The South Asian ferrous scrap market showed mixed sentiments as major participant India remained somehow inactive. Meanwhile, some bookings were heard from Bangladesh and Pakistan after a long gap.

Indian imported ferrous scrap market remained slow as negotiations remained on hold for bid-offer disparity. Mostly the western region of India remained inactive due to prior bookings of Pakistan-routed materials. These materials reached recently, creating scope for sufficient availability and fresh bookings might be heard at the end of March.

The domestic ferrous scrap market, returning from Holi in India, mostly remained positive with minimal price revisions d-o-d. On the other hand, the finished and semi-finished markets showed mixed price trends with region-wise price corrections, both positive and negative.

Local scrap availability in Bangladesh is tight. The production cost is increasing continuously due to a hike in electricity prices by around BDT 700-800 every month, Letters of credit (LCs) problems from the Central bank are still a matter of concern. However, in the recently-concluded Kanto tender, 15,000 t of H2 scrap have been booked at JPY 55,388/t ($406/t) FAS to Bangladesh.

Turkish deep-sea scrap purchases increased after touching a 10-month high in recent deals from the US and Europe.

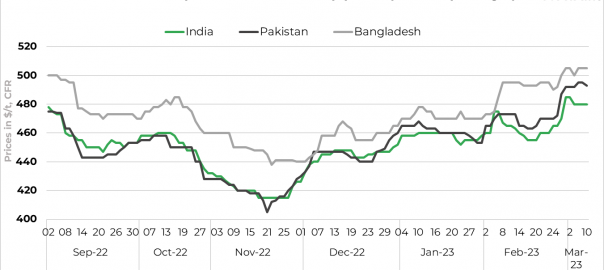

Recent deals:

- Around 500 t of New Zealand-origin containerised shredded was booked at $505/t CFR Bangladesh.

- A parcel of 1,000 t of New Zealand-origin HMS (80:20) was booked at $490/t CFR Bangladesh.

- A cargo of 500 t of New Zealand-origin bundles was booked at $460/t CFR Bangladesh.

- Around 500 t of Singapore-origin PNS scrap in containers have been booked at $525/t CFR Bangladesh.

- A volume of 500 t of Europe-origin containerised shredded was booked at $500/t CFR Bangladesh.

- Around 500 t of containerised HMS bundles were booked at $445/t CFR Bangladesh.

- Around 4,000 t of containerised shredded scrap were booked at $493/t CFR Pakistan.

Price assessments

- Europe-origin shredded scrap offers into India stood at $480/t CFR Nhava Sheva, unchanged d-o-d.

- UK-origin shredded scrap prices stood at $505/t CFR Chattogram, unchanged d-o-d.

- UK-origin shredded scrap prices stood at $493/t CFR Qasim, slightly down by $2/t d-o-d.

Leave a Reply