- Need-based procurements ahead of polls pulls down offtake

- Market fails to absorb price hike from tier-1 mills

Rebar inventory with tier-1 mills increased by around 8% or 40,000-50,000 tonnes (t) in January 2024. Currently, the volumes have crossed 600,000 t m-o-m from the levels seen in December, 2023. It may be mentioned that the tier-1 mills have around 30-35% share in the total rebar market, with the induction furnace (IF) segment enjoying the majority 65-70%.

Reasons for rising inventory:

1. Need-based procurements ahead of poll season: Demand was sluggish in general and need-based from the project segment. This is mainly due to the fact that most pre-election projects have been concluded or are nearing completion, allowing for a tapering off in steel demand for the same. Major buyers have sharply reduced bulk purchases.

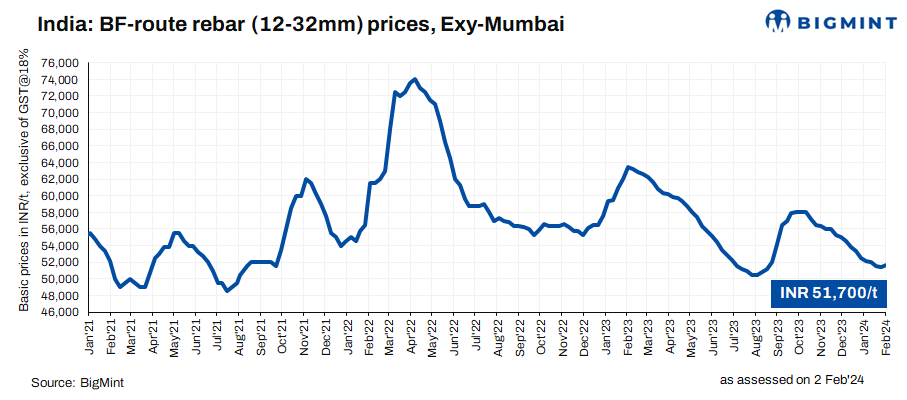

2. Market fails to absorb price hike: Tier-1 mills raised prices in end-January by INR 500-1,000/t ($6-12/t) although this was not replicated at the trade level. However, sources informed BigMint that the price hike is not getting absorbed in the market and buyers are mostly staying away. Retail prices are at INR 51,500-52,000/t ($621-627/t) exy-Mumbai and project prices at INR 50,000-50,500/t ($603-609/t) FOR Mumbai levels.

3. IF-route demand dull despite discounts: Rebar too faced need-based procurements amid sluggish demand but the mills here were unable to lower prices too much even as they struggled to sell because sponge and billet prices fell marginally m-o-m. IF mills resorted to discounting as inventory rose 25-30% m-o-m in January. The monthly average ex-Mumbai prices of INR 48,750/t ($588/t) in December 2023 dipped slightly to INR 48,700/t ($587/t). Mills were able to sell only around 50% of their daily production amid a sustained liquidity crunch in the market.

The monthly average price gap between BF-IF rebars stood at INR 3,000-3,500/t ($36-42/t) in January 2024 in the key market of Mumbai.

Outlook

Doubling up under the twin whammy of sluggish demand and rising inventory, many of the tier-1 mills are mulling production cuts in February which cumulatively may amount to around 100,000 tonnes. Since tier-1 mills have already opted for a recent hike, some stability in prices is expected in near term.