- Trade level HRC-CRC prices show mixed trend

- Labour shortages in some markets amid Navratri and Ugadi festivals

- Subdued buying interest, liquidity concerns persist

- Focus shifts to book reconciliation towards fiscal year-end

Trade-level hot rolled coil (HRC) and cold rolled coil (CRC) prices this week show a mixed trend. Prices remained mostly rangebound in the key markets of Mumbai, Faridabad and Chennai, but dropped in some other local markets, as per SteelMint assessment.

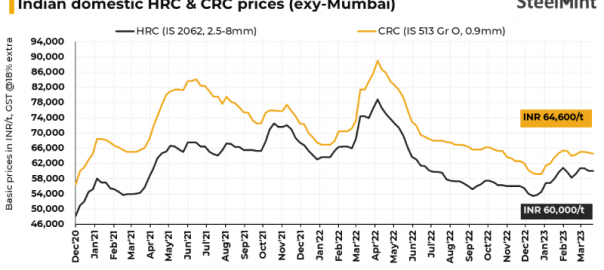

The weekly assessment of SteelMint’s benchmark HRC (IS2062, 2.5-8mm) stands at INR 59,500-60,500/t ($721-733/t) exy-Mumbai, same as last week. However, CRC dropped marginally by INR 200/t ($2/t) to INR 64,000-65,000/t ($776-788/t) exy-Mumbai. Prices are exclusive of GST at 18%.

(INR 1 = USD 0.012118 ; USD 1 = INR 82.5216)

Factors impacting the market:

1. Festivals and fiscal year-end: Trade market activities have remained slow since the beginning of March. “Holi at the beginning of the month and Navratri and Ugadi being observed this week have led to labour shortages in some markets, restricting market activities,” said a western India-based distributor source. Liquidity is another factor as the RBI increased bank lending rates in February. This also led to low buying interest among in the traders’ market, he added.

Furthermore, the financial year ends this month, hence both buyers and sellers are more focused on book reconciliation.

2. Indian HRC export prices rangebound: Export offers of Indian-origin HRC have remained rangebound this week amid global financial instability. SteelMint’s India HRC (SAE1006) export index dropped $4/t to $712/t FOB east coast this week. Indian mills have been offering at around $740-750/t CFR UAE for May shipments, but buyers in the Middle East are looking for cheaper alternatives.

Furthermore, active scouting of export opportunities in the European market has helped ease the inventory pressure on Indian manufacturers. Deals have been heard over the last one month with prices rising in each successive deal. Current offers hover at $830-840/t CFR Antwerp, although deals are yet to be concluded at these levels. This has helped in reducing the impact of low buying interest for Indian HRC in the UAE and Vietnam, which is the focus of SteelMint’s India HRC (SAE1006) export index.

“Domestic market prices in India are still higher than realisations from exports to the UAE or Vietnam. Hence the focus is more on the European market at present,” a source said.

Outlook:

Trade-level prices are likely to remain rangebound in the near term. Mills are looking to raise their list prices for early-April sales, factoring in elevated iron ore prices and good export exposure. India’s largest merchant iron ore mining company, NMDC, has increased list prices of iron ore fines by INR 200/t, with effect from 21 March. The miner has fixed prices for DR CLO (Fe 67%, 10-40mm) at INR 5,820/t and iron ore fines (Fe64% – 10mm) at INR 4,110/t FOR Bacheli complex, excluding royalty, DMF and NMET.

Leave a Reply