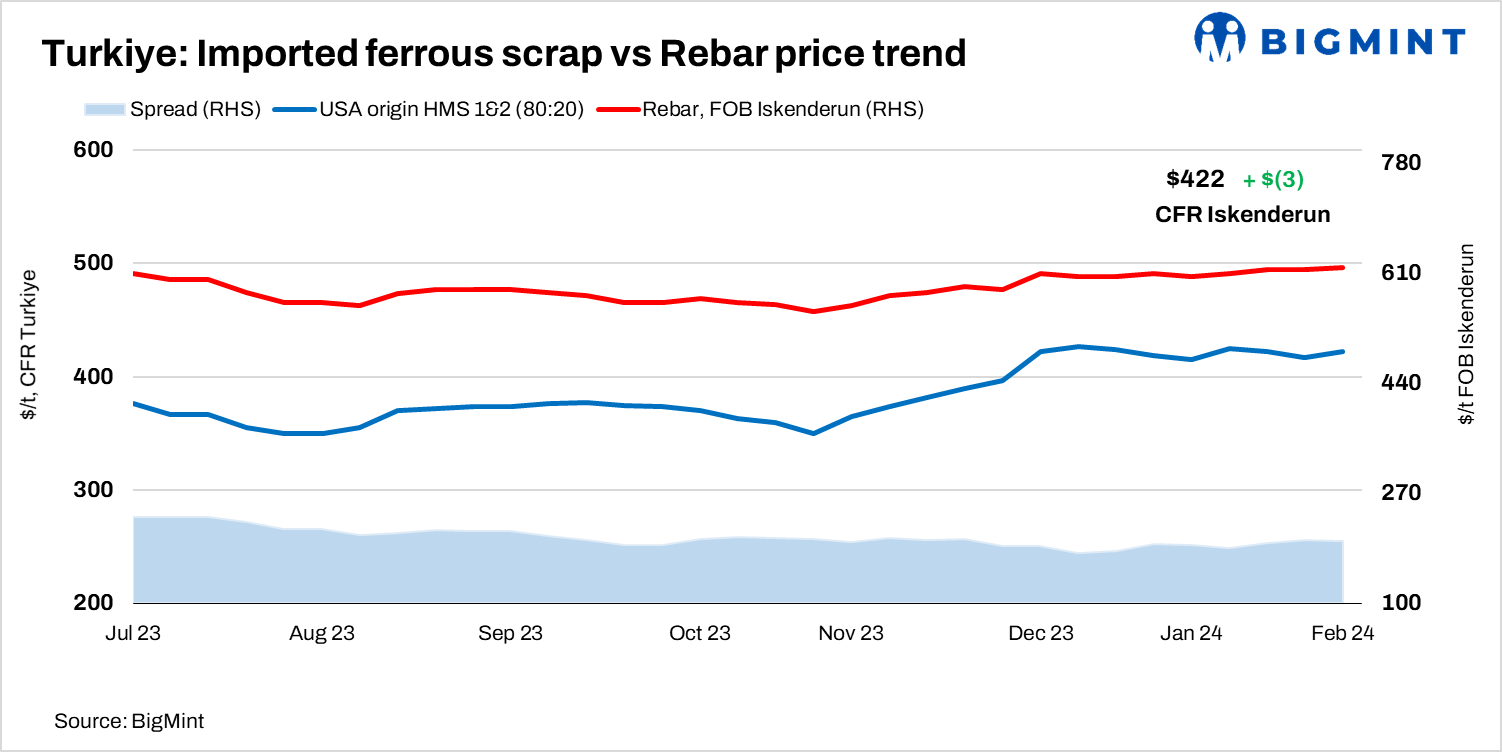

Towards the close of January, Turkish imported ferrous scrap prices saw a marginal increase in anticipation of an imminent re-stocking surge. Traditionally, indicative tradable values for HMS (80:20) remained relatively stable, primarily within the range of $422-424/tonne (t) CFR.

While the market exhibited some fluctuation within the $420-425/t CFR range, there is an expectation of pricing remaining within bounds in the upcoming deals for March shipments. The market dynamics are projected to witness heightened activity in the first half of February.

BigMint’s assessment for US-origin bulk HMS (80:20) recorded a $3/t w-o-w rise, reaching $422/t CFR Turkiye.

The scrap-to-rebar spread was evaluated at $195-200/t, considering Turkish exported rebar assessed at $615-620/t FOB and taking into account potential adjustments in scrap prices.

Despite a reduction in rebar demand accompanied by lower prices, the collection costs for Baltic-origin HMS (80:20) have maintained their elevation. Turkish mills aim to achieve figures below $420/t CFR, but challenges persist as sellers encounter difficulties in scrap collection. Interestingly, despite the industry facing subdued rebar demand, there is an urgent need to secure March shipments. While the majority of mills target $410/t CFR for HMS (80:20), hurdles in scrap collection processes currently make this objective unattainable, according to market insiders.

In 2023, Turkish mills experienced a 10% y-o-y decrease in ferrous scrap imports, totalling 18.78 million tonnes. Although there was an uptick in imports in the final months of the year driven by re-stocking activities, the overall decline aligns with the reduction in Turkiye’s crude steel output. The subdued demand for finished products in export markets contributed to a 4% y-o-y decrease in Turkish crude steel output, totalling 33.7 million tonnes, as reported by the World Steel Association.

Recent deals

US-origin cargo was booked by a Mediterranean region-based mill comprising HMS (80:20) at $422/t on a CFR Turkiye basis.

US-origin cargo was sold to a West Marmara-based mill comprising HMS (80:20) scrap at $421/t CFR Turkiye.

Benelux origin cargo was booked by the Aegean region-based mill at $415/t on a CFR Turkiye basis.

UK-origin supplier sold bulk cargo with Shredded and bonus scrap (40,000 t) at $442 CFR Turkiye.

US-origin bulk cargo with HMS (80:20), shredded, and bonus were booked at $420/t and $440/t on a CFR Turkiye basis.

Sweden-origin bulk cargo with HMS (80:20), shredded, and bonus were sold at $420/t and $440/t, respectively, on a CFR Turkiye basis.

Domestic market: In its recent sales round, Turkish steel producer Kardemir has implemented a price adjustment for billets, setting the S235JR grade at USD 585/t EXW, representing a $5/t increase from the second week of the month. Similarly, the B420 grade billet is now listed at $595/t EXW, reflecting a rise from its previous value of $590/t EXW. This price hike is attributed to escalating production costs, notably driven by increased labor expenses following successful negotiations by the Turkish metal workers union for higher wages.

Additionally, the recent benchmark interest rate hike by the central bank has further contributed to the overall cost uptrend. Kardemir is a prominent player in the Turkish steel industry, boasting a substantial 3.5 million tonnes per year production capacity. The company specializes in manufacturing blooms, billets, rebars, profiles, and various other steel products, strategically located in facilities in Karabuk.

Another Turkish steel producer, Kocaer Celik, has secured export orders totalling USD 27 million in the early months of 2024. These orders span the Middle East and North Africa (MENA) region, as well as the American continent. Operating three steel profile factories with a combined annual production capacity of 800,000 tonnes, Kocaer Celik is actively expanding its steel service center capacity. This expansion is geared towards processing steel profiles for the energy sector, with a targeted increase from 120,000 to 180,000 tonnes per annum.

Outlook: As per industry insiders, Turkish mills have commenced inquiries for March shipments, leading some sellers to exercise caution to maintain stability in near term. Anticipating increased demand, the upcoming week is expected to see a surge, prompting all EU suppliers to proactively present offers exceeding $422-425/t.