The domestic steel market witnessed downtrend during week 8 ( 20 February- 25 February, 2023). Semi-finished steel prices fell in the range of INR 400-1,700/tonne (t).

Domestic induction furnace-finished long steel offers saw negative price trend, offers dropped by up to INR 100-1,600/t w-o-w. The trade reference prices for HRCs and CRCs increased in the range of INR 300-1,000/t across region.

Iron ore and pellets

- SteelMint’s bi-weekly domestic pellets (Fe 63%) index, PELLEX, remained stable at INR 10,200/tonne (t) DAP Raipur compared to the last assessment on 21 February 2023. Around 35,000 t of deals were reported in this publishing window. The index remained range-bound amid fall in sponge iron offers.

- JSW conducted an auction for 600,400 t of iron ore fines. 197,500 t of fines (Fe54.5%) and 402,900 t of fines (Fe56%) were booked at INR 2,350/t and INR 3,010-3,040/t, respectively. ESL conducted an auction for 40,000 t of iron ore fines (Fe 57%) and the entire quantity was sold at INR 4,050-4,100/t against the floor price of INR 3,800/t. Prices include royalty, DMF, and NMET charges and is on ex-mines/plot.

- NMDC conducted an auction for 520,000 t of iron ore (both fines and lumps) from its Donimalai mines in Karnataka on 21 February, 2023. According to sources, 68,000 t of lumps (10-40mm, Fe61% indicative) were booked at INR 3,301/t while 160,000 t of fines (Fe59% indicative) were booked at INR 2,872/t. All materials were booked at the base price, and excludes royalty, DMF, and NMET charges.

- Vedanta conducted an auction for sale of 36,000 t of iron ore lumps from its A. Narrain mines in Karnataka’s Chitradurga district on 22 February, 2023. According to sources, 28,000 t of the material (Fe56.5%) was booked at INR 4,056/t against the floor price of INR 3,647/t. Price was exclusive of royalty, DMF, and NMET charges.

- SMIORE conducted an auction for 361,000 t of iron ore on 22 February, 2023. Out of which, 60,000 t of fines (Fe57-58.70%) were booked at INR 2,970-3,650/t and 1,000 t of lumps (10-40mm, Fe58.80%) at INR 3,650/t. Prices were inclusive of royalty, DMF and NMET charges.

- SteelMint’s India pellets (Fe 63%, 3% Al) export index FOB east coast was recorded at $126.5/t, up $8.5/t w-o-w due to positive buying interest and some active deals. Indian pellets exports prices increased on the back of a hike in global iron ore prices as China’s real estate market is expected to rebound with the help of more stimulus by the government.

Coal

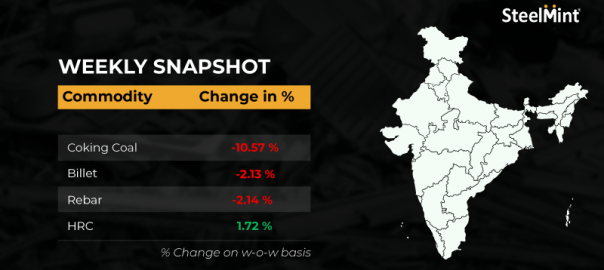

- Australian premium hard coking coal prices plunged by $43/t w-o-w to $347/t FOB and $364/t CNF on 25 February, 2023. Improvements in supplies resulted in a fall in prices as logistical bottlenecks have eased. Moreover, buyers opted for the sideline as prices started falling.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port have recorded a drop to INR 10,300/t, down by INR 300/t w-o-w ex-port.

- RB1 (6000 NAR) grade prices have been majorly stable at $142.35/t FoB. RB3 prices remained firm at $95-96/t FOB.

Ferrous Scrap

- The global ferrous scrap price remains largely volatile South Asian market remained mostly somehow alive with smaller deals with India and Bangladesh, but in Pakistan, it was the same with negligible trade activities as weeks before. Whereas, Turkiye trade volumes abruptly increased due to the requirement for rebar for upcoming reconstruction activities. SteelMint’s daily assessment for HMS 1&2 (80:20) from the US stood at $448-50/t CFR Turkiye, significantly up by $35-40/t w-o-w.

- Indian ferrous scrap market slow w-o-w: Indian ferrous scrap prices largely upwards with limited buying. Whereas, sellers keep quoting higher offers amid Turkish uptrend prices throughout this week. Major ports like Kandla receive bulk arrivals of around 40,000 t and small container consignments have been notified mostly from Europe, Venezuela, Bahrain, and South Africa. SteelMint’s assessment for imported shredded scrap in containers is at $465/t CFR, up $10/t w-o-w.

Ferro Alloys

- Indian silico manganese prices fell this week as buyers were hesitant to book the material at higher prices and began negotiating aggressively. According to SteelMint’s assessment on 24 February, the current market price for 60-14 grade was hovering around INR 75,500-75,600/t exw from Raipur, Durgapur and Vizag, major manganese alloys producing regions in India.

- Indian ferro manganese (HC70%) prices declined on an inadequate buying. According to SteelMint’s assessment on 24 February, prices of ferro manganese decreased to INR 78,500-78,700/t exw for both Durgapur and Raipur.

- According to SteelMint’s assessment on 23 February, Indian ferro chrome (HC60%) prices remained stable at INR 125,100/t exw. Indian smelters were unwilling to reduce offers in an anticipation of a hike in the Chinese stainless-steel giant’s upcoming purchase tender price.

- Indian ferro silicon (70%) prices inched down due to end users’ hard bargaining. According to SteelMint’s assessment on 24 February, Guwahati’s ferro silicon offers were at around INR 124,000/t exw. However, Bhutan producers kept their ferro silicon offers unchanged at INR 126,000/tonne (t) exw.

Semi-finished

- Indian semis trade slowed down this week as prices slumped by INR 400-1,700/t amid lessened inquiries of finished products in major markets.

- The domestic billets prices have decreased by INR 550-1,700/t. Similarly, sponge manufacturers were being pressurised and they started reducing their offers by INR 400-1,150/t w-o-w.

- SAIL-Bhilai Steel Plant (BSP) held an auction for 5,000 t of steel grade pig iron on 20 February, 2023. The entire quantity was booked at an average price of INR 41,885/t exw, sources informed.

- Steel Authority of India Ltd (SAIL) held an auction for 3,000 t of basic pig iron on 24 February, 2023 from the Rourkela Steel Plant (RSP). Buyers booked 2,400 t out of the total material at INR 40,850-40,950/t exw, sources informed.

Finished Long

India’s induction furnace route-finished long steel ended up with prices falling even lower w-o-w on weak buying interest and an uncertain market direction. Decline in semi-finished steel (billets) prices specifically in the key markets of northern and central region also led to a similar effect on prices of finished long steel segment. Apart from reducing prices, manufacturers even started offering discounts in order to liquidate material as per quantity and payment terms. Due to minimal activity in the spot market, a slight inventory pressure persisted on the suppliers.

- Rebars steel prices sharply decreased by INR 100-1,600/t w-o-w across regions as per SteelMint’s assessment.

- The trade reference price of Fe 500 grade rebars manufactured via the IF-route for 10-25 mm size was assessed at INR 50,100-50,500/t exw Raipur, INR 55,000-55,500/t exw Jalna.

- Trade discount given by Raipur-based heavy structural steel manufacturers is in the range of INR 2,000-2,500/t and trade reference price of 200 mm angles stood at INR 56,500-57,000/t exw Raipur.

- Trade reference price in steel wire rods (5.5 mm, SWRY 14) in Raipur is at INR 49,600-50,100/t exw and INR 49,600-50,000/t exw Durgapur, prices are excluding GST at 18%.

- Trade level prices of BF-route rebars registered a drop w-o-w across key markets amid slow domestic demand. Furthermore, market participants are awaiting price announcement for March deliveries from primary mills, which are likely to come next week.

- SteelMint’s weekly price assessment for rebars (12-32 mm, BF-route, IS 1786, Fe500D) dropped marginally by INR 200/t w-o-w to INR 62,600/t, exy-Mumbai, excluding GST at 18%.

Finished Flat

- Trade level prices of finished flat steel products rebounded in the key markets as two major mills increased their list prices at the beginning of the week. On the other hand, HRCs and CRCs prices saw marginal drops in some markets. But distributors in those markets are likely to start quoting higher in the upcoming week, informed sources.

- Order books of most of the mills are decently filled till March. Hence, mills are likely to start quoting for mid-April sales and later for exports, as per the market chatter. In addition, mills are likely to raise their list prices for March sales soon amid elevated prices of raw materials such as iron ore and coking coal and coating materials such as zinc and aluminum. Market participants are hoping for a revival in the end-consumers’ buying interest as the fiscal year enters its final month.

- On the export front, SteelMint’s India HRC (SAE1006) export index stood unchanged at $708/t FOB east coast this week. Indian mills stay muted in the Vietnamese market. They have maintained their export offers for the Middle East markets. Last week, a major mill had booked about 40,000-50,000t HRC for export at $790-800/t CFR for April or mid-April deliveries. Current week indications from India have stood around $740-750/t UAE and $800-810/t CFR Europe.

Leave a Reply