In the ship recycling sector this week, despite an improvement in vessel prices from the lows of 2023 and a notable surge in plate prices in Bangladesh, the number of confirmed sales in the recycling markets for 2024 have been limited. Ship owners seemed cautious about accepting offers in the low $500/LDT, as these levels were lower than those observed just a few quarters ago. Fortunately, there was a positive development with easing letters of credit (LC) restrictions in Pakistan and Bangladesh, sparking increased interest from both markets in making purchases. However, India is facing challenges due to declines in steel prices, making it difficult for end-buyers to compete with their stronger counterparts.

India

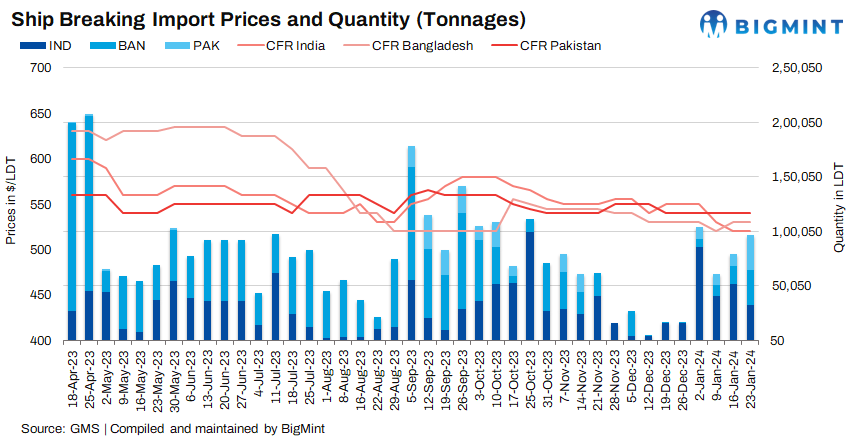

Throughout the week, prices for tankers and containers remained stable in India, influenced by a decline in the domestic steel market. Additionally, the rupee depreciated against the US dollar.

In contrast, Alang recyclers were experiencing positive outcomes, taking advantage of financial difficulties in neighbouring countries. This situation allowed recyclers to successfully finalise deals since the beginning of January. In a recent development, a Spain built container vessel had been sold by MSC – MSC JEMIMA (12,000 LDT) at USD 520-525/LDT, it includes $10/t worth of bunkers onboarded. Notably, this transaction is limited to a select few Alang yards adhering to specific standards.

Despite facing challenges, the Alang port continued to witness consistent arrivals. Nevertheless, local buyers expressed concerns about the future availability of units due to heightened competition.

The total tonnage received at Alang Port last week was 32,057 LDT.

Bangladesh

The Bangladeshi market experienced a sluggish week primarily due to a pronounced scarcity of recycling candidates persisting across all markets. This is despite an increase in LCs approvals and financing from various banks in the country, along with a significant $50/t surge in local steel plate prices.

The local port position also observed limited activity, with only a few fresh arrivals, as several recent arrivals concluded their journeys by being beached.

Rising global geopolitical tensions may contribute to an upswing in freight rates, as a backlog gradually forms and vessel owners redirect their ships away from the troubled Red Sea shipping lanes. This situation could lead to strengthening chartering levels and, consequently, an earlier-than-expected shortage of recycling candidates – possibly even before the arrival of Spring.

The total tonnage received at Chattogram Port last week was 32,218 LDT.

Pakistan

Throughout the week, there was an uptick in the availability of financing and viable LCs in Gadani. Unfortunately, due to the ongoing scarcity of recycling units in the industry, Pakistani recyclers could not finalise any deals.

Interestingly, only three vessels were observed at Gadani’s waterfront, and the total LDT was on par with competing countries like India and Bangladesh, where eight and seven vessels were present at their respective waterfronts. This underscores the prevalence of small LDT and discounted recycling tonnage in the current market.

Additionally, in February, Pakistan is poised for national elections, potentially leading to hesitancy or uncertainty in acquiring units until the official election results are known and any potential negative consequences unfold.

Lastly, following recent military actions by the US and the UK forces against Houthi targets in Yemen, tensions appear to be rising in Pakistan. Reports suggested that the country exchanged several missiles with neighbouring Iran, adding to the already delicate situation unfolding across the region.

The total tonnage received at Gadani Port last week was 31,967 LDT.