Australian coking coal exports stood at 10.48 million tonnes (mnt) in January 2023, a decrease of 21% m-o-m and 16% y-o-y. The drop in exports was due to heavy rains and floods in Australia, which caused disruptions in supplies. Notably, this is the second consecutive monthly decline in coking coal exports from Australia.

Port-wise analysis

Floods induced by heavy rains in north and central Queensland blocked coal shipments to Dalrymple Bay Coal Terminal (DBCT), Hay Point, and Abbot Point. Notably, Queensland is Australia’s largest producer of coking coal.

In terms of volume, DBCT witnessed the largest drop in cargoes at 1.73 mnt m-o-m. In January, the port exported 2.57 mnt of coking coal compared to 4.3 mnt in the previous month.

However, Hay Point Port was less affected by the rains despite being adjacent to DBCT port.

Coking coal shipments from Abbot Point port dropped 60% m-o-m in January to 1.46 mnt. Exports via Port Kemble were negatively impacted by rains in New South Wales.

Gladstone Port was the only port that saw an improvement in coking coal exports in January compared to December. The port exported 3.71 mnt of coking coal, a m-o-m increase of 4%. However, supplies to the port were cut off after the 29 January Blackwater rail line accident.

Company-wise exports

The top coking coal supplier in January was BMA which exported 4.16 mnt, down 2% m-o-m. Exports by key miners also fell with the exception of Jellinbah which witnessed a surge of 43% in exports to 0.72 mnt in January.

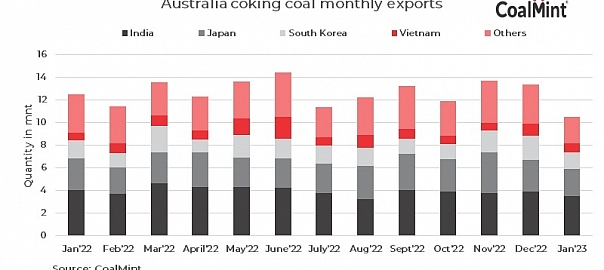

Country-wise shipments

Australia’s coal shipments to key countries – India, Japan, and South Korea – fell on m-o-m basis. Shipments to India fell by 16% m-o-m to 3.46 mnt in January while exports to Japan fell by 13% to 2.4 mnt.

Meanwhile, shipments to South Korea also fell by 33% m-o-m to 1.44 mnt.

The drop in coking coal exports to key countries was due to subdued demand. In addition, end users seem to have adopted a wait-and-watch policy with prices beginning to surge since mid-December.

On 15 December last, Australian premium hard coking coal prices stood at $250/t FOB which rose to $295/t on 31 December, an increase of 18%. Prices later rose to $335/t on 31 January, an increase of 13.5 % on-month.

However, exports to Europe rose by more than 300% in January compared to December following a revival in demand after the Christmas holidays.

Outlook

In February, it is expected that there will not be any significant improvement in supplies as shipments from the four key Queensland coal terminals fell to a six-month low in January and ship queues are above average at Queensland coal ports.

Furthermore, Gladstone Port, which closed on 29 January, is expected to reopen in the second week of February.

Leave a Reply