- Iron ore fines supply a challenge as miners near year-end EC limits

- Semis dip amid drop in local demand for finished steel

- Finished prices hinging on exports, Turkey demand

Morning Brief: Steel and raw material-related prices showed a mixed trend m-o-m in February 2023, as per data maintained with SteelMint. It was mainly the cost push, along with positive global sentiments, that led to a spurt in finished prices. SteelMint goes behind the scene:

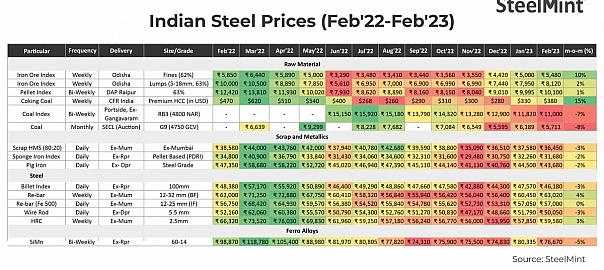

1. Coal

a) South African RB3: The bi-weekly index tracking the average portside ex-Gangavaram prices of the South African RB3 4800 NAR dropped 7% m-o-m in February, 2023 to INR 11,000/tonne (t) compared to INR 11,820/t in January, 2023. Prices of this grade have been declining for some time now amid weakened demand from sponge iron units, which are the main buyers of South African coal. But sponge prices themselves have dipped on lesser demand for finished steel.

Imported South African coal prices had touched stratospheric levels last year, following the onset of the Russia-Ukraine war. Sanctions on Russia and a natural gas inflation impelled Europe to seek other coal sources, South African being one. This factor led to a supply shortage and spurt in prices of the same. However, thanks to the recent plunge in gas prices in EU– due to milder temperatures, enough inventory stock-up and a drop in demand from the industrial sector — imported thermal coal (including RB3) prices have also started cooling down since the last few months.

b) Australian low-vol HCC coking coal: Average prices of the Australian low-vol HCC rose 15% m-o-m in February 2023 to $380/t against $330/t in January. Mainly three factors are leading to the persistent m-o-m rise. One is the supply tightness emanating from the unfavourable weather conditions in Queensland which hampers coal evacuation. Second is the post-Covid domestic steel demand uptick in China which has been leading to some aggressive buying from this steel-producing giant. Thirdly, Australia witnessed a spurt in demand from Europe from January, post-Christmas and New Year holidays.

c) SECL’s G9 (4750 GCV) auctions: Prices in these auctions dropped 8% m-o-m to INR 5,711/t in February 2023 against INR 6,189/t in January.

In fact, prices dropped primarily due to higher offerings.

South Eastern Coalfields (SECL), along with another major Coal India subsidiary, Mahanadi Coalfields (MCL), had twice conducted auctions in February, 2023 in tandem with the increase in production.

In SECL’s case, prices of G9 dropped 12% to INR 5,000/t in the latest auction held on 27 February as against INR 5,711/t on 7 February.

Imported Indonesian prices are usually higher than domestic. Imported low CV Indonesian hovered at around $52/t a week back which works out to a little above INR 4,000/t FOB. The high CV was pegged at $121/t FOB (nearly INR 10,000/t). If imported prices become competitive then domestic may be under pressure.

2. Ferro alloys

Silico manganese 60:40: Prices of the bi-weekly 60:14 grade silico manganese index emerging out of Raipur fell 5% m-o-m to INR 76,670/t in February, 2023 against INR 80,335/t in January. Moderate finished steel demand saw limited enquiries for the material in the domestic market. Sluggish global demand led to fewer exports bookings. Moreover, overseas buyers sought material at prices lower than expectations. Overall, the silico manganes market remained dull in February.

3. Scraps and metallics

All showed a m-o-m dip, albeit negligible, in a range of 2-3%, mainly on account of an increase in raw material prices coupled with moderate finished steel demand in local markets. Sponge especially fell because of the dip in billets prices.

Liquidity issues in the local markets also kept prices sluggish and range-bound for metallics.

“On the one hand, raw material prices are high, on the other, sponge and billet prices are coming down. There is no clarity and traders are wary,” said a source.

a) Pellet-based P-DRI: The pellet-based P-DRI, ex-Raipur, edged down 2% to INR 31,680/t in February, 2023, compared to INR 32,260/t in January.

b) Steel grade pig iron: Prices also dipped 2% m-o-m in this period to INR 43,680/t (INR 44,500/t in January).

c) Domestic scrap prices (ex-Mumbai): These lost 3% to INR 36,450/t last month against INR 37,580/t in January. Prices were somewhat volatile if tracked on a daily basis, due to liquidity crunch and limited demand for finished steel.

4. Iron ore

This raw material, in terms of fines, lumps and the high-grade 63% pellets, showed an increasing trend m-o-m.

Fines, lumps and pellets: Fe63% fines from Odisha rose a marked 10% to INR 5,480/t (INR 5,000/t) in February 2023 while the Fe63% lumps (Odisha) upped 2% to INR 8,120/t (INR 7,950/t) m-o-m. Fe63% pellets (DAP Raipur) remained almost stable, gaining 1% m-o-m to INR 10,100/t (INR 9,995/t).

Iron ore availability has become an issue amid exhausting environmental clearance (EC) limits of merchants miners with the fiscal year-end approaching. Mills are finding it a challenge to secure supplies of high grade ores.

At the same time, sponge and billets demand is sluggish, impacting their prices downward while finished steel trades are limited, affecting all upstream commodities.

Iron ore supply from Odisha miners has been impacted due to constraints in rakes availability. Preference is being given to coal transportation at the cost of iron ore.

5. Steel

This segment, comprising billets and finished products, saw a mixed trend.

a) Billets: The ex-Raipur billet index dipped 3% m-o-m to INR 46,180/t in February, (INR 47,570/t in January) amid dull finished steel sales.

b) Rebar: The ex-Mumbai BF-grade rose 4% to INR 63,020/t (INR 60,450/t) in the period under review. The IF grade remained flat at INR 57,050/t (INR 57,050/t) while wire rods (ex-Durgapur), dipped 3% to INR 50,050/t (INR 51,790/t) last month. Fourth quarter procurement from the infrastructure segment kept BF-route rebar supported. IF-route rebar stayed flat amid liquidity crunch in the market and tepid finished demand.

c) HRC: Ex-Mumbai trade-level HRC prices upped 3% to INR 59,580/t (INR 57,850/t). HRC prices remained supported by the uptick in exports especially from Europe. Volumes did not meet expectations, nor did Southeast Asia show any interest but mills could fall back on domestic demand and even effected a few quick rounds of price increases.

Outlook

Longs demand from the project segment may become cold from here and this could reflect in the prices. On the other hand, if quake-hit Turkey buys billets in large volumes from India, then longs will stay supported.

Flats may remain under some pressure since exports are yet to pick up to pre-export duty levels of 1 million tonnes per month while domestic demand may stay moderate.

Iron ore and coking coal prices could stay propped if China continues to buy.

Market participants do not see any clear short-term price directions.

Leave a Reply