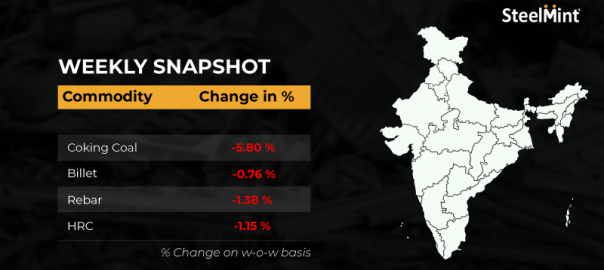

The domestic steel market witnessed negative price trends during week 11 ( 13 March-18 March, 2023). Semi-finished steel prices decreased in the range of INR 250-1,500/tonne (t).

Domestic induction furnace finished long steel offers saw downward trends. Offers declined by up to INR 200-1,000/t w-o-w. Trade reference prices for HRC and CRC edged down in the range of INR 100-1,000/t across region.

Iron ore and pellets

- SteelMint’s bi-weekly domestic pellets (Fe 63%) index, PELLEX, decreased marginally by around INR 50/t to INR 9,900/tonne (t) DAP Raipur today compared to the last assessment on 14 March, 2023. No deal was recorded in this publishing window as market participants showed least interest in buying pellets at current offers. Buyers are silent after the Odisha Mining Corporation’s (OMC’s) iron ore auction concluded on 16 March, 2023.

- Odisha Mining Corporation (OMC) has conducted an auction for 494,000 t of iron ore fines (Fe54-64%) and 404,000 t of iron ore lumps (Fe60-65%) on 16 March 2023. Around, 456,000 t of fines were booked at INR 3,150-6,600/t and 277,000 t of lumps were booked at INR 6,150-10,600/t. Bids remained close to the base price except for some lots for which prices increased by INR 50-650 for fines and INR 100-650/t for lumps. Earlier, miner had increased the base price for fines by up to INR 1,050/t and INR 490/t for both fines and lumps respectively.

- Steel Authority of India Ltd (SAIL) put up 20,000 t of iron ore tailings (Fe 58.55%-indicative) for auction from Barsua mines located in Odisha on 14 March, 2023. According to sources, the steelmaker received bids for the entire quantity at INR 4,600/t. Prices were ex-mines, including royalty, DMF, NMET, and an extra premium.

- SMIORE concluded its 221,000 t-iron ore auction held in Karnataka’s Bellary on 15 March, 2023. According to sources, 4,000 t of lumps (20-40mm, Fe59.20%) were booked at INR 4,310/t, 136,000 t of fines (Fe57-57.5%) got sold at INR 3,110-3,420/t, 60,000 t of fines (Fe57.6%) were booked at INR 3,445-3,455/t, 12,000 t of fines (Fe57.7%) were booked at INR 3,470/t and 8,000 t of fines (Fe58.7%) got sold at INR 3,435/t. Prices include royalty, DMF, and NMET.

- Vedanta sold around 12,000 t of iron ore lumps (6-20mm, Fe 56.5-58.5%), out of 28,000 t offered in auction from Karnataka on 15 March. As per market sources, the material was sold at INR 3,804-4,043/t. Prices exclude royalty, DMF and NMET.

- SteelMint’s India pellets (Fe 63%, 3% Al) export index FOB east coast was recorded at $123/t, up $5/t w-o-w despite sluggish pellets demand in the export market. As per market sources, one deal for 55,000 t of pellets (Fe 63%) is under negotiations and may get concluded at around $136-137/t CFR China. Another tender for pellets exports by an eastern India-based player was also heard to be under discussion.

Coal

- Australian premium hard coking coal prices plunged by $22/t w-o-w to $341/t FOB and $357/t CNF on 18 March, 2023 amid low buying interest. Indian and Chinese buyers were also on the sidelines as they are expecting prices to correct further. Portside prices of

- South African RB3 (4800 NAR) thermal coal at Vizag Port were recorded at 10,300/t, majorly stable w-o-w. RB1 (6000 NAR) grade prices have been up marginally by 2% w-o-w to $132.65/t FoB and RB3 prices inched up to $94/t FOB, up $1 w-o-w.

Ferrous scrap

- Indian imported ferrous scrap remained sluggish due to high offers in the global scrap market, whereas, minimal deals in containers took place throughout the week. Major players have had sufficient inventory for the next few weeks. However, there is good stock of domestic scrap in major regions available for immediate requirements. Recently, major ports in India like Chennai received around 28,000 t of bulk ferrous scrap booked by a major South Indian steelmaker. Furthermore, buyers are not willing to purchase scrap at the current price level and are waiting for the price to fall further.

- SteelMint’s assessment for imported shredded scrap in containers stood at $470-75/t CFR, down by $5-8/t w-o-w.

Ferro alloys

- In SteelMint’s assessment on 17 March 2023, Indian silico manganese prices were rangebound w-o-w to INR 74,000/t ex-Durgapur, down by 1%, INR 74,000/t ex-Vizag, nearly stable w-o-w, and INR 74,600/t ex-Raipur, down by 1 %. Prices of silico manganese remained rangebound because of mixed market trend in domestic markets.

- As on 17 March 2023, Indian ferro manganese prices were down by 3% w-o-w to INR 75,100/t ex-Durgapur and ex-Raipur at INR 76,000/t. Special steel demand remained subdued, and ferromanganese prices dropped as a result. Indian ferro chrome (HC60%) prices inched down by INR 3,000/t w-o-w to INR 115,800/t exw Jajpur owing to weak demand amid under pressure stainless steel prices, assessed on 16 March. Increased production in China also shifted country’s interest in domestic market from Indian ferro chrome. This has also impacted ferro chrome prices.

- According to SteelMint’s assessment on 17 March, Indian ferro silicon (70%) prices inched down at around INR 118,700/t exw Guwahati. While, Bhutan’s producers were offering at around INR 119,600/t exw. Slow buying forced producers to reduce prices marginally amid selling pressure.

Semi-finished

- Indian Semi finished steel prices decreased sharply as per SteelMint’s assessment, the domestic billets prices fell by INR 200-1,500/t across region with a major fall seen in Mumbai and Ahmedabad. Similarly, low demand and falling billets prices weighed on sponge iron offers, as prices declined by INR 300-950/t w-o-w.

- Vizag Steel has floated an ocean sale export tender for 30,000 t of steel blooms (150x150mm, 3SP/4SP) on FOB ST delivery against 100% advance payment terms. The last date for bid submission is 23 March, 2023 and the delivery is scheduled for 15 May.

- Tata Metaliks has reduced pig iron (both basic and foundry grades) prices by INR 1,300/t ($16/t) to INR 46,200/t (foundry grade) and INR 43,200/t (Basic grade, Si 1.0-1.5%). Prices are exw-Kharagpur and applicable for Kolkata and Howrah.

- SAIL-Rourkela Steel Plant (RSP) conducted an auction for 4,000 t of steel grade pig iron on 16 March, 2023. About 3,300 t of material was booked at INR 40,000/t exw, sources informed.

- A state-owned steelmaker had floated a spot sale export tender for 30,000 t of blooms (BF-route, 150x150mm, 3SP/4SP grade) for end-April shipment. The deal was concluded at $600-605/t FOB, sources informed.

Finished long

- India’s finished long steel market of IF-route observed limited buying enquiries throughout the week across regions. Overall market remained volatile this week due to fluctuations in prices of the semi-finished steel and an uncertain market trend that slowed down purchase capacity in finished steel.

- This has impacted rising inventories in the mills putting pressure on manufacturers to give the tradable discount or to decline the offers in spot market. Rebars steel prices fell by INR 200-1,000/t w-o-w across regions as per SteelMint’s assessment. The trade reference price of Fe 500 grade rebars manufactured via the IF-route for 10-25 mm size was assessed at INR 49,800-50,200/t exw Raipur, INR 55,000-55,500/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 52,200-52,700/t exw Raipur. Trade reference price in steel wire rods (5.5 mm, SWRY 14) in Raipur is at INR 50,500-51,000/t exw and INR 49,800-50,200/t exw Durgapur, prices are excluding GST at 18%.

- Trade level prices of rebars made through blast furnace (BF) route fell w-o-w as subdued demand weighed on the market. Prices have been on decline for the sixth consecutive week in a row. Moreover, buying interest continued to remain low post-Holi as buyers are struggling with higher interest rates and distribution channel participants are facing challenges of delay in credit collection.

- SteelMint’s weekly price assessment for rebars (12-32 mm, BF-route, IS 1786, Fe500D) fell by INR 800/t w-o-w to INR 60,800/t, exy-Mumbai, excluding GST at 18%.

Finished flat

- Trade level prices of flat steel products declined this week in key markets. Market activity is still sluggish as buyers are struggling with higher interest rates and distribution network participants are challenged by delays in credit collection. Demand in the traders’ market is around 5-10% at present, shared some reliable sources. Trade market prices might stay rangebound in the latter half of this month, as participants’ focus shifted to book reconciliation as the fiscal year comes to an end.

- On the export’s front, India’s HRC (SAE1006) export index has increased by $8/t w-o-w to $716/t FOB east coast India. Higher offers quoted by mills in the UAE market is the major reason behind this. However, buying interest is slow in the UAE amid the availability of cheaper alternatives. EXIM trade participants opined that prices to elevate further amid buoyed global market sentiments. In addition, Indian mills have been signing export deals to the Europe with prices rising in each successive deal for April and early-May deliveries.

Leave a Reply