The domestic steel market witnessed mixed price trends during week 9 ( 27 February-4 March, 2023). Semi-finished steel prices fluctuated in the range of INR 50-1,100/tonne (t).

Domestic induction furnace-finished long steel market witnessed volatility in prices. Offers varied in the range of INR 100-900/t w-o-w. Trade reference prices for HRC and CRC increased in the range of INR 400-1,400/t across regions.

Iron ore and pellets

- SteelMint’s bi-weekly domestic pellets (Fe 63%) index, PELLEX, remained stable at INR 10,200/tonne (t) DAP Raipur compared to the last assessment on 24 February, 2023. No deal was reported in this publishing window due to low buying interest. Currently, market participants are in a wait-and-watch mode.

- NMDC conducted an iron ore auction from Chhattisgarh for 10,000 t of sized Baila lumps (Fe 65.5%, indicative) from its Bacheli mines on 2 March. According to sources, the entire quantity was booked at INR 4,996-5,006/t against the base price of INR 4,836/t. The floor price excluded royalty, DMF and NMET charges, and delivered FOT (by truck) ex-mine.

- Vedanta conducted an auction for sale of 32,000 t of iron ore lumps from its A. Narrain mines in Karnataka’s Chitradurga district on 28 February. According to sources, the entire quantity offered (10-40mm, Fe57.25%) was booked at INR 3,729/t against the floor price of INR 3,689/t. Price was exclusive of royalty, DMF, and NMET charges.

- SteelMint’s India pellets (Fe 63%, 3% Al) export index FOB east coast was recorded at $123/t, down $3.5/t w-o-w. Iron ore prices in China have come under pressure as the government has mandated curbs in production to contain air pollution. This, in turn, has created an uncertainty about demand in the near term.

Coal

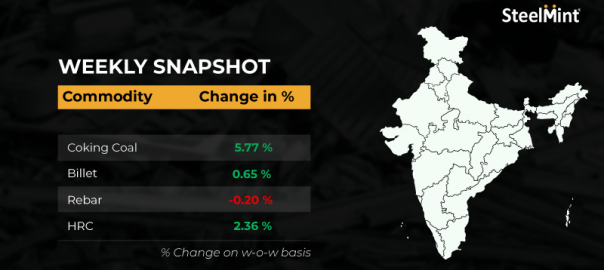

- Australian premium hard coking coal prices increased by $21/t w-o-w to $368/t FOB and $385/t CNF on 4 March. Strong buying interest from Asia and Europe has led to an increase in prices.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag port have been recorded at 10,300/t, majorly stable w-o-w.

- RB1 (6000 NAR) grade prices inched down w-o-w to $139.65/t FOB and RB3 prices recorded a rise to 104/t FOB, up by $9 w-o-w.

Ferrous scrap

- Indian ferrous scrap prices remained high as offers from the suppliers’ side increased by $20-25/t w-o-w on high demand from active Turkish buying last week. Market participants expect stablility in prices over the next few weeks.

- Experts speculate that Indian ferrous scrap import volumes could touch 10 mnt in the coming years because of higher estimated demand for steel. The domestic steel and scrap market in India saw no major movement in prices ahead of the Holi holidays. Hence, buyers were mainly muted this week in view of payment settlement concerns.

- SteelMint’s assessment for imported shredded scrap in containers is at $480/t CFR, up by $15-20/t w-o-w.

Ferro alloys

- As per SteelMint’s assessment on 3 March, Indian silico manganese prices inched down by 2% w-o-w to INR 74,100/t ex-Durgapur, INR 74,000/t ex-Vizag, and INR 74,900/t ex-Raipur. Due to gloomy trends in the domestic markets, prices of silico manganese decreased.

- Indian ferro manganese prices were almost stable w-o-w at INR 78,000/t ex-Durgapur and ex-Raipur at INR 78,500/t. Since demand for special steel remained muted, ferro manganese prices stayed stable.

- Indian ferro chrome prices dropped w-o-w due to selling pressure amid weak demand in the domestic market at higher prices. According to SteelMint’s assessment on 2 March, smelters were offering at around INR 121,400/t exw Jajpur, down by around INR 3,750/t w-o-w.

- Ferro silicon prices in Bhutan dropped in the beginning of March as sellers were keen to attract buying interest. According to SteelMint’s assessment on 3 March, ferro silicon prices were hovering at INR 120,000-122,000/t exw from both Bhutan and Guwahati. Some major producers in Bhutan were offering higher at around 126,000/t exw because they had sufficient orders in hand and were not in a rush to sell material at lower prices.

Semi-finished

- The semi-finished steel market saw volatility in prices as demand was moderate which led to price fluctuation.

- Domestic billets prices increased by INR 200-1,100/t while sponge iron offers fluctuated in the range of INR 50-700/t.

- SAIL-Rourkela Steel Plant held an auction for 3,000 t of steel grade pig iron on 1 March. The entire quantity was booked in the range of INR 40,835/t exw.

- Steel Authority of India Ltd (SAIL) held an auction for 2,000 t of basic pig iron on 3 March from the Durgapur Steel Plant (DSP). Buyers booked 1,200 t out of the total material at INR 41,250/t exw, sources informed.

- Tata Metaliks has reduced pig iron prices by INR 1,300/t ($16). Fresh offers for foundry grade are at INR 47,500/t and basic grade (Si 1.0-1.5%) at INR 44,500/t exw Kharagpur. Prices are exw-Kharagpur and applicable for Kolkata and Howrah markets.

Finished long

- India’s induction furnace rfinished long steel prices saw mixed price trends. Buying enquiries were limited from end-users, which prompted suppliers to offer discounts in order to liquidate material. A similar trend in the sponge iron and billet segments turned the finished steel market volatile even though buying activities remained average throughout the week, smooth lifting of previously-booked material was reported by mill officials.

- Rebar prices fluctuated across regions. Prices increased by INR 100-900/t in the nothern, eastern and central regions. Meanwhile, in some locations, prices remained stable or dropped INR 100-300/t.

- The trade reference price of Fe 500 grade rebars manufactured via the IF-route for 10-25 mm size was assessed at INR 50,000-50,400/t exw Raipur, INR 55,000-55,500/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stand at INR 52,500-53,000/t exw Raipur.

- Trade reference prices of steel wire rods (5.5 mm, SWRY 14) in Raipur were at INR 50,500-51,000/t exw and INR 50,100-50,500/t exw Durgapur. Prices are excluding GST at 18%.

- This week all primary mills rolled over list prices of rebar m-o-m for early-March deliveries. Increasing gap between BF and IF route rebars is one of the prime reasons why prices remained unchanged. Meanwhile, trade level prices of rebars made through the blast furnace (BF)-route continued to fall across markets as low demand weighed on sentiments.

- SteelMint’s weekly price assessment for rebar (12-32 mm, BF-route, IS 1786, Fe500D) fell by INR 300/t w-o-w to INR 62,300/t, exy-Mumbai, excluding GST at 18%.

Finished flat

- An Indian steel major announced an increase of INR 2,000/t for HRCs and CRCs. A hike of INR 1,500 for plates’ list prices had come into effect from 1 March, 2023. Similarly coated steel list prices were raised by INR 1,000-1,500/t for early-March sales this week. Elevated raw material prices, good levels of export bookings in the past, and strong performing global prices have been the major reasons behind this hike.

- Trade level prices of hot-rolled coils (HRCs) have shown a substantial increase, rest others stayed range-bound. Lacklustre buying interest in the traders’ market has kept activities low. The observance of the Holi festival in the upcoming week has led to shortage of labour in some markets. This is going to keep the market activity low next week, hinted a reliable source. Prices shall also stay range-bound next week, he added.

- On the exports’ front, there have been very limited activities over the past couple of weeks. European buyers’ appetite for imported products is satiated at present as they did make decent bookings over the past couple of months. Buyers in the middle east also stayed on the sidelines and started countering with lower bids amid cheaper alternatives from China. SteelMint’s India HRCs (SAE1006) export index stood unchanged at $708/t FOB east coast this week.

Leave a Reply