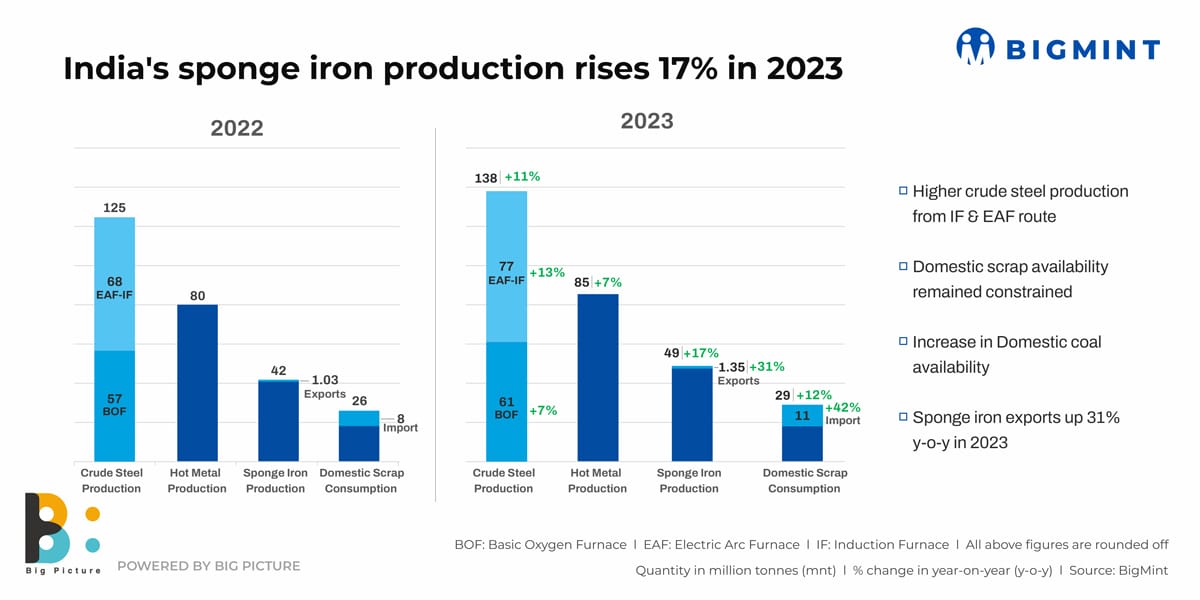

- Indian crude steel production up 11%, where as IF-EAF route registered 13% growth

- Domestic scrap generation affected due to GST crackdown

- Sponge iron exports rise over 30% y-o-y

Production of direct reduced iron (DRI), or sponge iron, in India increased by an impressive 17% y-o-y to around 49 million tonnes (mnt) in calendar year 2023 (CY’23) from a little under 42 mnt in CY’22, as per SteelMint data.

Sponge iron production rode the wave of a robust growth in domestic crude steel production, especially through the EAF-IF route. As per estimates, around 26% of domestic crude steel production is based on sponge iron.

Why did DRI output increase?

*Higher crude steel production: Sponge iron production increased due to the significant surge of around 11% in domestic crude steel production to nearly 138 mnt in CY’23. Notably, production from the IF-EAF route increased by 13% to 77.06 mnt in CY’23 from 67.68 mnt in CY’22. The IF-based steel producers, as well as EAF players, are the major consumers of sponge iron in India which, in most cases, plugs the deficiency of domestic scrap supply. Note that crude steel production from the BF-BOF route increased slower at 7% compared with the IF-EAF route. So, the marked overall increase in crude steel production was mainly sustained by higher sponge iron production.

*Lower domestic scrap generation: India’s consumption of ferrous scrap in steelmaking increased by 12% y-o-y in CY’23 to over 29 mnt. However, imports of ferrous scrap rose to over 11 mnt from 7.7 mnt in CY’22 – up sharply by 42%. This is partly because of low demand in major scrap consuming countries such as Turkiye, Bangladesh, Pakistan, etc. and redirection of seaborne cargoes into India amid high domestic demand.

But another, more significant, reason is the slower pace of domestic scrap generation when it comes to meeting exponential demand growth in the steel sector. The GST crackdown on the scrap market, an effort to streamline an informal domestic market, led to restricted domestic supplies. This encouraged higher DRI production as a substitute in IF-EAF steelmaking.

*Growth in domestic coal production: India’s production of non-coking coal used in the domestic rotary kiln-based sponge iron sector (over and above imports of South African coal) rose by an impressive 13% y-o-y in CY’23 to over 900 mnt from 802 mnt in CY’22. Coal-based DRI producers could sustain the growth in production due to higher domestic coal availability. It bears recall that domestic DRI producers are often unable to secure enough domestic coal supplies due to the government’s preferential allotment policy for the power sector.

Another reason supporting sponge iron production was the climbdown in global coal prices compared with 2022, as energy volatility lessened. This enabled domestic sponge players to secure imported coal cargoes at moderate prices, which boosted production.

*Exports up over 30% y-o-y: Although volumes were not very high, India’s exports of sponge iron increased by over 30% y-o-y to 1.35 mnt from 1.03 mnt in CY’22. This, too, played a role in supporting domestic production. The key export destinations were Nepal and Bangladesh, which ramped up sourcing following sustained growth in the crude steel capacities of these countries.

Outlook

Despite projected energy and technological transitions in the domestic sponge iron sector and the consequent possibility of disruptions, stable growth in production is anticipated.

SteelMint expects India’s production of sponge iron to increase in the coming years, although growth may not be as sharp as in CY’23 which, being a pre-election year, witnessed above-average growth in domestic steel demand and production. However, DRI output is likely to follow a steady growth path, thanks to a robust steel production outlook.

Leave a Reply