the previous week’s $415/t CFR. Similarly, HMS (80:20) offers dropped by $3/t w-o-w, standing at $394/t CFR Nhava Sheva, down from $397/t CFR.

- Despite the overall tepid market conditions, some transactions were finalised during the week, but notably, these deals were sourced from Central America, West Africa, and Germany. Specifically, 500 t of HMS (80:20) were secured from Central America at $395/t CFR, approximately 2,500 t of HMS (80:20) were obtained from West Africa at $387-395/t CFR, and around 1,200 t of CR busheling scraps were booked from Germany at $415/t CFR.

- Major Indian ports saw a substantial decline in imported scrap, receiving 217,555 t in the first two weeks of January 2024, marking a 61% m-o-m decrease from the previous month’s 556,559 t. These figures are provisional and subject to revision with future updates and do not represent the final volume for the entire month.

Ferro alloys

- Silico manganese

Indian silico manganese prices elevated to a 3-month high; production curtailment and active inquiries attributed domestic silico manganese prices in India to rise. Additionally, export volumes have also increased, which has caused material shortages resulting in domestic price hikes. As per BigMint assessment, Silico manganese (60-14) was traded at approximately INR 66,900-67,600/t ($806-$814/t) exw Durgapur, Raipur, and Vizag up by INR 1,850/t ($22/t) on 2 February, 2024. - Ferro manganese

Prices for ferro manganese (HC70%) have increased due to increased export inquiries and a restricted supply on the domestic market. Ferro manganese offers on 2 February in Durgapur and Raipur, as reported by BigMint, were INR 67,000 to INR 67,700/t ($807-$816/t), with an additional INR 1,250/t ($15/t). - Ferro silicon

Indian ferro silicon (FeSi:70%) prices have diminished by INR 900/t ($11/t) ex-Guwahati and Bhutan. Post-BIS renewals, Bhutan rolled over its prices and now the announcements of new offers are much awaited which made ferro silicon prices to decrease in both the regions. As of 2 February, SteelMint reported ferro silicon prices in India at INR 108,600/t ($1,308/t), down INR 1,400/t ($17/t) exw-Guwahati and INR 109,600/t ($1,320/t) exw-Bhutan, suggesting a price fall of INR 400/t ($5/t). - Ferro chrome

On 2 February, Indian ferro chrome (HC 60%, Si:4%) prices remained curbed as buyers seemed hesitant in accepting higher offers. Prices inched down by INR 300/t ($4/t), reaching INR 118,700/t ($1,433/t) exw-Jajpur. The buying in the market happened only when required, this could also be a reason for price staying largely stable. Meanwhile, 304 grade stainless steel prices remained unchanged at INR 173,000/t ($2,085/t) exw-Mumbai w-o-w. The stability in prices can be attributed to limited inquiries in this sector.

Semi-finished

- Indian semi-finished steel prices decreased as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 50-350/t across regions, with a major decrease of INR 350/t seen in Raipur, Raigarh and Ramgarh. However, billet prices in Jalna and Chennai rose by INR 100-500/t. Similarly, sponge iron prices also decreased in key locations by INR 50-600/t, with a major decrease of INR 600/t seen in Ramgarh market. However, sponge iron prices only in Hyderabad edged up by INR 100/t.

- Neelachal Ispat Nigam Limited (NINL) is set to hold an auction for about 1,400 tonnes of melting scrap, comprising pooled iron fines, LRS fines, pig iron chips, and PCM scrap, originating from its Kalinganagar plant in Odisha on 8 February, 2024.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for a total of 30,000 t on 30 January, 2024. The entire quantity was booked at an average price of INR 35,750/t, exw, which was down by around INR 400/t from the last auction held on 17 January, 2024.

- Indian DRI (Direct Reduced Iron) exports offers remained stable in Nepal at $360/t on CPT Raxaul, and decreased by approximately $7/t in Bangladesh reaching $365/t on CPT Benapole.

Finished-long steel

- Finished Long Steel (IF Route):India’s induction furnace route finished long steel prices remained range-bound on a weekly basis, observing slight variation in prices. Moderate buying activities were observed at the start of the week. However, it slowed down later, as buyers opted for wait-and watch mode amid bid-offer disparity. Marginal fall in prices of sponge iron as well as steel billet and uncertain market direction led to the current market scenario of the finished steel. Participants expect such volatility to persist in the near term.

- On a weekly basis, in rebar steel prices fluctuated in the range of INR 100-700/t across regions while few markets remained stable also as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 42,600-43,000/t exw Raipur, INR 47,700-48,300/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 45,600-46,000/t exw Raipur

- Trade reference prices of wire rod hovering at INR 42,700-43,100/t ex Raipur.

- BF-route rebar: Trade-level prices of blast furnace (BF) route rebars rose marginally on weekly basis across major markets as tier-1 mills increased their list prices by INR 500-1,000/t in the last week of January, 2024. Inventories with tier-1 mills have registered 8% rise m-o-m in January, 2024. Demand in the trade segment remained weak last month.

- BigMint’s weekly price assessment for rebars (12-32 mm, BF-route, IS 1786, Fe500D) for the trade segment rose by INR 300/t to INR 51,700/t, exy-Mumbai, excluding GST at 18%.

- In the projects segment, prices are currently hovering at INR 50,000-50,500/t on FOR Mumbai basis. Buyers procured on urgent requirement basis last month.

Finished flat steel

- As of January 30, 2024, the bi-weekly benchmark evaluation for HRCs stood steady at INR 54,000/t, while CRCs witnessed a price increase of INR 300/t, reaching INR 62,000/t.

- In the domestic market, prices remained stable with an excess supply of materials and influx of imports. Buyers are cautious with increase in bargaining activity resorting to need-based buying at discounts.

- Indian steel mills maintained steady offers for HRC (SAE1006) to the Middle East at $635-640/t CFR, securing a significant 20,000 t export booking by a major Indian mill. In Europe, Indian HRC exports (S275, 3mm) remained unchanged at $720-725/t CFR Antwerp, with 20,000 t booked at around same price levels. The deliveries pertain to early March 2024. Additionally, a prominent Indian steel major sold 1 rake (approx. 2,750 t) of HRC for Nepal at around $615-620/t ex-mill (equivalent to $630-635/t CFR) for February 2024 deliveries, as per reliable sources.

- Imports of HRCs and plates increased in January 2024 to 586,451 t compared to December 2023.

- Looking ahead, private flat steel manufacturers are expected to increase their list prices for February owing to increase in raw material prices, while uncertainty remains regarding rebates or price support for January.