- OMC suspended iron ore dispatches from Daitari mines

- Few steel mills operating at lower capacities

- Few merchant miners have exhausted their EC limits

BigMint’s weekly Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,800/t ex-mines on 3 February, 2024. A deal of 25,000 t fines was recorded of standard grade Fe 62% at INR 6,000/t ex-mines in this publishing window.

The market remained muted. Most of the sellers dispatching the booking material while the EC limit was also consumed by the merchant miners. However, buyers remained hesitated to book material amid lower margins in the sponge and finished steel as prices fell by INR 1,000-1,400/t in the last one month in the Odisha region.

A market participant said that few sponge and steel plants in the eastern India have lowered their capacity utilization due to negative market dynamics which lowered iron ore demand in the region. However, material availability dropped as the financial year came to an end. The lunar holiday in China may support the iron ore market in the eastern region following the decreased demand for export. This will keep iron ore prices under control for the next few days in Odisha.

Another participant expressed that fines prices may be decreased in the coming days as pellet prices are under pressure in both export and domestic markets. However, due to remaining in demand, lumps will sustain the current level. The OMC is the major miner in Odisha and everyone waiting for the next auction to get clarity about prices in the market.

On the other hand, a few miners already sold the material of the remaining EC of the next few days and regularly supplied the material which fulfills demand in the market.

Odisha Mining Corporation (OMC) is likely to stop the iron ore dispatches from its Daitari mines from 1 February, 2024 onwards as it is awaiting clarification for excess dispatch. Notably, Daitari mines have EC of 5 mnt for FY’24, out of which 4.968 mnt material was dispatched.

Rationale:

- T1- One deal was taken from Odisha but not considered in this publishing window under price computation. It was given 0% weightage for index calculation.

- T2- SteelMint received thirteen (13) offers and indicative prices under T2 trade deals in this publishing window. Ten (10) were taken into consideration and given 100% weightage. To check SteelMint’s iron ore assessment, pricing methodology, and specification documents Click here.

Factors driving prices:

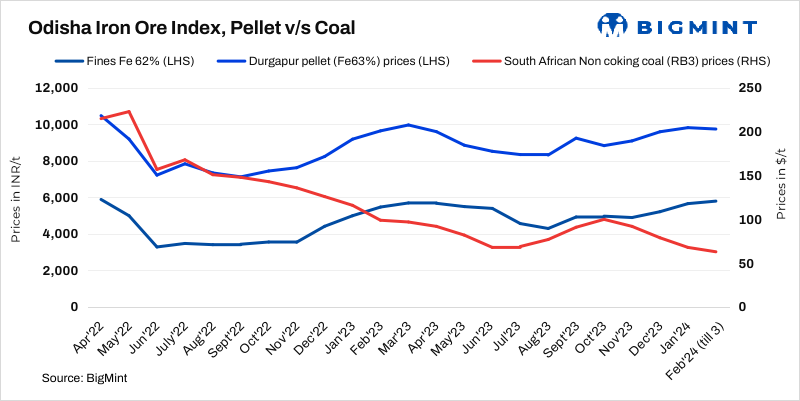

- Barbil pellet prices largely stable w-o-w: Pellet (6-20 mm, Fe 63%) prices in Odisha’s Barbil decreased marginally by around INR 100/t w-o-w. The current assessment stands at INR 9,100/t loaded to wagon. However, pellet (Fe 63%, 6-20 mm) prices in Durgapur largely remained stable w-o-w at INR 9,750/t exw on 2 February.

- Drop in fines export prices: BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index decreased by $5/tonne (t) w-o-w to $86/t FOB east coast on 1 February 2024. A deal of 55,000 t Fe 57% fines was heard at $88/t FOB India last weekend, however, it is yet to be confirmed by the seller. As per sources, most of the Chinese mills almost completed restocking for iron ore ahead of the Lunar holidays, so buyers remained cautious about booking material at higher offers amid low steel margins and production.

- Rourkela sponge iron prices stable w-o-w: BigMint’s assessment for sponge iron C-DRI (FeM 80%) prices in Rourkela remained stable at INR 26,450/t exw on 3 February compared to last week. However, steel billet (100*100 mm) prices in Rourkela inched down by INR 100/t w-o-w to INR 38,500/t today.

Outlook

Odisha iron ore prices are likely to remain volatile in the coming days following pressure from pellet and sponge prices, However, tight availability of the material may keep prices supported in the coming days.