The global ferrous scrap prices exhibited a mixed trend this week. In South Asia, Indian buyers opted to stay on the sidelines, citing significant price disparities. Meanwhile, Pakistani buyers slowed down their purchases in light of national elections taking place within the week. In contrast, Bangladeshi buyers actively engaged in procuring scraps from the seaborne market. This surge was fuelled by improved demand post-elections, as well as enhanced production and sales in the domestic steel market. Additionally, the market benefited from an easing of letters of credit (LC) approvals from banks.

In Japan, H2 scrap export offers experienced a w-o-w decline, influenced by Tokyo Steel’s recent price cut and subdued demand from key importing nations ahead of the Lunar New Year holidays.

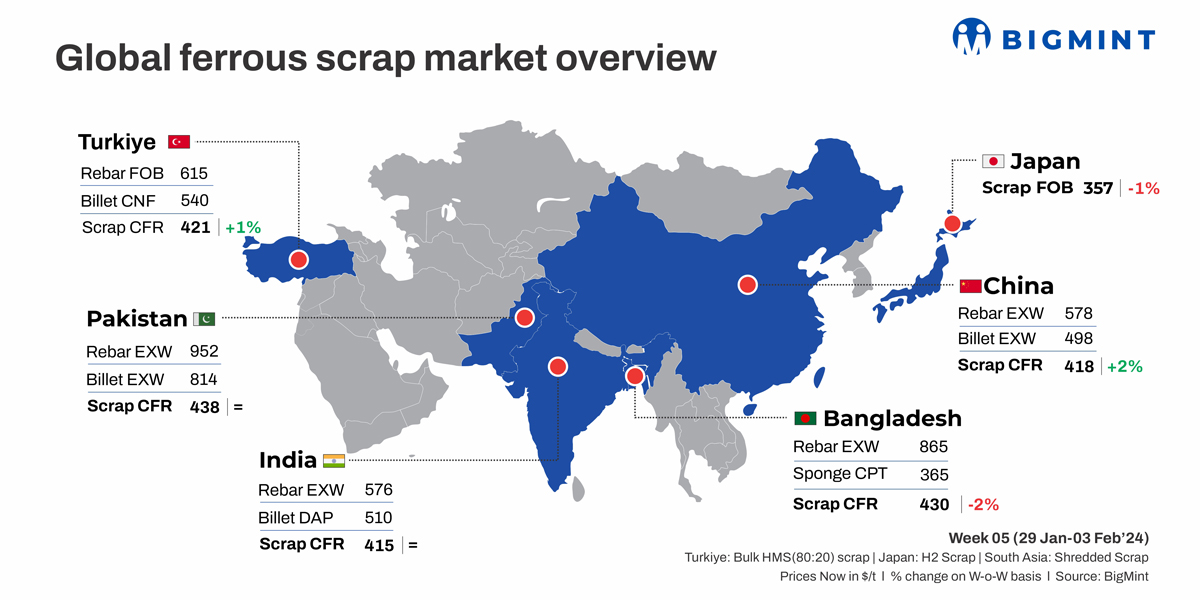

Turkiye: Turkish imported ferrous scrap prices experienced a slight uptick in anticipation of an impending restocking surge. Indicative tradable values for HMS (80:20) remained relatively steady, primarily within the range of $422-424/t CFR.

Throughout the week, approximately 8-10 bulk deals, originating from the UK, US, and Benelux, were reported at a price range of $415-440/t on a CFR Turkiye basis, covering various mixed grades, including shredded, HMS, PNS, and bonus scrap.

While the market displayed some fluctuations within the $420-425/t CFR range, there is an expectation that pricing will stay within bounds in upcoming deals for March shipments. The market dynamics are projected to witness increased activity in the first half of February.

BigMint’s assessment for US-origin bulk HMS (80:20) recorded a $3/t w-o-w rise, reaching $422/t CFR Turkiye.

The scrap-to-rebar spread was evaluated at $195-200/t, considering Turkish exported rebar assessed at $615-620/t FOB and accounting for potential adjustments in scrap prices.

India: In India, the demand for imported scrap remained sluggish as buyers hesitated due to the gap between bids and offers. Shredded scrap offers from Europe, on a weekly average, saw a slight decrease of $1/t, reaching $414/t CFR Nhava Sheva compared to the previous week’s $415/t CFR. Similarly, HMS (80:20) offers dropped by $3/t w-o-w, standing at $394/t CFR Nhava Sheva, down from $397/t CFR.

Despite the overall tepid market conditions, some transactions were finalised during the week, but notably, these deals were sourced from Central America, West Africa, and Germany. Specifically, 500 t of HMS (80:20) were secured from Central America at $395/t CFR, approximately 2,500 t of HMS (80:20) were obtained from West Africa at $387-395/t CFR, and around 1,200 t of CR busheling scraps were booked from Germany at $415/t CFR.

Major Indian ports saw a substantial decline in imported scrap, receiving 217,555 t in the first two weeks of January 2024, marking a 61% m-o-m decrease from the previous month’s 556,559 t. These figures are provisional and subject to revision with future updates and do not represent the final volume for the entire month.

Pakistan: In Pakistan, market activities experienced a slowdown during the week, largely influenced by the imminent elections. Buyers anticipate a return to normalcy in the market post-elections. Shredded scrap offers from Europe, on a weekly average, remained within the range of approximately $438-439/t CFR Qasim.

A representative from a steel mill noted, “Business has been sluggish throughout this entire month, attributed to the upcoming February elections. There is a noticeable absence of significant infrastructure activities in the country at the moment.”

Another official from a steel mill added, “We are currently on hold due to the depressed market conditions. Finding a seller below $430/t is challenging. Payment processing from the bank is posing difficulties with the upcoming elections and weakening Forex.”

During this period, a transaction involving approximately 500 t of HMS (80:20) was concluded from the Middle East at $409/t CFR, and an additional 100 t of HMS (80:20) was processed at $410/t.

Bangladesh: In Bangladesh, the demand for imported scrap has seen a resurgence following the January national elections, with improved LC approvals and a boost in domestic steel production and sales. Shredded scrap offers from Europe remained steady at $439/t CFR Chattogram levels on a weekly average. Meanwhile, HMS (80:20) experienced a $4/t drop, settling at $415/t CFR compared to the previous week’s $419/t CFR.

Significant bulk deals were reportedly closed, including a US recycler selling two bulk cargoes of 30,000 t of HMS and shredded scrap to a Bangladeshi mill. Additionally, another Bangladeshi mill secured bulk HMS (80:20) and PNS scrap from Australia at around $414/t and $424/t CFR, respectively.

According to a trader, “Bookings were subdued in December due to election-related factors and issues with LC openings. Now that the elections have concluded and LC approvals have eased, along with steel mills resuming normal production after a reduction in December, there is a noticeable uptick in fresh bookings.”

Japan: Japan’s H2 scrap export offers experienced a weekly decline following Tokyo Steel’s price reduction announcement, coupled with sluggish demand from key importing nations. In the latest assessment by BigMint, Japanese H2 scrap export offers witnessed a drop of JPY 800/t ($5/t) to JPY 53,000/t ($362/t) FOB Tokyo Bay, compared to the previous week’s JPY 53,800/t ($367/t) FOB.

The FAS H2 grade scrap collection prices in Kanto Bay experienced a decline, dropping to JPY 49,500-50,500/t ($338-345/t) for the week from JPY 51,500-52,500/t ($351-358/t) in the previous week.

South Korea: In South Korea, steel mills abstained from procuring scraps from the seaborne market as they found cost-effective alternatives within the domestic market. Despite ongoing price increases by steel mills, domestic scrap prices continued to be more affordable compared to offers for imported scrap.

The scrap inventory of leading South Korean steel producers rose by 2%, amounting to 11,000 t, reaching a total of 736,000 t compared to the previous week.

Additionally, as of 29 January, fresh scrap arrivals at major ports recorded a reduction to 56,164 t, marking a decrease of approximately 5,400 t compared to the previous week.

Vietnam: Vietnamese mills adopted a “wait-and-see” approach due to discrepancies between bids and offers following a recent reduction by Tokyo Steel and on approaching of Lunar New Year holidays. Despite a decline in offers by approximately $5/t w-o-w to $400/t CFR Vietnam, there has been no visible buying interest. Bids have consequently fallen to around $395-400/t CFR levels for H2 grade scrap.

A Japanese trader remarked, “Scrap demand in Vietnam is notably limited, and finding buyers has become challenging following Tokyo Steel’s price cut. Despite a decrease in export offers of approximately $5/t and JPY 1,000-2,000/t in the domestic market.”