Major Indian flat steel producers have increased their HRC and CRC prices in the range of INR 1,000-2,000/tonne ($12-24/t) with effect from 1 March 2023. Cost pressure from the elevated raw material prices and sustained upward momentum of global prices have propelled mills to take the decision, hinted a reliable source.

Project orders have driven the demand for hot rolled coils (HRCs) and cold rolled coils (CRCs) since mid-January, keeping the mills satiated.

Meanwhile, improved overseas demand — especially from Europe — has led to the conclusion of multiple deals in the last couple of months. On the other hand, the cautious approach of end-buyers has weighed on the domestic traders’ market activity.

Trade-level prices of HRCs increased by INR 1,400/t ($17/t) w-o-w and those of CRCs by INR 800/t ($10/t) w-o-w following the price increases by mills.

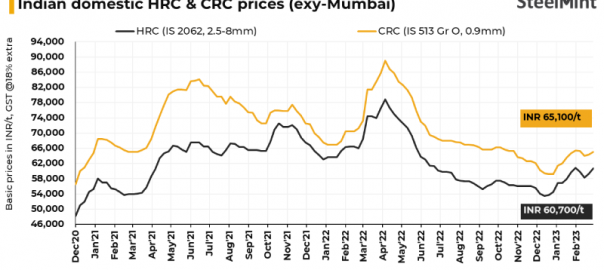

SteelMint’s benchmark HRC (IS2062, 2.5-8mm) prices stood at around INR 60,000-61,000 ($728-740/t) exy-Mumbai and those of CRC (IS513 Gr O, 0.9mm) at INR 64,500-65,500/t ($783-795/t) exy-Mumbai as assessed on 1 March 2023. Prices exclude GST at 18%.

Why have mills increased prices?

1. Cost pressure: Elevated raw material prices have pushed mills to raise prices. For instance, SteelMint’s Odisha iron ore fines (Fe 63%, 0-10mm) index which was treading in the territory of INR 4,000/t ($49/t) in December 2022, moved up to INR 5,000/t ($61/t) since early January and by the end of January had touched INR 5,750/t ($70/t). The prices further increased to INR 6,000/t ($73/t) as last assessed on 25 February after hovering at INR 5,750/t in the three preceding weeks. All prices mentioned above are on an ex-mines basis.

Similarly, imported hard-coking coal (HCC) prices increased steeply during this period. The weekly average price of Australian-origin Premium HCC stood around $263/t CNF India for the week ended 3 December and increased to $396/t CNF by the week ended 18 February, as per SteelMint records. This marks a steeper increase of $133/t.

Thus, mills went for a price hike to pass on the cost impact to the market.

2. Improved exports helped ease inventories: Most of the Indian steel producers went scouting the global waters as the 15% export duty on clad or plated non-alloyed steel products was lifted on 19 November. Securing multiple export deals over the period from December till mid-February has helped mills to ease inventories and now they have limited allocations for April shipments, informed a reliable source. Steel majors were actively exploring the higher realizations that the European market offered.

The Middle East markets were among other targets for exports too. This led to a steeper increase in SteelMint’s India HRC (SAE1006) export index. The index was assessed at $708/t FOB east coast India on 28 February, up by a steep $108/t from $600/t FOB as on 3 January.

3. Expectation of improved demand: The expectation of further pick up in demand from major projects from the infrastructure and construction businesses is another reason. The monthly activity reports of the Ministry of Road Transport and Highways (MoRTH) have shown a four-figure addition of 1,029 kilometers (km) to the existing national highways network in January 2023. The ministry further awarded 1,137 km of national highways to be added. Thus, seeing the improved speed of infrastructure and construction industries, participants opine this sector will continue driving the demand for steel in March. White goods and general engineering industries are some other segments that shall see a boost as summer kicks in, hinted a source.

Outlook

Trade-level HRC and CRC prices are likely to stay supported in the near term amid an expected pick-up in market activities. In addition, there are further opportunities in exports. That apart, better-performing global HRC prices will also likely lend support to domestic prices as fresh import bookings will not be a viable option for market participants.

Leave a Reply